")

JONGHO SHIN

A guest post by D Coyne

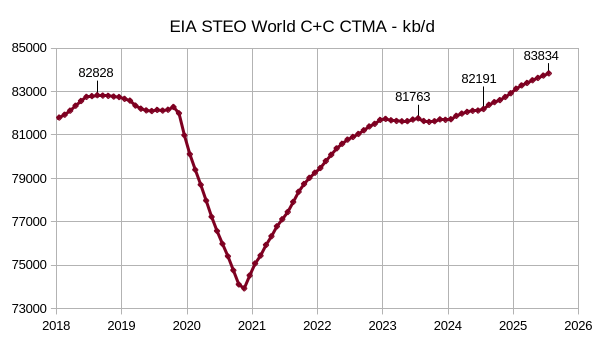

The EIA STEO was published recently, the estimate below is based on data from that report and statistics from the EIA International Energy Statistics. The EIA expects the 2018 peak for annual average World C+C output will be surpassed in 2025.

The EIA changed its method of presentation this month and now gives an estimate of World Crude output. This was compared with EIA data for C+C output from Jan 2005 to Jan 2024 so that condensate output could be estimated. I looked at the trend over the 2005 to 2024 period and simply extrapolated the trend by 23 months for World condensate output, this was added to the World forecast for crude output and is shown in the chart above. The centered 12-month average (CTMA) is presented with the July CTMA shown for selected years (2018, 2023, 2024, and 2025). In my opinion, the STEO estimate is too optimistic, my expectation is about a 500 kb/d increase in average annual output in 2024 and 2025 followed by 250 kb/d on average in 2026 and 2027 with a peak in 2027/2028 at about 83.3 Mb/d.

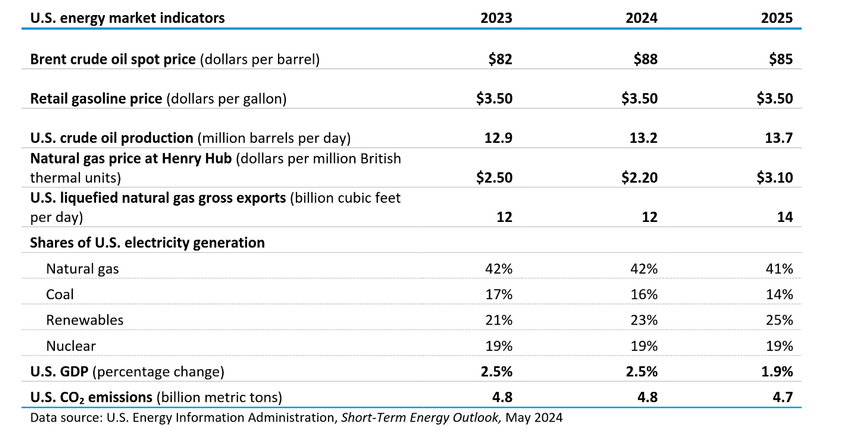

Oil prices are expected to rise to $88/b in 2024 and then fall to $85 in 2025, US oil output is forecast to rise to 13.7 Mb/d by 2025 (13.5 seems more reasonable to me). Natural gas prices fall in 2024 and then rise in 2025 with increased LNG exports from 2024 to 2025. Coal and natural gas electric power output are expected to fall, while renewable output rises from 2023 to 2025. US economic growth is expected to slow in 2025.

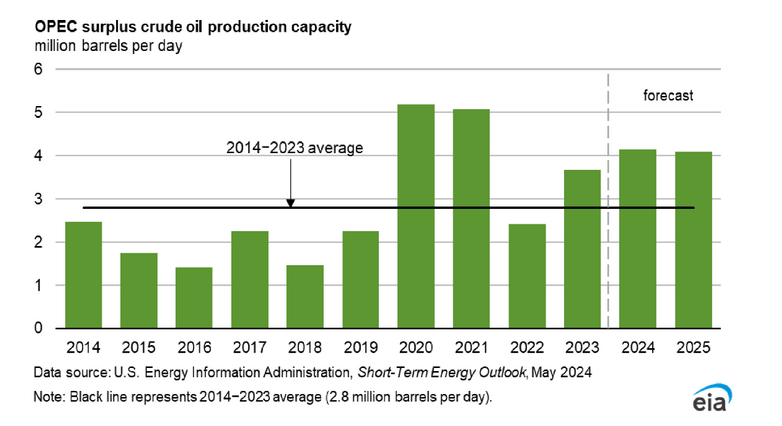

The EIA estimate for OPEC spare capacity looks high in 2024 to 2025, I would estimate it to be about 1.2 to 1.4 Mb/d less than shown in the chart above, maybe 300 kb/d below the 2014 to 2023 average shown on the chart or roughly 2.5 Mb/d.

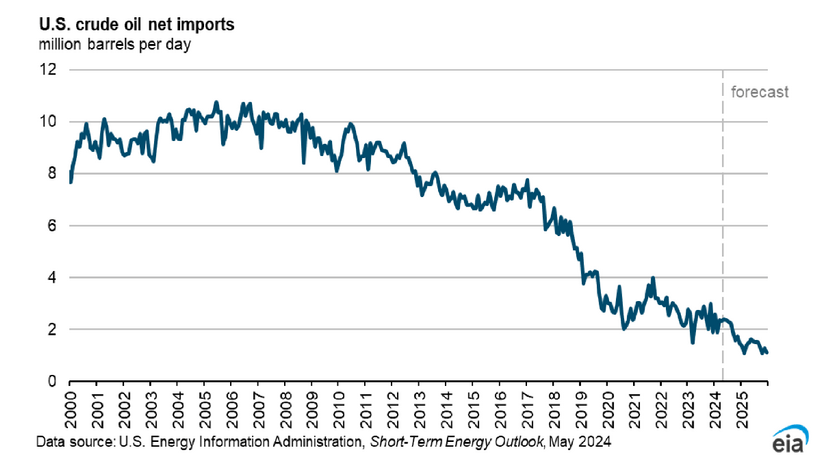

The chart above may be part of the reason the US has reduced its Strategic Petroleum Reserve (SPR) as crude oil net imports have been reduced from 10 Mb/d in 2005 to just under 2 Mb/d this past February. In February 2024, the US SPR was at about 361 million barrels and crude oil net imports were about 1.9 Mb/d, that is about 190 days of supply of crude oil net imports. Typically, nations aim for a 90-day supply or about half the level held by the US in its SPR.

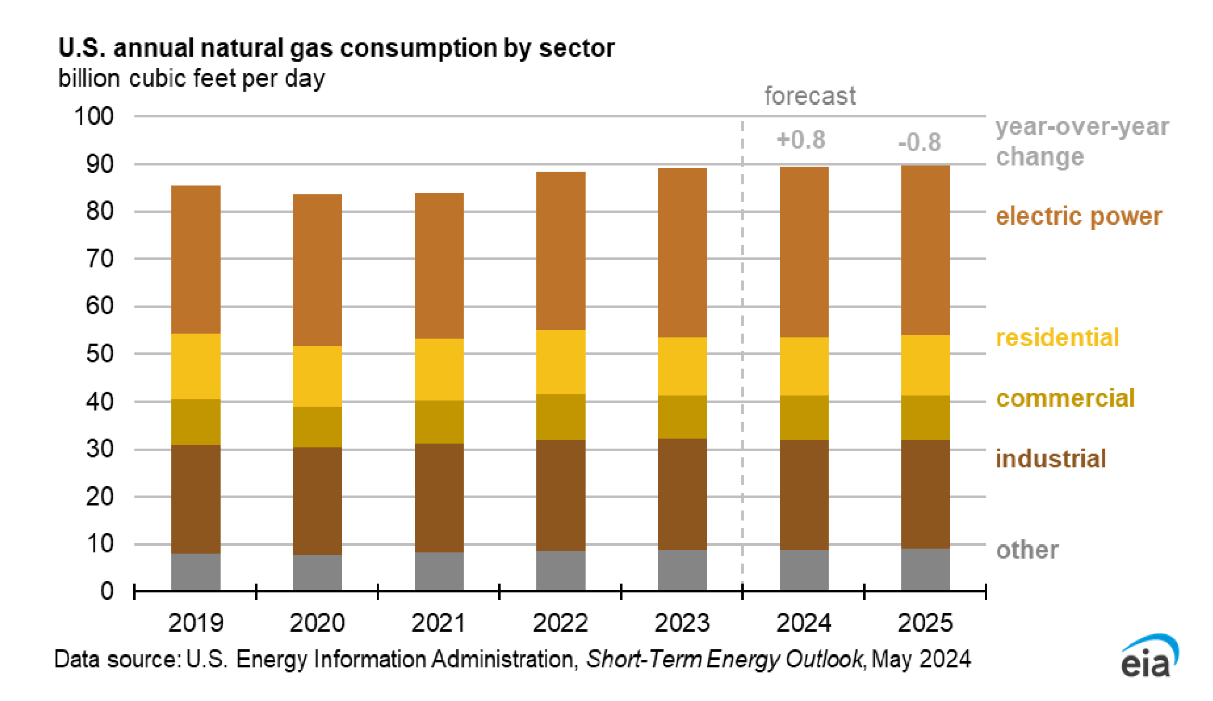

US demand for natural gas is expected to be relatively flat from 2023 to 2025.

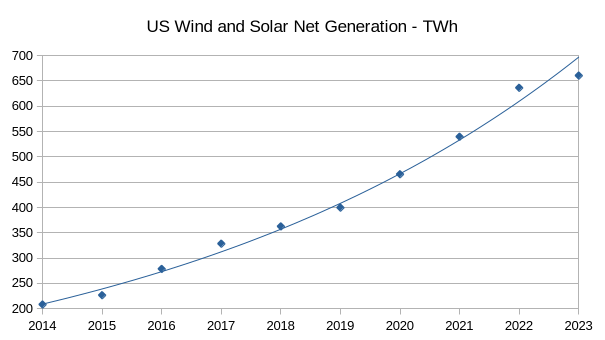

The chart above uses data from the EIA’s electric power monthly for net generation of wind and solar power from 2014 to 2023, output has grown at about a 13% annual rate with solar growing by 19.6% per year from 2017 to 2023, electric output from fossil fuel powered plants fell by 245 TWh from 2014 to 2023 with wind and solar output increasing by 452 TWh over the 2014 to 2023 period. Total US electric power output rose by 155 TWh from 2014 to 2023 with the difference of about 52 TWh (452-245-155) mostly coming from falling hydropower and nuclear power over the 2014 to 2023 period.

Editor’s Note: The summary bullets for this article were chosen by Seeking Alpha editors.

{kind=link}