The abrdn Physical Platinum Shares ETF (PPLT) is an exchange-traded fund that aims to track the price performance of physical platinum, which appears to refer to the spot (cash) price as opposed to any of the platinum futures prices. The fund’s website states:

abrdn Physical Platinum Shares ETF seeks to reflect the performance of the price of physical platinum, less the Trust’s expenses.

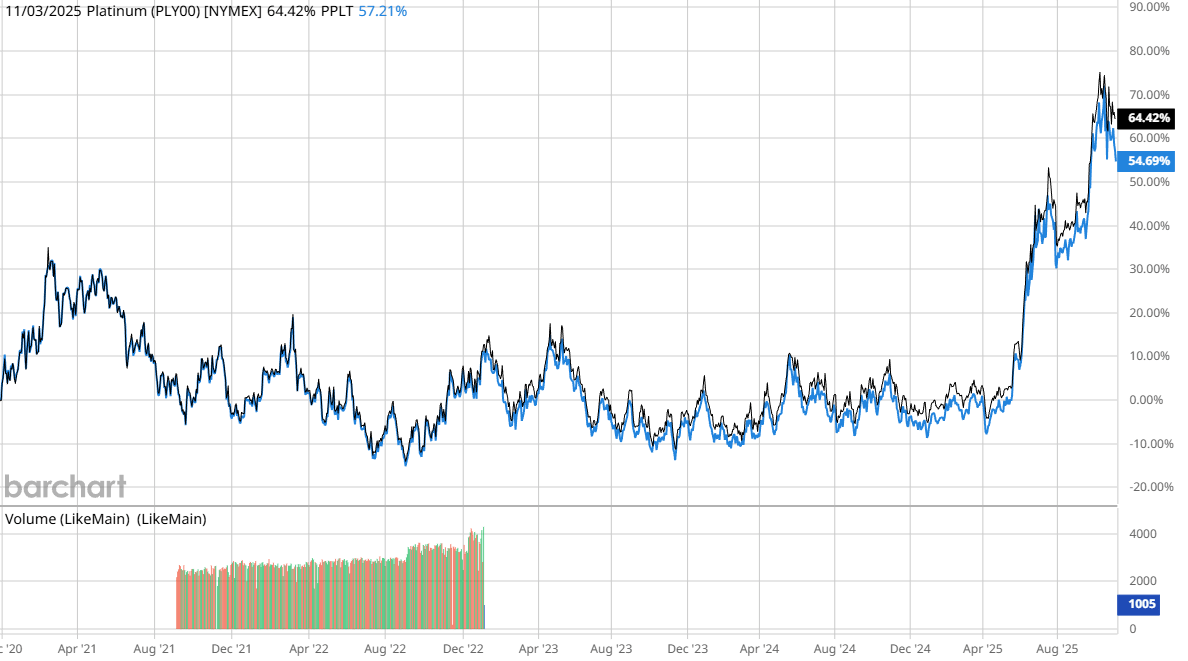

The website states that PPLT has an expense ratio of 0.60%, so we would ordinarily expect the fund to underperform platinum’s spot price by 0.60% annually. This expense ratio compounds, so that the more time that passes, the worse the fund will perform compared to physical platinum. We can see that in this chart, which shows the spot price of physical platinum over the five-year period that ended on November 4, 2025, compared to the ETF:

Barchart

In this chart, the spot price of platinum is represented by the black line, whereas the share price of PPLT is represented by the blue line. As we can see, the exchange-traded fund’s price generally moves both up and down along with the price of physical platinum. However, the more time that passes, the greater the difference between the two charts, which ultimately resulted in the exchange-traded fund underperforming the spot price of platinum by 9.73% over the period. The underperformance of the exchange-traded fund relative to spot platinum prices is largely due to the fund having expenses that cause it to underperform. All exchange-traded funds have similar fees that result in them underperforming their benchmarks over time, a characteristic known as “tracking error.” Investopedia offers a pretty good description of the causes of tracking error on its website, but in short, there are various things that can cause an exchange-traded fund to underperform its benchmark. These things can include securities regulations, management and trading fees, and other things. PPLT claims (see the fund fact sheet) to hold the physical platinum represented by each share inside a vault in London, so the fund will also have storage fees that create a drag on its performance relative to the price of the physical platinum that it holds. An individual investor who wanted to rent space in a vault in order to store platinum that they purchased on the market would also have to pay storage fees, and it is quite possible that those fees would be greater than the ones charged by this ETF. As such, despite the 0.60% expense ratio, this fund may actually be a more cost-effective way to profit from the movements of platinum prices than buying the metal itself.

About The abrdn Physical Platinum Shares ETF And Comparison To Other Options

As already mentioned, the primary objective of the abrdn Physical Platinum Shares ETF is to roughly match the performance of spot platinum prices minus the fund’s expenses. It is one of only two ETFs that attempt to achieve this goal, and it is by far the larger of the two. As of November 4, 2025, PPLT has approximately $1.94 billion in assets under management. The only other exchange-traded fund that tracks the price of platinum is the GraniteShares Platinum Trust ETF (PLTM), which has a much smaller $141.35 million in assets under management.

While PPLT and PLTM are the only two ETFs that aim to track the performance of platinum, there is a closed-end fund that offers some exposure to physical platinum. This fund is the Sprott Physical Platinum and Palladium Trust (SPPP). As the name of this fund implies, its price is influenced by the spot prices of both platinum and palladium, although it is more heavily weighted towards platinum:

Sprott

As we can see, SPPP has about 1.53 ounces of platinum for every ounce of palladium. As of November 4, 2025, platinum has a spot price of $1,559.10 per ounce, whereas palladium is a bit lower at $1,438.50 per ounce. Thus, in terms of composition, SPPP clearly has more assets invested in platinum than in palladium, and so platinum prices will have a greater impact on its market performance. However, the fact that both metals are included in the fund’s portfolio means that it will not deliver a performance that is based solely on platinum prices alone. Thus, the two ETFs are going to be the better choice if an investor wants exposure to platinum prices without the influence of other precious metals.

In terms of liquidity, the abrdn Physical Platinum Shares ETF is reasonable for most retail investors. An average of 393,603 shares change hands every day. At the price of $139.88 per share that the fund held on November 4, 2025, this works out to about $55,057,188 worth of volume every day. That should be enough to absorb most trades that an individual investor would want to make without adversely impacting the price. However, an institutional investor who is looking to invest several million dollars would likely want to space out their trades over a period of a few days to ensure that the authorized participant has sufficient time to keep the price in line with the net asset value and to ensure that there are sufficient sellers for the shares needed.

The GraniteShares Platinum Trust ETF has much lower liquidity by comparison. For this fund, an average of 513,504 shares trade every day. While that is more shares on average than PPLT, the share price of PLTM is substantially lower. As of November 4, 2025, shares of PLTM were trading at $14.80 per share, so the average daily volume is only about $7.6 million in U.S. dollar terms. That is still sufficient to absorb a trade of a few thousand dollars without much difficulty, but an investor looking to buy or sell a more sizable amount may need to be more conscious about spacing out their trades than would be the case with PPLT.

One advantage that PLTM has over PPLT is that the GraniteShares fund has a lower expense ratio of 0.50% compared to 0.60% for PPLT. In theory, that could cause PLTM to more closely track the price of platinum. Over the five-year period that ended on November 4, 2025, the GraniteShares Platinum Trust did slightly outperform PPLT (55.08% versus 54.66%), which is probably due to the lower expense ratio. However, both funds underperformed platinum’s 64.42% return over that period.

As mentioned, PPLT could be a more cost-effective way to invest in platinum than actually purchasing and storing the metal itself. One reason for this is that a 0.60% expense ratio might be lower than the storage fees that would be required for vault storage. An internet search of bullion storage costs that I conducted showed prices ranging anywhere from 0.50% to 0.70% annually of the value of the metal stored, depending on the chosen vault, location, and amount of platinum bullion that the investor wishes to store. That is reasonably in line with PPLT’s expense ratio. Furthermore, when buying platinum from a bullion dealer, an investor will have to pay a price that is higher than the spot price for platinum and may have to pay to have the metal shipped to the vault in which space is being rented. Neither of those is true with this ETF.

Finally, another major advantage that the abrdn Physical Platinum Shares ETF might have over buying and storing physical platinum is due to the fact that it is taxed differently than the metal itself. In short, shares of PPLT are taxed at either short-term capital gains rates or long-term capital gains rates, depending on how long the shares are held. Physical platinum, on the other hand, is taxed at a higher rate. As Investopedia explains:

The IRS considers physical holdings in precious metals such as gold, silver, platinum, palladium, and titanium to be collectibles. Holdings in these metals are subject to capital gains tax regardless of their form, whether they’re bullion coins, bullion bars, rare coinage, or ingots. Physical holdings in gold or silver (or platinum) are subject to a capital gains tax that’s equal to your marginal tax rate up to a maximum of 28%.

Gains from physical platinum are taxed at whatever an individual’s ordinary income tax rate is or at 28%, whichever is less. However, long-term capital gains are subject to either a 0%, 15%, or 20% tax rate, depending on the individual’s income. Thus, depending on income, taxes on gains from PPLT might be lower than taxes on the capital gains derived from physical platinum. Of course, investors who are using a retirement account to make their purchase do not have to worry about taxation, but investors who wish to invest in platinum using a standard brokerage account may want to consider the differing tax treatment that PPLT has compared to buying and storing physical platinum.

Understanding The Composition Of PPLT

As the name of the fund suggests, the abrdn Physical Platinum Shares ETF exclusively invests in physical platinum bullion bars held by ICBC Standard Bank in London, United Kingdom. The fund formerly used JPMorgan Chase as the custodian that stored the physical platinum bullion that comprises the entirety of the fund’s assets, but this role was appointed to ICBC Standard Bank on May 23, 2024. Every day, the fund releases a public report that provides the location, exact product, and serial number of every bar held in the trust’s account. A copy of the current list can be found here, but if the custodian ever changes, then investors should be able to obtain the document from the fund’s website (click on the link that says, “Bar List”).

The fund’s fact sheet states that the fund’s bars are stored under an allocated custody agreement with ICBC Standard Bank. Many precious metals consider this to be a superior form of storage to the more common (and cheaper) unallocated storage used by many precious metals investment vehicles. In order to understand why, it is important to understand the difference between unallocated, allocated, and segregated precious metals storage:

- Unallocated Storage: This essentially means that the investor does not hold title to the precious metals. Rather, the investor only owns a claim against the precious metals stored in the custodian’s vault. As the investor does not hold title to the assets, they are considered to be a creditor to the issuer, and the custodian is actually allowed to use the precious metals for their own purposes. In short, the custodian owes the investor physical metals, but there is no guarantee that the custodian actually has sufficient precious metals to back all of the claims that were made against it.

- Allocated Storage: This type of storage is much preferred by investors who are nervous about counterparty risk. In this type of storage, the investor actually holds title to specific bars or coins that can be identified by serial number. Furthermore, the custodian cannot use the precious metals for their own purposes without the express permission of the investor. In this type of custody arrangement, the investor could theoretically demand proof that the exact bars that they own are actually in the custodian’s vault.

- Segregated Storage: This type of custody arrangement is the same thing as allocated storage, with the added feature of the investor’s bars being separated from the holdings of other investors. Basically, this means that the investor has a private vault that holds only their precious metals.

The difference between unallocated storage and allocated storage can be equated with the difference between owning a real estate investment trust and owning a specific house. Segregated storage is even more secure than either unallocated or allocated storage, but it is also more expensive. The prospectus for PPLT states the following:

The Custodian segregates by identification in its books and records the Trust’s platinum in the Trust Allocated Account from any other platinum which it owns or holds for others and requires any sub-custodians it selects to so segregate the Trust’s platinum held by them. The Custodian’s books and records are expected to identify each plate or ingot of platinum held in the Trust Allocated Account in its own vault by refiner, assay or fineness, serial number and gross and fine weight.

This is characteristic of an allocated account, as the fund owns specific bars and ingots of platinum, rather than a situation where the custodian simply promises to deliver platinum on demand. The custody agreement that the fund has with ICBC also states that the fund has the authority to send an auditor to the custodian to make sure that those exact platinum products are actually in the custodian’s possession. The fund’s fact sheet states that it actually does conduct such an inspection twice during every calendar year, one of which is at a random time. This inspection is conducted by Bureau Veritas Commodities UK, which is a company that specializes in independent inspection and auditing of various metal products worldwide.

In addition to the allocated account, PPLT does have an unallocated account with the same custodian (ICBC Standard Bank). This is mostly a mechanism meant to help the fund’s share price track the price of platinum. Basically, whenever investors purchase shares, the share price could lose its link to the actual value of the platinum that the fund holds. In order to prevent this, there is an authorized participant that has the right to exchange platinum to the fund for shares that it can sell on the open market. This pushes the price of the shares down and allows the authorized participant to make a profit from the arbitrage opportunity. The reverse is also true, and if the shares of the fund are trading at a price that is less than the value of platinum backing each share, the authorized participant will buy shares of the fund on the open market and exchange them for actual physical platinum held in the fund’s vault, which pushes up the price of the shares. The unallocated account exists to facilitate transfers of physical platinum both to and from the authorized participant and support the share price of the fund relative to platinum until the physical platinum can be obtained and delivered to ICBC Standard Bank to put into the fund’s allocated storage.

In short, the fund’s assets basically consist primarily of physical platinum in allocated storage at ICBC Standard Bank, but it may also include unallocated platinum on a temporary basis whenever necessary as a way to keep the fund’s share price relatively close to its net asset value.

Composition And Relevant Details

As mentioned earlier, the abrdn Physical Platinum Shares ETF invests its assets only in physical platinum. As of September 30, 2025, the fund had 1,246,268.512 ounces of platinum in its portfolio, which provided the backing for 13,700,000 shares. This works out to approximately 10.993 shares of the fund, representing one ounce of platinum. This ratio will likely increase slowly over time as the fund sells platinum to cover its expenses.

Unlike some other commodity ETFs that are available in the market, the abrdn Physical Platinum Shares ETF does not use futures or other derivatives in its portfolio. It is simply holding physical platinum as its sole asset, and the authorized participant arbitrages the shares to keep the price in line with net asset value, as detailed above.

About Platinum

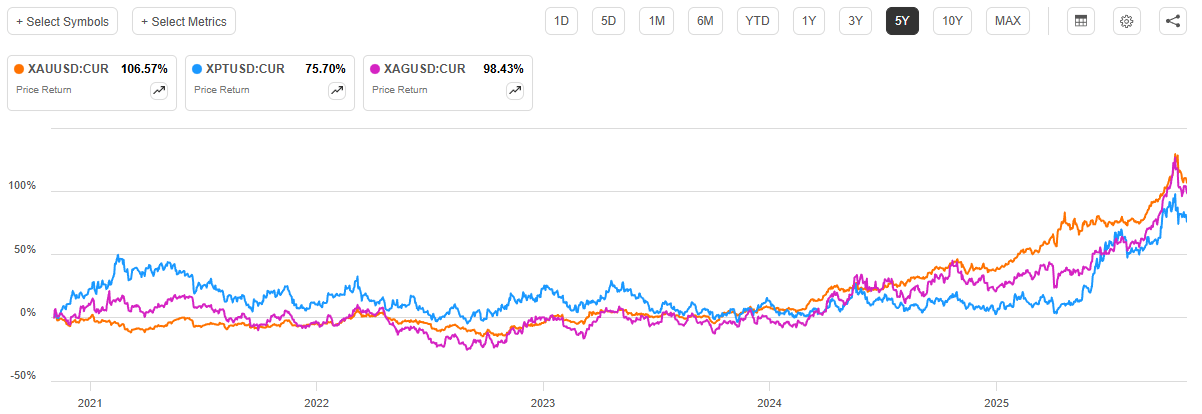

Platinum is generally considered to be both a precious metal and an industrial metal, so it does not perform exactly the same as gold. However, according to APMEX, a precious metals dealer, the price of platinum does correlate more strongly with gold than with silver. This would suggest that investors who already own a lot of gold may not obtain nearly as much diversification from adding platinum to their portfolios as investors who own a lot of silver. However, we do still see a strong correlation between platinum, gold, and silver prices. Seeking Alpha provides this chart for the five-year period that ended on November 4, 2025:

Seeking Alpha

Over this particular five-year period, gold rose 106.57%, silver rose 98.43%, and platinum rose 75.70%. Thus, gold was the best performing of the three metals over the period. However, we are looking for the correlation between the three metal prices, and it does appear to exist. For example, we can see that whenever gold rises, both silver and platinum follow soon after it.

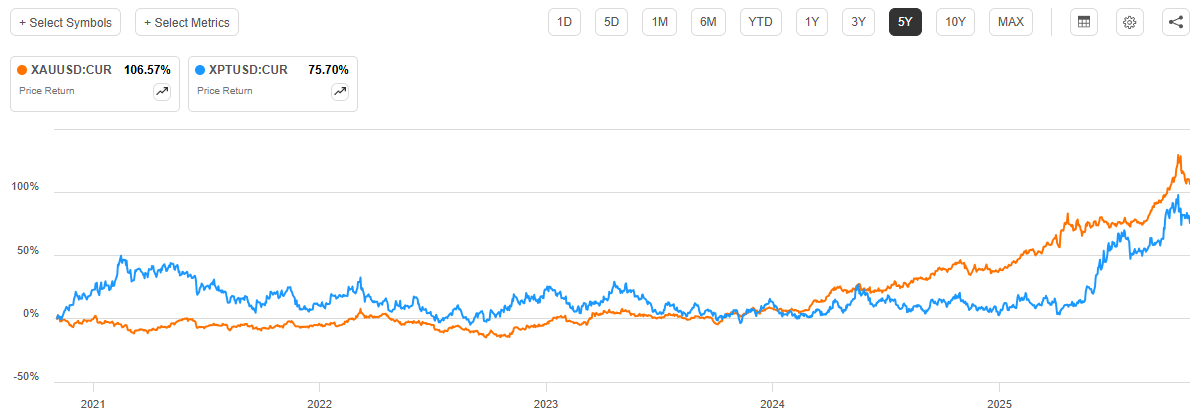

If we remove silver from the chart, we get this:

Seeking Alpha

Once again, we can see that platinum prices typically rise whenever gold prices rise and decline whenever gold prices decline. However, we can also see that platinum’s price movements tend to be more pronounced. Whenever it rises, it moves upwards more rapidly than gold and also declines more than gold. In short, it trades with a correlation to gold but with more volatility.

Much like silver, platinum has a number of uses in industry. Swiss America, an investment advisory firm in Phoenix, Arizona, provides a few of these uses in a blog post on its website. These uses include producing catalytic converters for cars, the manufacturing of pacemakers, the treatment of cancer, and as a catalyst in various chemical processes. Platinum is also used in the manufacture of hydrogen fuel cells and other next-generation batteries that could be used in electric vehicles. As such, economic conditions can have a larger impact on platinum prices than on gold. In particular, if demand from industry rises, then platinum prices can also rise independently of gold prices.

As PPLT is designed to track the performance of platinum, investors should have expectations of where platinum prices will head before considering an investment in the fund. The fund does not pay a distribution, so the only returns that the fund provides come directly from the movement of platinum prices. Investors who believe that platinum prices will rise may wish to consider this fund as a potential alternative to buying physical platinum. Similarly, investors who expect platinum prices to decline will probably have an easier time shorting PPLT than they would trying to short physical platinum.

Conclusion

In conclusion, the abrdn Physical Platinum Shares ETF is an exchange-traded fund that aims to track the spot price of platinum, minus the fund’s 0.60% expense ratio. The fund’s only asset is physical platinum that it holds title to, so the counterparty risks here should be lower than the counterparty risks of some other precious metals funds. There are very few funds out there that aim to track the price of platinum, and PPLT is by far the largest of them, but it also has the highest expense ratio. The fund does not use leverage, nor does it use derivatives, so it should be fine for both short-term and long-term investors.

This article answers these three main questions about PPLT:

- Does PPLT hold anything other than physical platinum?

- Is PPLT’s expense ratio reasonable when storage costs are taken into account?

- How do PPLT and platinum itself correlate with other precious metals like gold and silver?

Editor’s note: This article is intended to provide a general overview of the ETF for educational purposes only and, unlike other articles on Seeking Alpha, does not offer an investment opinion about the ETF.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}