As economies grow, so does the demand for commodities, and eventually the demand outstrips supply. That leads to rising commodity prices, but the commodity producers don’t initially respond to the higher prices because they’re unsure whether they will last. As a result, the gap between demand and supply continues to widen, keeping upward pressure on prices.

Eventually, prices get so attractive that producers respond by making additional investments to boost supply, narrowing the supply and demand gap. High prices continue to encourage investment until finally, supply overtakes demand, pushing prices down. But even as prices fall, supply continues to rise as investments made during the boom years bear fruit. Shortages turn to gluts and commodities enter the bearish part of the cycle.

There have been multiple commodity super cycles throughout the course of history. The most recent one started in 1996 and peaked in 2011, driven by raw material demand from rapid industrialization taking place in markets like Brazil, India, Russia and especially, China.

We can talk about the cyclical nature of commodities in general, but we can also pick certain commodities to see whether they are on the upswing or downswing.

Sprott recently did that, pointing out that A new copper supercycle is emerging, built on several rising geopolitical and market trends, including electrification, national security concerns, environmental policy, supply constraints and deglobalization.

We agree. Below are five reasons why we are entering the next copper supercycle.

Demand surge

Copper is one of the most important metals with more than 20 million tonnes consumed each year across a variety of industries, including building construction (wiring & piping,) power generation/ transmission, and electronic product manufacturing.

In recent years, the global transition towards clean energy has stretched the need for the base metal even further.

Simply put, electrification doesn’t happen without copper, the heartbeat of the global energy economy.

Along with the usual applications in construction wiring and plumbing, transportation, power transmission and communications, there is now added demand for copper in electric vehicles and renewable energy systems.

Millions of feet of copper wiring will be required for strengthening the world’s power grids, and hundreds of thousands of tonnes more are needed to build wind and solar farms. Electric vehicles use triple the amount of copper as gasoline-powered cars. There is more than 180 kg of copper in the average home.

Additional copper is being demanded by the electrification of public transportation systems, 5G and AI.

Supply crunch

However, some of the world’s largest mining companies, market analysis firms and banks, are warning that by 2025, a massive shortfall will emerge for copper, which is now the world’s most critical metal due to its essential role in the green economy.

The deficit will be so large, The Financial Post stated, that it could hold back global growth, stoke inflation by raising manufacturing costs, and throw global climate goals off course.

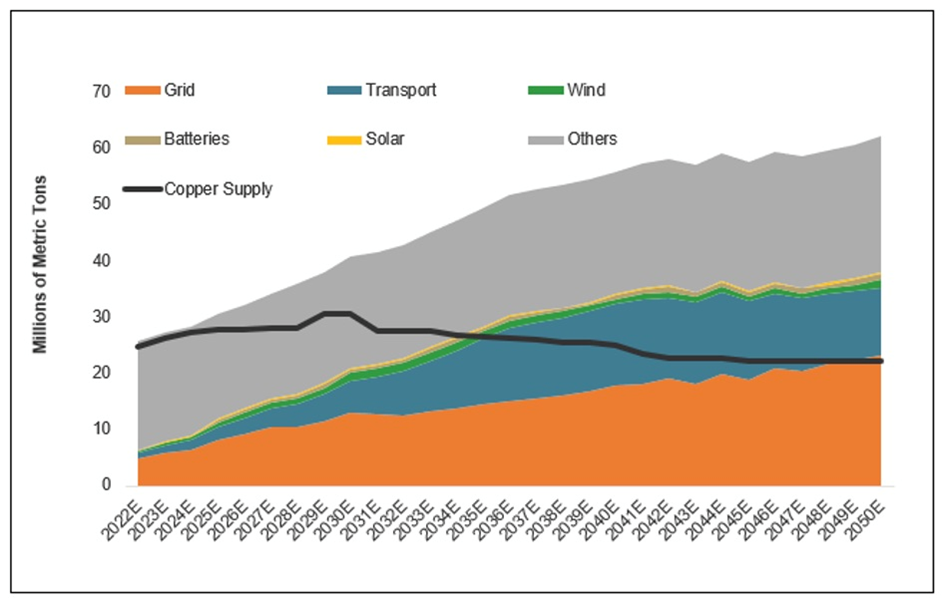

The graph below shows supply not keeping up with demand. Two reasons identified by Sprott: developing a new copper mine is lengthy and expensive, often taking over a decade from exploration to production; and the mining sector has seen long periods of underinvestment, when low copper prices meant reduced exploration budgets and fewer discoveries.

There has also been an overdependence on mergers and acquisitions. It’s much easier for a copper mining company to increase its reserves by purchasing a smaller company (and its reserves), than dedicating capital to greenfield exploration, which is expensive and risky.

According to Sprott, relying on M&A over new discoveries may slow the industry’s supply response to price signals and lead to prolonged market tightness, supporting a bullish outlook for the copper market.

Source: BloombergNEF Transition Metals Outlook 2023. The black line represents supply and the shaded areas represent demand. Demand is based on a net-zero scenario, i.e., global net-zero emissions by 2050 to meet the goals of the Paris Agreement.

The degree to which the industry has failed to bring on new mines is evident in a new study by the University of Michigan and Cornell University. The researchers found that copper can’t be mined fast enough to keep up with current US policy guidelines to make the transition from fossil-fueled power and transportation to electric vehicles and renewable energies.

For example the Inflation Reduction Act calls for 100% of new cars to be electric vehicles by 2035.

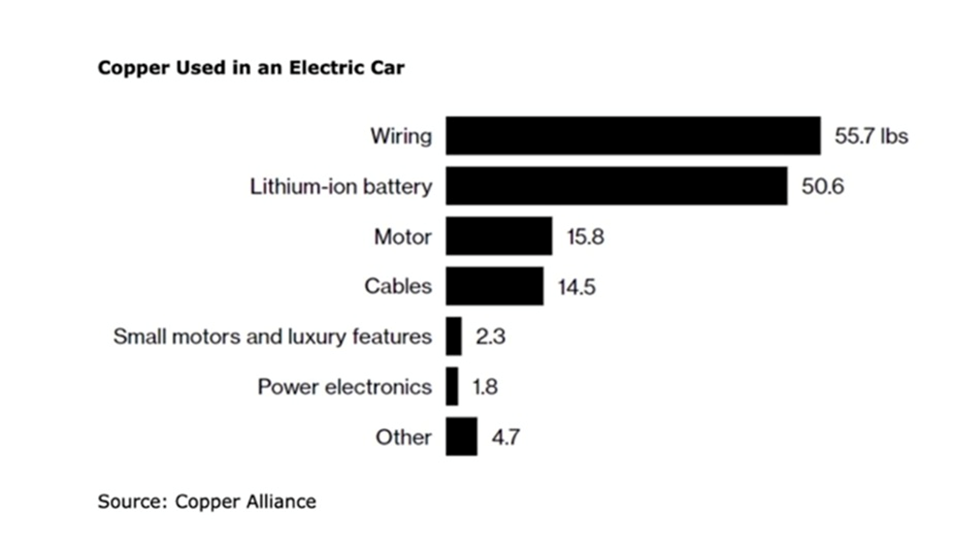

“A normal Honda Accord needs about 40 pounds of copper. The same battery electric Honda Accord needs almost 200 pounds of copper. Onshore wind turbines require about 10 tons of copper, and in offshore wind turbines, that amount can more than double,” said Adam Simon, co-author of the paper, published by the International Energy Forum (IEF). “We show in the paper that the amount of copper needed is essentially impossible for mining companies to produce.”

How impossible? The researchers found between 2018 and 2050, the world will need to mine 115% more copper than has been mined in all human history to 2018. This would meet our current copper needs and support the developing world without considering the green energy transition.

To electrify the global vehicle fleet requires bringing into production 55% more new mines. Between 35 and 195 large new copper mines would have to be built over the next 32 years, at a rate of up to six mines per year. In other words, impossible. In heavily regulated environments like the United States and Canada, it can take up to 20 years to build one mine from scratch.

Instead of fully electrifying the US fleet of vehicles, Simon suggests focusing on manufacturing hybrid vehicles, which require far less copper than electric vehicles — 29 kg vs 60 kg.

Going this route would not require major grid improvements and would have almost as large an impact on reducing CO2 emissions, the study found. Also, the likelihood of finding the copper needed to make hybrids is much greater than for electric vehicles.

Nearly 600,000 tonnes of copper supply didn’t come to market last year due to the Panama government’s closure of Cobre Panama, and a strike at the Las Bambas copper mine in Peru.

Anglo-American says its 2024 Chilean production will disappoint, at between 210,000 and 270,000 tonnes owing to head grade declines and logistical issues at its Los Bronces mine. (Goehring & Rozencwajg)

Chile’s copper output has been dented by a long-running drought in the country’s arid north. Codelco’s 2023 production was the lowest in 25 years. Chile in April registered its lowest month of copper production in more than a year, concerning for the world’s largest copper producer. Mines produced 6.7% less than in March and 1.5% less that April 2023.

Resource nationalism

The term “resource nationalism” is loosely defined as the tendency of people and governments to assert control, for strategic and economic reasons, over natural resources located on their territory.

While it presents opportunities for those in less developed countries to seek profit from their natural resources, state ownership can exacerbate the instability of the world’s critical minerals supply.

The Sprott report notes that [export] bans and tariffs, political instability and rising resource nationalism in copper-producing regions can disrupt supply chains and cost structures, leading to price spikes.

Deglobalization and rising geopolitical tensions increase dependence on local supply chains and ramp up military expenditures, spurring copper demand.

Two recent examples of copper resource nationalism took place in Peru and Panama.

The world’s second-largest copper producer in 2023 was racked by protests owing to a change of government. Last November, a strike at the Las Bambas, copper mine threatened ~250,000 tonnes of annual production.

Also late last year, the government of Panama ordered First Quantum Minerals to shut down its Cobre Panama operation, removing nearly 350,000 tonnes of copper from global supply.

Environmental concerns

The transition to clean energy has the cleanup of air pollution as its goal. Copper is one of the most important metals needed to push this transition, and yet environmental concerns often get in the way of new mines.

“Copper miners face stringent environmental regulations related to land use, pollution control and conservation. These potentially delay new projects,” states the Sprott report.

In a recent article, Barron’s points to the National Environmental Policy Act as a piece of legislation that makes the permitting process for major mining and energy infrastructure projects difficult to navigate. While the Biden administration and Congressional leaders are trying to reform the permitting process, Barron’s notes it won’t help the mining projects that entered permitting before the new one- to two-year time limits were imposed. This includes the Resolution copper mine in Arizona, the Rhyolite Ridge lithium-boron project, and the Stibnite gold project.

Inflation

A rally in May carried copper prices to a record high of $5.20/lb. Despite a recent pullback, prices are 13% higher year-to-date amid speculative bets of looming shortages. (Trading Economics)

The Federal Reserve this week froze interest rates at the current 5.25-5.5%, and said there would likely only be one quarter-point interest rate reduction by year’s end instead of two. Inflation dropped two-tenths of a percentage point in May (3.6%) compared to April (3.4%) — still a long way from the Fed’s 2% target.

According to gold and copper bull Peter Schiff, High inflation and a supply shortage are conspiring with increased demand for electric vehicles, a boom in renewable energy tech, and an AI bubble to keep the price going up even without the flood of speculative money.

Schiff believes that even if impractical “net zero” targets are revised down to more realistic figures, the demand will still be there, and the current supply squeeze and inflationary pressures are here to stay…

To avoid a banking and commercial real estate crisis, the Fed will have no choice but to cut interest rates at some point. This will invite a new torrent of inflationary expansion as the Fed ignores the pressure cooker that its policies helped create.

Conclusion

All of the above can only mean one thing for copper: higher prices.

We already mentioned the shutdown of Cobre Panama, a major strike in Peru, and production misses in Chile contributing to supply concerns.

As we reported in April, all four of Codelco’s megaprojects have been delayed by years, faced cost overruns totaling billions, and suffered accidents and operational problems while failing to deliver the promised boost in production, according to the company’s own projections.

There are also concerns about Zambia, Africa’s second largest copper producer, where drought conditions have lowered dam levels, creating a power crisis that threatens the country’s planned copper expansion.

Ivanhoe Mines reported a 6.5% quarterly drop in production at the world’s newest major copper mine, Kamoa-Kakula in the DRC.

The tightness of the copper concentrate market has been reflected in treatment and refining charges plummeting from over $90 per tonne to below $10/t. This drastic reduction compelled Chinese smelters, responsible for around half of global refined copper production, to consider a 10% production cut.

Meanwhile, copper demand continues to increase.

The graph below shows the demand for copper to 2050 is greater than all of the copper produced over the course of human history.

While prices have been reaching among the highest levels of the past five years, some believe that copper, and other commodities, have never been more undervalued.

We know one thing for sure. The case for all commodities rests upon the US dollar. Once the Fed starts cutting interest rates, the dollar will weaken and the entire commodities complex will strengthen.

Investing in juniors has historically been a good way to leverage rising metals prices.

Juniors own the world’s future mines – they help the majors to replace the ore that they are constantly depleting in their operating mines, thereby helping to overcome the copper supply shortfall we know is coming.

Legal Notice / Disclaimer

Ahead of the Herd newsletter, aheadoftheherd.com, hereafter known as AOTH.

Please read the entire Disclaimer carefully before you use this website or read the newsletter. If you do not agree to all the AOTH/Richard Mills Disclaimer, do not access/read this website/newsletter/article, or any of its pages. By reading/using this AOTH/Richard Mills website/newsletter/article, and whether you actually read this Disclaimer, you are deemed to have accepted it.

Any AOTH/Richard Mills document is not, and should not be, construed as an offer to sell or the solicitation of an offer to purchase or subscribe for any investment.

AOTH/Richard Mills has based this document on information obtained from sources he believes to be reliable, but which has not been independently verified.

AOTH/Richard Mills makes no guarantee, representation or warranty and accepts no responsibility or liability as to its accuracy or completeness.

Expressions of opinion are those of AOTH/Richard Mills only and are subject to change without notice.

AOTH/Richard Mills assumes no warranty, liability or guarantee for the current relevance, correctness or completeness of any information provided within this Report and will not be held liable for the consequence of reliance upon any opinion or statement contained herein or any omission.

Furthermore, AOTH/Richard Mills assumes no liability for any direct or indirect loss or damage for lost profit, which you may incur as a result of the use and existence of the information provided within this AOTH/Richard Mills Report.

You agree that by reading AOTH/Richard Mills articles, you are acting at your OWN RISK. In no event should AOTH/Richard Mills liable for any direct or indirect trading losses caused by any information contained in AOTH/Richard Mills articles. Information in AOTH/Richard Mills articles is not an offer to sell or a solicitation of an offer to buy any security. AOTH/Richard Mills is not suggesting the transacting of any financial instruments.

Our publications are not a recommendation to buy or sell a security – no information posted on this site is to be considered investment advice or a recommendation to do anything involving finance or money aside from performing your own due diligence and consulting with your personal registered broker/financial advisor.

AOTH/Richard Mills recommends that before investing in any securities, you consult with a professional financial planner or advisor, and that you should conduct a complete and independent investigation before investing in any security after prudent consideration of all pertinent risks. Ahead of the Herd is not a registered broker, dealer, analyst, or advisor. We hold no investment licenses and may not sell, offer to sell, or offer to buy any security.

{kind=link}