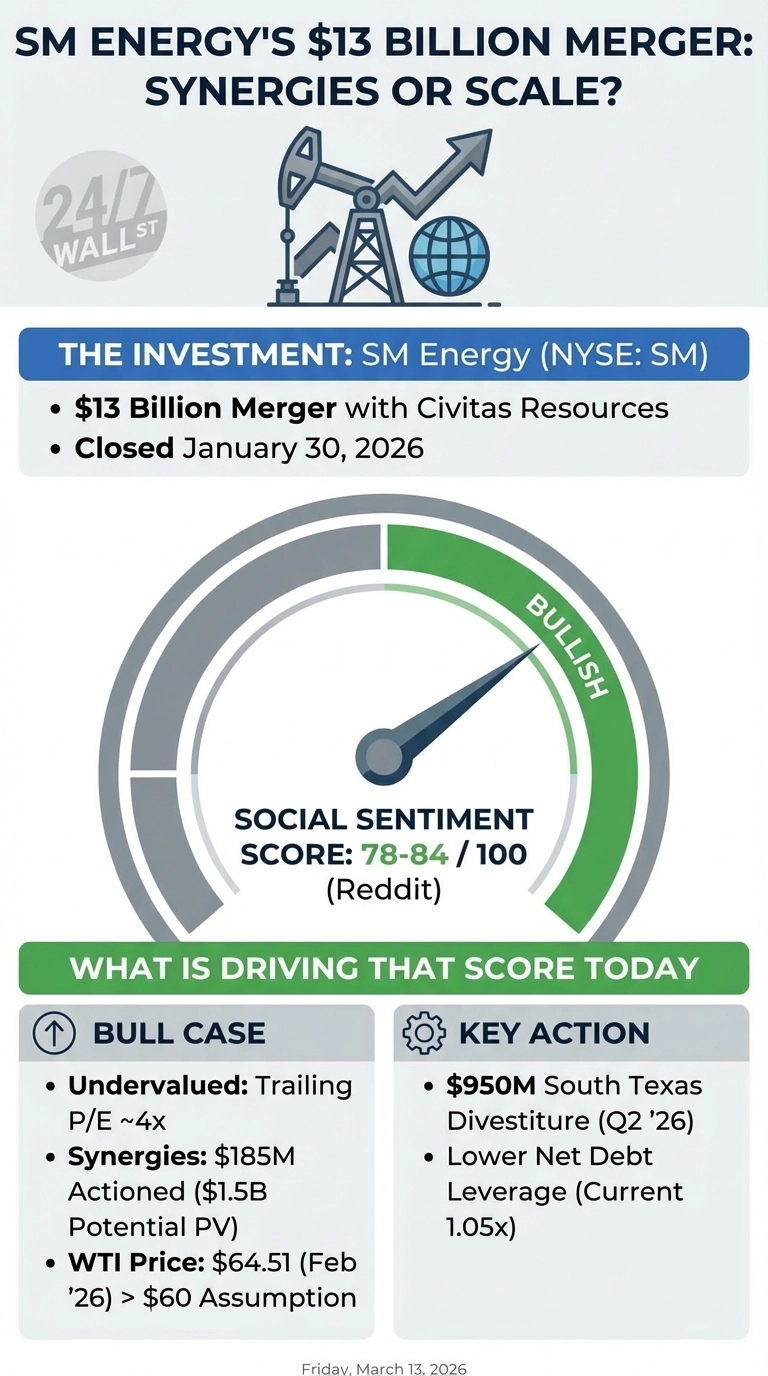

A prominent independent energy company based in Denver, Colorado, SM Energy (NYSE:SM) has climbed 37% year-to-date as retail investors weigh whether its $12.8 billion merger with Civitas Resources, which was successfully closed on January 30, 2026, is a genuine scale play or a leverage trap. Reddit sentiment sits at 78 to 84 out of 100, firmly in bullish territory, even after SM missed Q4 estimates by a wide margin.

As far as the numbers go, investors take note as the Q4 miss was real. Kicking off the red flag is EPS coming in at $0.83 against a $0.73 estimate, while revenue of $705 million missed the $846 million consensus by 8%. The culprit was oil prices, which fell 16% year over year to $58.17 per barrel. Production held up fine at 206.8 MBoe/d, in line with guidance.

Why r/WallStreetBets Is Calling SM Energy Undervalued

Discussion on Reddit is concentrated in r/wallstreetbets, where a post titled “$750k on SM Energy (Undervalued US Oil Producer)” has drawn 66 upvotes and 98 comments. The high comment-to-upvote ratio signals genuine debate, not just passive agreement.

$750k on SM Energy (Undervalued US Oil Producer)

by u/unknown in wallstreetbets

The bull case driving that discussion rests on three concrete factors:

- SM trades at a trailing P/E of roughly 4x, unusually cheap for an E&P with a multi-basin asset base

- Synergies of $185 million have already been actioned against a $200-$300 million target, with management citing up to $1.5 billion in present value, nearly 30% of market cap

- WTI at $64.51 in February 2026 sits above SM’s $60/barrel planning assumption, giving the 2026 free cash flow forecast a cushion

SM Energy’s Leverage Is the Real Question

CEO Beth McDonald framed the merger around three priorities: “integrate, execute, bolster.” The bolster part matters most to skeptics. Net debt leverage sits at 1.05x, with a target to bring it to the low 1s. The $950 million South Texas divestiture, expected to close in Q2 2026, is the clearest near-term lever for that goal.

Outperforming the Sector, but the Gap Is Narrowing

SM has outpaced Devon Energy (NYSE:DVN) year-to-date, with SM up 37% versus Devon’s 25%, while the broader E&P sector, as measured by the SPDR S&P Oil & Gas Explore & Production ETF (NYSEARCA:XOP), is up 30% year-to-date, meaning SM’s outperformance is real but not dramatic. The divestiture close and Q1 production results will be the next concrete test of whether the merger thesis is delivering or just scaling up risk.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}