BNP Paribas Capital Introduction survey on alternative investments provides a snapshot of hedge fund investor sentiment for 2024. Read the findings below or listen to the highlights on our Great Expectations podcast.

Introduction

In response to the new rates regime set by global central banks, investors have the highest hedge fund return expectations in more than 10 years and plan to grow their hedge fund portfolio in the year ahead. Credit strategies remain the most sought after in 2024, the withdrawal from China slows down and multi managers remain at the forefront of investors’ minds.

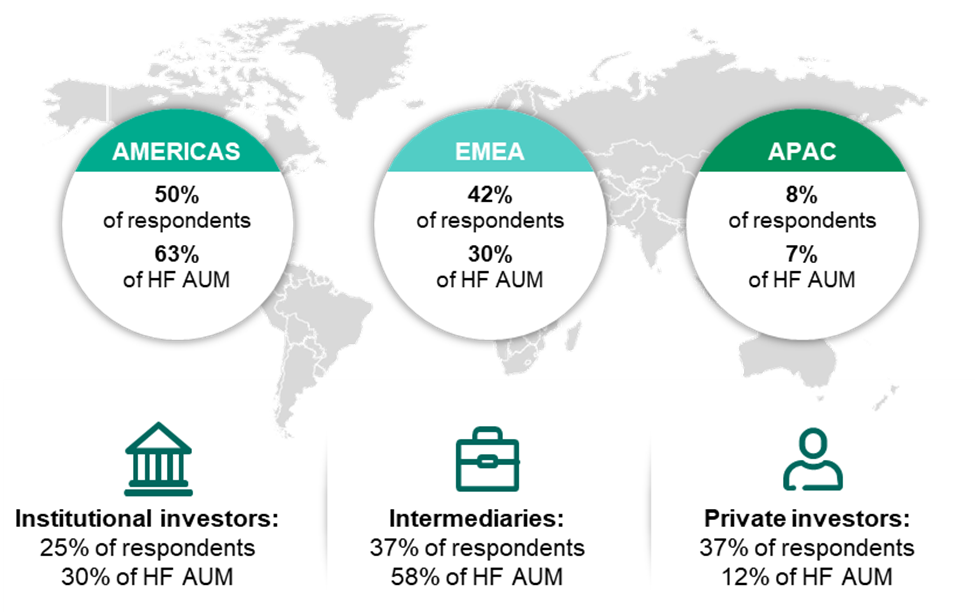

These are the findings of the latest Alternative Investment Survey: “Great expectations: investors bet on alpha in the new rates regime”, released by the BNP Paribas Capital Introduction team. Each year it surveys its global allocator community to discuss and forecast key trends in the hedge fund industry. This year, 238 allocators that manage or advise on US$1.2 trillion in hedge fund assets (“HF AUM”) participated in the survey in December 2023 and January 2024, representing around a third of the industry.

Hedge fund performance: 2023 flipped 2022 on its head

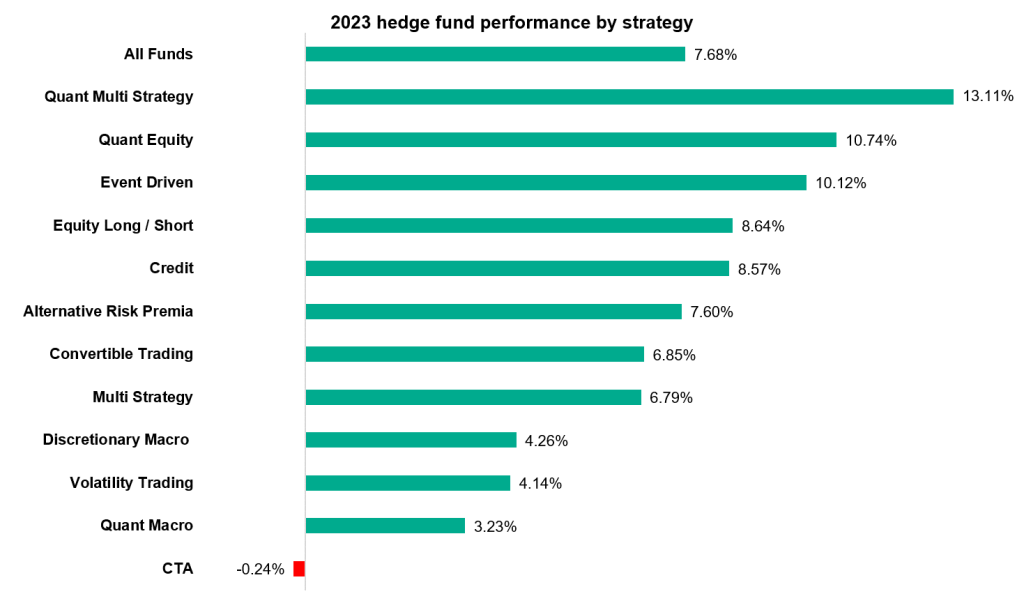

In 2022 the market struggled in the red with the MSCI World down almost 18%. Hedge funds protected capital, meaningfully outperforming the market and were flat on average for the year. Discretionary macro and CTA funds topped the charts in 2022, while equity long/short dragged on investors’ portfolios. In 2023, the market soared with the MSCI World returning 24%, whilst hedge funds returned 7.68%.

It was far from one way traffic though, with investors navigating inflationary pressures, rising rates, an unexpected banking crisis, the rise of artificial intelligence (AI), the magnificent seven dominance, hard and soft landings and increased geopolitical events. Equity long/short focused on Americas or TMT led the way for most of our responding investors as their best performing hedge fund strategy – precisely what had struggled most of the year before.

On the other hand, discretionary macro and CTAs were the worst performers in our respondents’ portfolios. Quant equity and quant multi strategy, were the best performers on average across the industry. It is worth highlighting that over the full 24 month period (2022 and 2023), the average hedge fund outperformed global equity markets by 5.84%

Investors back hedge funds as we shift into the alpha era

For most of the past decade, hedge funds faced headwinds to generate alpha as a result of zero interest rates and subdued volatility. As highlighted in a research report we conducted last October, hedge funds perform well in periods of high stable rates. However, during periods when rates are rising, the broader industry does not adapt fast enough and hence there is a lag in producing higher returns.

As a consequence, the recent multiple central bank rate rises did no short-term favours to hedge funds in 2023 with respondents reporting that their hedge fund portfolios returned 6.67%, still 1.5% shy of their target return.

Hedge fund expected returns versus the risk free rate has been keenly discussed by global allocators and the Capital Introduction team was not surprised to learn that responding investors have pushed up their return targets by 161bps since 2022 from 7.45% to 9.06%; the highest level in a decade. Investors are anticipating improved returns from their hedge fund portfolios as they expect us to move into a high but more stabilised rate environment: the alpha era.

Perhaps unsurprising given (1) hedge fund underperformance versus their expected returns; (2) investors taking profits from their hedge funds to rebalance their portfolios following 2022 outperformance versus other investments; and (3) five percent risk free rates, last year saw up to US$100 billion of net outflows from hedge funds1; leaving overall industry assets somewhere between US$3.5 trillion and US$4 trillion as reported by various industry data providers2.

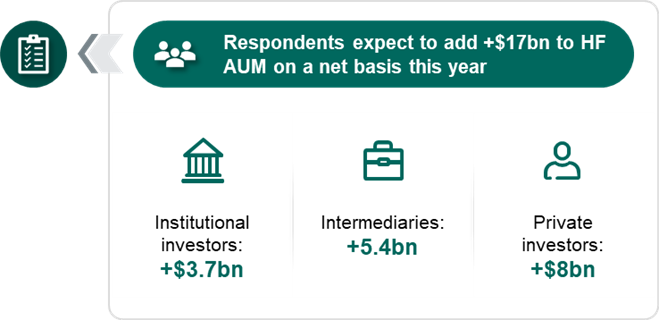

Nevertheless, for the year ahead, almost half of our respondents are looking to add to hedge funds. Investors in our survey expect to add $17bn on a net basis in 2024, up 70% from the $10 billion net they added in 2023. The much anticipated alpha regime is prompting investors to inject more alternative investments that have low or no correlation to global equities and bonds into their portfolios following the breakdown of the 60/40 asset allocation model in 2022.

For most of the last century, bonds’ low or negative correlation to stocks protected portfolios from stock market volatility. Unfortunately, this relationship tends to fall apart amid high inflation and our respondents are preparing for this!

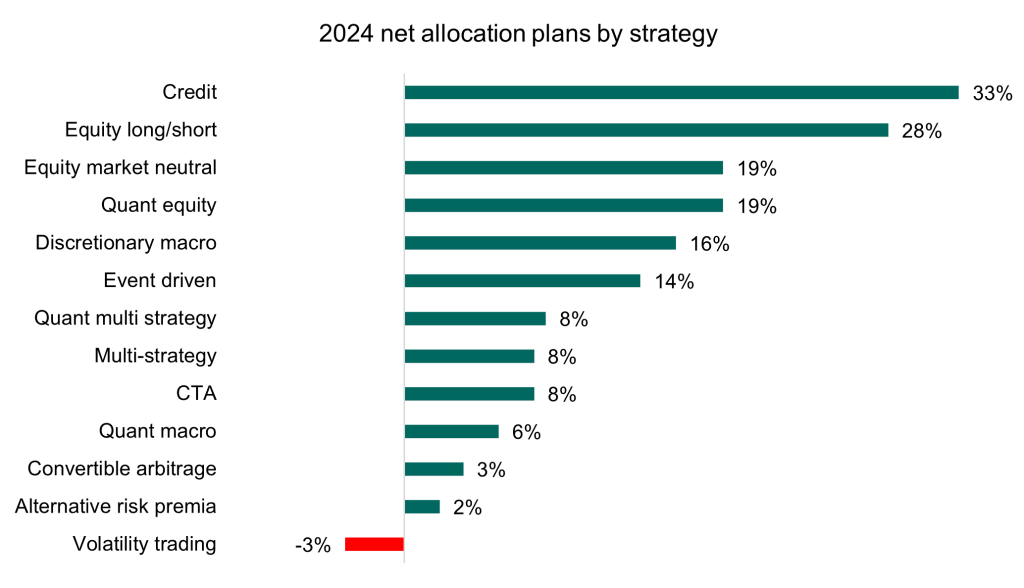

Credit remains the most sought after strategy in 2024

Continuing the trend from our survey last year, credit strategies remain the most sought after in 2024 with a third of respondents looking to add on a net basis. As predicated in our 2023 survey, credit was the number one strategy allocators added to last year; however, the BNP Paribas Capital Introduction team did not observe allocators investing as many dollars as they planned to.

This is evidenced by only 21% of survey respondents adding to credit in 2023, whereas in 2022 48% had intended to do so. Heightened interest rates are expected to further expose balance sheet weakness, creating an environment where credit hedge funds can strategically capitalise on short and distressed credit opportunities.

Additionally, as technicals tighten spreads while fundamentals simultaneously widen them, credit funds will also be well-positioned to exploit the increasing dispersion between strong and weak companies. The looming maturity wall, flurry of primary market activity and rising default rates, present an optimal landscape for these funds to build upon their strong 2023 performance.

China exodus slowing down in 2024

The world’s second largest economy has slowed down in recent years, following the Covid pandemic and the more recent crash in the property market. Last year, 42% of investors on a net basis pulled capital from China-focused hedge fund managers. This exodus of capital is expected to slow down in 2024, with only 6% of investors on a net basis looking to redeem.

Some investors believe the sentiment with respect to China has become too negative and this could present fruitful investment opportunities for alpha generators. Allocators looking to add to China, like the fact that many of their peers are avoiding the region and fund managers have reduced exposure, making it less crowded.

Identifying opportunities in companies that have minimal economic sensitivity is an area of focus while on the other hand, if policymakers double down on fiscal policy, particularly in segments like affordable housing, this should have a positive effect on consumer sectors.

Multi managers in the spotlight

The capital introduction team has noted two schools of thoughts emerging across the investor base around the future of the multi manager model. On one hand, some investors expect more consolidation of the hedge fund industry into multi manager platforms as well as acquisitions amongst multi manager platforms.

It follows that the war for talent will continue to be waged through increased payouts, there will be fewer independent launches, more fund closures and investors will battle for access resulting in further proliferation of restrictive liquidity and higher fees. On the other hand, some investors believe single managers will once again find their value proposition and expect a reversal of flows away from multi managers. These allocators question whether liquidity and fees are commensurate with returns and risk.

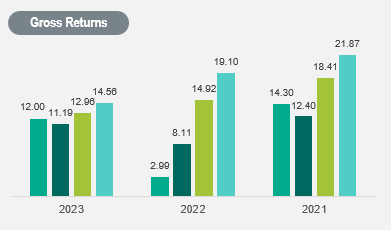

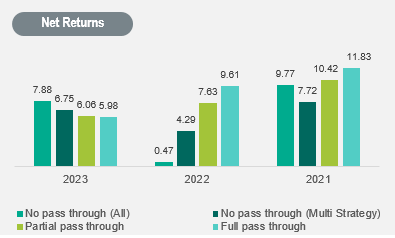

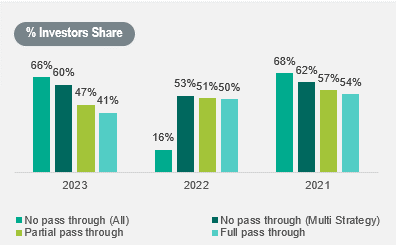

Our analysis shows that the investors’ share of return amongst pass through structures dipped below 50% while managers with no pass through fees outperformed in 2023 on a net basis reversing the trend from the previous two years. It is worth noting though that the three-year average investor share for no pass through structures is only 50% which was dragged by performance in 2022. Other concerns shared by these investors include position crowding and the potential for a systemic deleveraging event.

For more information, read our press release or contact our Capital Introduction team: dl.capintro@uk.bnpparibas.com.

Plan Managers")

{kind=link}