The year 2023 ended with a bang on the financial markets, with both equities and fixed income – in this column represented by S&P 500 and global government bonds – going through the roof.

A widely used benchmark for a balanced portfolio consisting of 60% equities and 40% bonds earned 10.2% during the fourth quarter alone, leading to a total gain of 17.4% for the year as a whole. This is more than many expected, as the consensus going into 2023 was that a recession would soon hit the markets.

In the alternatives universe, 2023 was the year of the niche strategies. While “mainstream alternatives” like private equity and real estate, to which most institutional investors have sizable allocations, had a hard time and delivered lackluster returns at best, niche strategies like ILS (insurance-linked securities) and forestry delivered outstanding returns. Sometimes, money does indeed grow on trees.

New benchmarks in this column

As mentioned in a previous column, I have been looking for new infrastructure and private equity benchmarks and have finally found suitable replacements.

I have chosen to use the eFront Insight database for infrastructure, private equity buyout, and venture capital. These indices consist of unlisted funds and are thus more representative of the results achieved by institutional investors. The disadvantage, however, is that these indices come out more slowly, meaning that at this point in time only the Q3 2023 results are available.

But before we dig into the numbers, I want to remind you of a few technical facts of importance. Most alternative investments, aside from liquid alternatives, are long-term investments. Evaluating performance over a single quarter has limited explanatory power. Due to the illiquid nature of the underlying investments, there is always a time lag between reported returns and public market returns.

Alternative investments are very heterogeneous in nature with huge dispersion, including at the manager level. The realized returns of an investor will most likely deviate from the benchmark-level returns.

(The column continues below this graph. Refresh page, if graph doesn’t show)

CTA, a sub-asset class from the hedge fund universe known for using trend-following models, suffered from the turnaround of both equities and fixed income following the softer CPI print in November and ended the year slightly negative. 2023 was not an easy year for trend followers with two major moves: The first one being the regional banking crisis in the US in March, and the second one being the equity and fixed income rally fuelled by the inflation surprise in Q4.

According to this research note from AlphaSimplex, if the two worst days in March 2023 were excluded, the performance of the SG Trend Index would have been close to 10% points (!) better.

Slower strategies performed generally better than faster strategies during 2023, with March and December being the exceptions to this rule as the faster models adapted quicker to the changing markets. Besides these two periods, the faster models were being pulled in two opposing directions at once and suffered more.

Another factor explaining performance differences is the contracts traded, where some underlying assets performed better than others. Positive performance can be attributed to, for example, exposure to soft commodities like cocoa and sugar and emerging market currencies like MXN and BRL. Strategies that did not have exposure to these assets missed some great opportunities. Typical mainstream contracts like WTI Oil and various fixed-income contracts were not profitable for many strategies.

It remains to be seen whether 2024 will be a good year for CTA or not, but as of the time of writing, the market is off to a pretty good start. CTA has at least some tailwinds from the higher base rates on the collateral.

Infrastructure, as represented by the eFront Insight Research index, an index consisting of unlisted funds, showed resilience during the first three quarters of the year with an accumulated return of 5.3%. At the time of writing this column, data for the fourth quarter had not yet been published. The third quarter return was not impacted by the free fall of the stock price of the renewable energy darling Ørsted (-40% in Q3 2023) after the company announced impairments due to challenging market conditions. This relates to development projects of offshore wind parks that are negatively impacted by supply-chain issues, increased interest rates, and a lack of favorable progress in Investment Tax Credit (ITC) guidance.

This highlights, once again, that it is important to take a nuanced view on the infrastructure asset class as, for example, transportation assets have been performing quite well.

Real Estate, as represented by the NCREIF Property Index, an unlevered index of directly held properties in the US, continued downwards and ended the quarter with a loss of 3.02%, bringing the full-year return down to -7.94%. Office, making up 23% of the index, was the main culprit, with a loss of -17.63% for the year. Hotels were the only sub-asset class with a positive return of 10.31% for the year.

MSCI Real Assets reported that global deal activity in 2023 fell by almost 50% relative to 2022, the lowest level in a decade. According to the MSCI report, buyers and sellers must become more aligned on pricing amid the higher-rate environment for deal activity to recover.

Timberland ended the year with strong performance and posted positive returns of 4.3% in the fourth quarter, bringing the full-year return to 9.5%. Before we get too excited about the strong fourth quarter, it is worth noting that this is a known seasonality in the timberland index as most assets are appraised by third-parties during the fourth quarter. But still, the performance is very impressive.

Farmland also ended the year on a solid note with a quarterly return of 2.3%, bringing the full-year return to 5.0%. Most of the year-to-date performance was driven by annual croplands, while permanent croplands (fruit plantations etc.) did less well.

Private Equity was a tale of two markets with Buyouts up and Venture Capital down both during Q3 2023 and year-to-date. At the time of writing, the numbers for Q4 2023 were unfortunately not out yet due to their illiquid nature, but my expectation is the same for Q4 with Buyouts outperforming Venture Capital.

While things are still not rosy in private equity land, there were some bright spots, as Pitchbook data showed an increase in exits in US PE during Q4 2023. However, activity is still substantially down compared to the post-Covid era, extending the average holding period of portfolio companies. According to PitchBook, the median age for PE portfolio companies in the US was 4.2 years in 2023, an 11-year high, while the median age for exited companies last year was an all-time high of 6.4 years. It remains to be seen whether the Q4 2023 success stories are a predictor of a better exit environment in 2024.

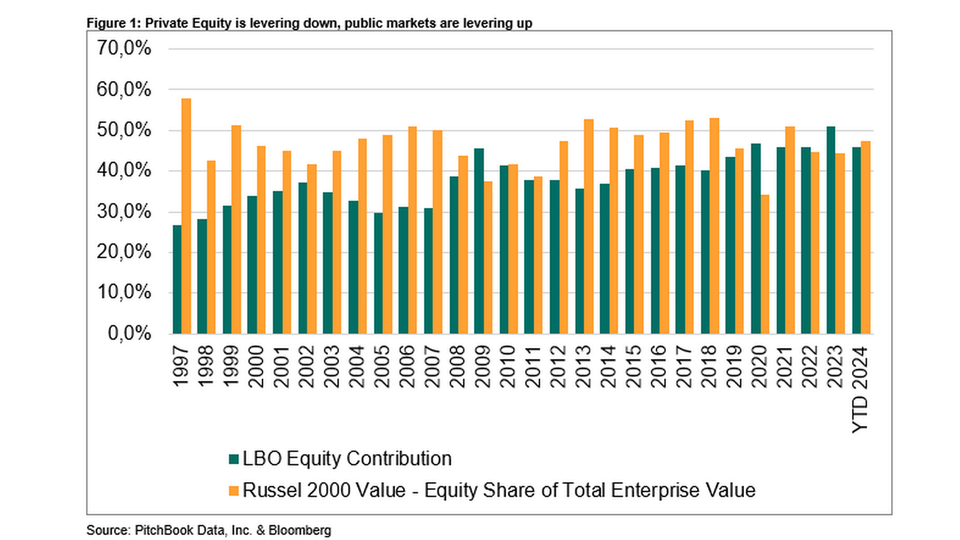

The higher interest rates are often named as one of the main culprits for the slowdown in deal activity. Another impact of higher interest rates might be that PE funds use more equity and less debt nowadays. This has, however, been a trend for many years. As shown in Figure 1 below, the average LBO (leveraged buyout) equity contribution has increased from less than 30% in 1997 to more than 50% in 2023. At the same time, the equity share of the total enterprise value of companies in the Russel 2000 Value index (calculated as 1 – Total Debt to EV) has decreased from close to 60% in 1997 to approximately 45% in 2023.

It seems like the old PE critic saying that PE is just levered small-cap value stocks needs updating. If this trend continues, one might call small-cap value stocks levered PE.

Of course, this back-of-the-envelope calculation is not very scientific, and differences in sector composition can play a role. On the other hand, the typical buyout is leveraged the most at the very beginning (which is what is shown here) and is de-leveraged over time, while the leverage in listed companies does not follow this pattern.

The increase in equity contribution also places greater demands on GPs as financial engineering is no longer enough to generate value, although those who have specialized in their field and are masters of operational excellence will still be able to create value for their investors.

The median EV/EBITDA multiple in buyout deals has decreased slightly but not substantially, as shown in Figure 2 below. This is good for existing PE investors but might also indicate that the current years will not be stellar vintages for new investors, although as highlighted in my last column, it is important to continuously make commitments, as trying to time them perfectly is futile.

Insurance-Linked Securities (ILS), often also referred to as “CAT Bonds” (catastrophe bonds), continued their strong performance and posted a gain of 3.8% for the Swiss Re Global CAT Bonds Index, bringing the total return for the full year to 19.7% – the strongest performance among the alternative asset classes covered in this column and the strongest year since the inception of the index, dwarfing the earlier record from 2007 where the index delivered 14.97%. The extraordinarily solid performance was driven by both higher spreads (e.g., insurance premiums), higher rates on collateral and a rebound of some CAT bonds that traded down in the aftermath of Hurricane Ian in late 2022 that were not as affected as initially thought – and of course, no major new catastrophes.

Even though spreads are coming down, market participants still say that “cat bonds remain a compelling asset class to include in a fixed income portfolio allocation. And not just for return optimization, but also risk diversification, given the low qualitative and quantitative correlation of cat bonds to most other traditional asset classes as well as little interest rate duration risk.”

Unless a major catastrophe occurs, ILS could be in for another very positive year – albeit not as positive as 2023 – as they are also profiting from the higher base rates.

Conclusion

There was high dispersion in the performance of alternative investments during 2023, with niche asset classes like ILS and timberland as the top performers. Other real assets, namely infrastructure and farmland, also fared quite well, with real estate being the odd one out with painful losses.

CTA, being famous for delivering crisis alpha, posted a small loss, mainly driven by a few trading days with some sharp reversals in interest rates following the banking crisis in March 2023 and again in Q4 2023 following the softer CPI print in November.

Private equity has been a tale of two markets this year, with buyouts delivering at least positive but not impressive returns and outperforming venture but lagging behind listed equities by a large margin. That said, this comes after a healthy outperformance in 2022.

As most institutional investors have their largest allocation to real estate and private equity and less (or none) to timber and ILS, the performance contribution to the overall returns was most likely more muted in 2023. However, it is still important to highlight the dispersion on the manager level, which can lead to substantially different outcomes than the benchmark returns.

Looking into the crystal ball for 2024, I am cautiously optimistic. However, there is great uncertainty, and the year may turn out to be volatile and characterized by low growth. High interest rates, tighter credit conditions, and increased cyclical and geopolitical risks, including deglobalization, could put markets under pressure.

If the US and Europe should end up in recession (something which is absolutely not certain); earnings in many portfolio companies will fall, affecting the valuation of private equity portfolio companies. In this scenario, parts of the core infrastructure universe, especially contracted and regulated assets, might be able to deliver positive returns, while the more cyclically sensitive assets, such as airports and ports, will likely be hit by falling volumes.

CTA/managed futures have the potential to provide positive returns as long as there are clear and persistent trends within shares, commodities, currencies and interest rates. They will also profit from higher base rates.

Given that alternative investments are long-term in nature and that there is a time lag in the benchmark, I will change the frequency of my columns to be semi-annual going forward. The next column will be published after summer when the Q2 numbers are out for most asset classes.

Christoph Junge is Head of Alternative Investments at Velliv, Denmark’s third-largest commercial pension company. He is a Chartered Alternative Investment Analyst with more than 20 years of experience in the financial industry in Denmark and Germany. He has worked with Asset Allocation, Manager Selection, as well as investment advice in, among others, Nordea, Tryg and Jyske Bank.

Besides working as a Head of Alternatives, Christoph teaches a top-rated course on Alternative Investments. Read more at http://www.christoph-junge.de

This publication is provided for informational purposes only and such information is not intended to be relied upon as a forecast, research or investment advice. All data is provided for informational purposes only and is not intended to be relied upon as investment, trading, accounting, financial or other advice, recommendations or decisions. The data is not provided as “Input Data” for the purposes of Regulation 2016/1011 of the European Parliament and of the Council (as amended or superseded from time to time) and may not be used as “Input Data”. You may not use or cause or permit others to use or consider any data in connection with an offer to sell, or solicitation of an offer to buy, any security. Velliv, Pension & Livsforsikring A/S makes no guarantee, representation or warranty and accepts no responsibility or liability as to the accuracy and completeness of the publication, nor for any trading decisions, damages or other losses resulting from, or related to, the information, data, analysis or opinions or their use. Any opinions contained in the publication are those of the Author at the time of the publication. Investment markets and conditions can change rapidly and as such the opinions shall not be taken as a statement of fact. Neither the information nor any opinion expressed herein constitutes a recommendation, offer or solicitation to buy or sell any securities or to adopt any investment strategy. Such information and opinions are subject to change without notice. Past performance is no guarantee of future results.

{kind=link}