")

Hispanolistic

Investment Thesis

As Bridge Investment Group (NYSE:BRDG) nears all-time lows, I believe the stock is now a compelling buy due to its well-diversified alternative investments across many asset classes ranging from real estate, credit, and renewable energy. The company has proven to be a well-managed asset manager and can navigate economic and credit cycles skillfully while protecting their core assets. I believe Bridge Investment Group provides a safe haven for investors as they are more attracted to alternative investments with a multifamily real estate focus. Thus, the stock’s dividend yield is likely sustainable and will provide shareholders with solid income and capital appreciation.

An Alternative Investment Manager

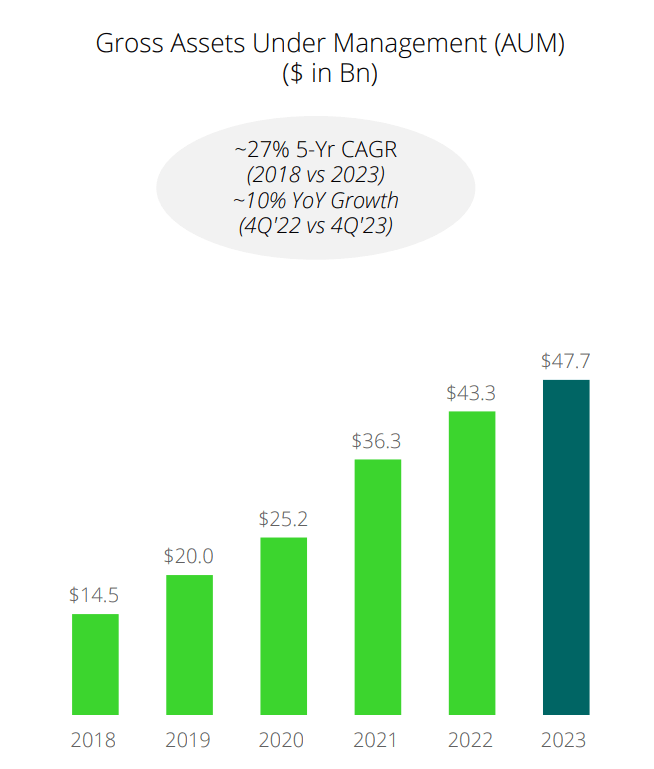

The company is an alternative investment manager with around $47 billion AUM as of December 31, 2023. According to the annual report,

Bridge combines its nationwide operating platform with dedicated teams of investment professionals focused on various specialized and synergistic investment platforms, including real estate, credit, renewable energy and secondaries strategies. Our broad range of products and vertically integrated structure allow us to capture new market opportunities and serve investors with various investment objectives.

The company typically takes in client money from “individual investors, which includes high-net-worth fund investors, fund investors who invest through a wirehouse relationship or an RIA family office, and institutional investors” (Annual Report, Page 14). This diverse investor base has proven to be sticky as AUM for Bridge Investment has grown from $14.5 billion in 2018 to $47.7 billion in 2023.

Investor Q4 2023 Presentation

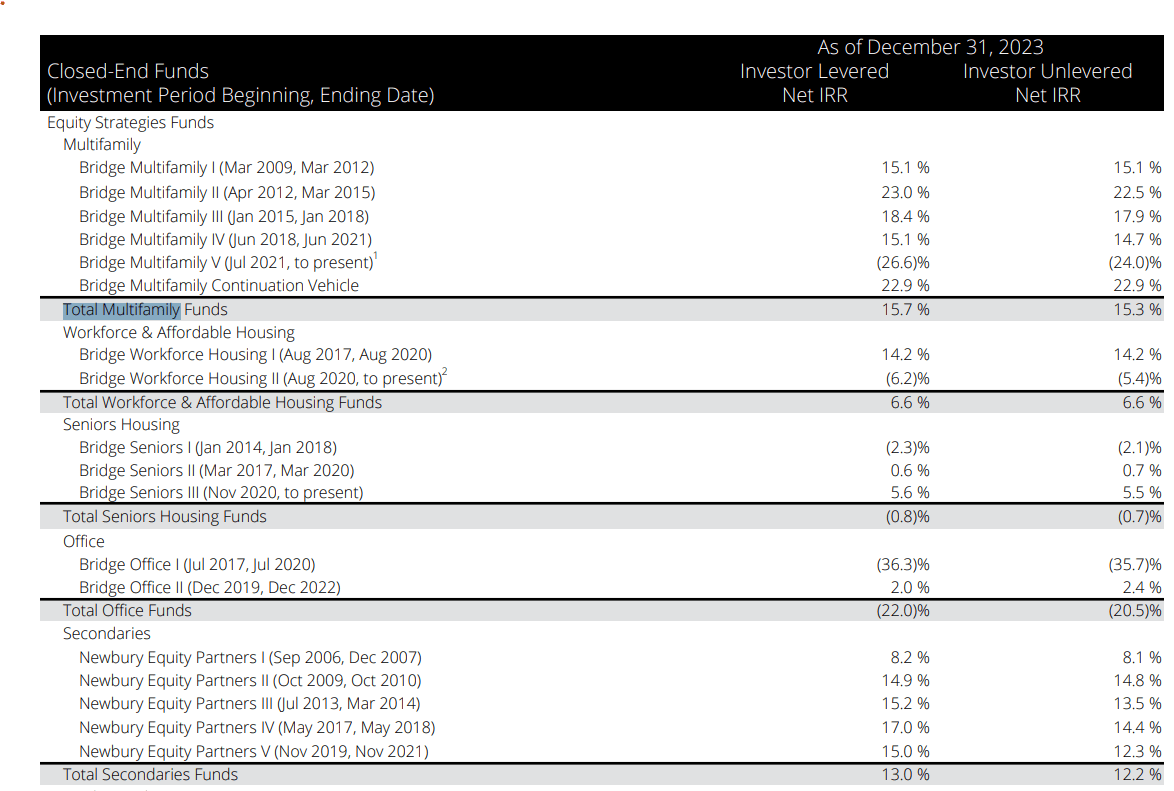

Investors can see that their track record of investing performance is strong and likely will continue as their management team has navigated economic cycles and the pandemic skillfully, growing their AUMs dramatically over the past few years. The investor presentation on page 13 shows that most multifamily real estate funds have unlevered returns of around 15%. Their single-family funds have returns of 16% and debt strategies of over 8%. I believe these numbers demonstrate their strong performance for clients, which explains why AUM has increased dramatically over the past few years. Despite this growth, the stock continues to decline which leads me to believe it is underpriced.

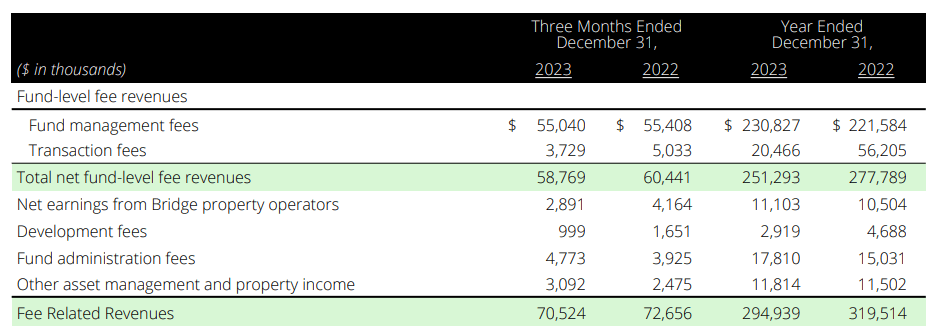

Like any other investment manager, the company makes most of its revenues through fund management fees. According to the annual report on page 57,

Our fund management fees are generally based on a defined percentage of total commitments, invested capital, or net asset value (“NAV”) of the investment portfolios that we manage. Generally, with respect to fund management fees charged on committed capital, fund management fees are earned at the management fee rate on committed capital and, beginning at the expiration of the investment period, on invested capital.

For 2023, fund management fees came in at $230 million, about 91% of sales. The remaining 9% of sales comes from transaction fees, which, per the annual report on page 57,

We earn transaction fees associated with the due diligence related to the acquisition of assets and origination of debt financing for assets. The fee is recognized upon the acquisition of the asset or origination of the mortgage or other debt. The fee range for acquisition fees is generally 0.5% to 1.0% of the gross acquisition cost of the investment or, in the case of development projects, the total development budget, and the fee range for debt origination is generally 0.3% to 1.0%.

Total net-level fund fee revenues were $251 million for 2023, a slight decrease from $278 million in 2022. Investors will also note that the company makes some revenues from its property operators and development fees. For the sake of simplicity, I think investors should just know that they are asset managers with revenues that correlate directly with AUM and investment performance.

Investor Presentation Q4 2023

Growing AUM, Sticky Client Base

As public markets become more volatile and approach lofty valuations, I believe institutional investors are looking to diversify away from public equities and into the alternative investments space. According to one report,

According to the forecast from industry analysts Preqin, the global alternative assets market will grow at an annualized growth rate of 8% between 2022-2028.

JPMorgan cites reasons for increased alternative investment demand in its research in this article,

JPMorgan issued its 2024 outlook for alternative investments. Overall, it sees continued growth for the asset class especially as economic and financial uncertainty remain elevated due to inflation, tight monetary policy, a decelerating global economy, geopolitical risks, and volatility in financial markets.

I think this trend will continue because volatility in the public markets may scare investors as they see their holdings drop significantly. However, in alternative investments, clients don’t deal with their daily volatility, which makes them psychologically more attractive to big investors. Alternative investments in real estate, credit, and renewable energy align with clients’ ESG mandates, so they are willing to invest money in Bridge Investment as their performance is solid and AUM continues to grow. A look at the investor presentation reveals that since the inception of their closed-end funds, the IRR has been around 15% in aggregate for multifamily real estate funds.

Investor Presentation Q4 2023

Some of the other funds have disappointing performance, but that has not stopped overall AUM from growing for Bridge Investment. Thus, I believe the track record shows management is adept at investing, can navigate markets well, and provides value for clients. Clients seem to be sticky as it may be hard to find another skilled investment manager and alternative investments are also hard to sell. According to PIMCO, a key characteristic of alternative investments is “longer lock-up of periods, meaning shares or interests may not be able to be redeemed/sold on a daily basis. This helps allow for exposure to less liquid assets”. The combination of illiquid investments and satisfactory performance makes Bridge Investments a unique opportunity as I expect AUMs to grow, and clients to stay.

Investor Presentation Q4 2023

Multifamily Focus Is Attractive

I think the company’s true talent is in the multifamily real estate sector, which has shown strong returns and will likely continue. So, I think the AUM for multifamily real estate should increase along with the fees they charge for managing client money.

The company describes its multifamily investments on page 10 of the annual report,

Our Multifamily investment platform focuses on assets in growth markets that we believe offer attractive risk-adjusted returns. Our senior executives have focused on multifamily investments for the past 30 years, including previous ventures. Our Multifamily platform generally targets markets with investments within metropolitan statistical areas, (“MSAs”), with household and employment growth rates that are projected to exceed national averages.

In the United States, we are seeing more demand for multifamily real estate which includes apartments, townhomes, and condos. The reason for this is traditional homes are extremely unaffordable at the moment. So, I think more demand for multifamily real estate will help fuel growth for Bridge Investment as their performance takes off from this growing trend.

However, near-term performance may be challenging for multifamily real estate. According to Freddie Mac,

As the overall economy slows leading to a softer labor market, multifamily demand is expected to remain positive but weaker compared with pre-pandemic rates. For 2024, our baseline forecast is for rent growth of 2.5% for the year, remaining slightly below the long-term annual average from 2000 to 2022 of 2.9%, according to RealPage.

Despite this challenge, I think the company will emphasize its multifamily real estate focus in the long term and attract more clients with its strong track record. Even though investment managers are everywhere and all competing for money, I think Bridge Investment has shown to be a clear leader in the multifamily space and will likely attract more investment and assets to grow its business and reputation.

Valuation – $10 Fair Value

Starting with TTM revenues of $373 million, I believe revenues will grow at 3% for the next few years. I chose 3% because it is roughly in line with US GDP growth and is below the sector median FWD growth of 5%. Given the dramatic increase in AUMs, I think growing AUMs will continue as more investors are interested in alternative investments and the diversification opportunities it presents. So, assuming a floor of revenues of around $400 million in the future, I think the company can earn distributable earnings of at least $150 million in 2024, which translates to a distributable net margin of 37.5%. For distributable net margin, I calculate it as distributable earnings divided by fee-related revenues. For 2022, the distributable net margin was 59% and for 2023 it was 45%. So, for 2024, my forecast of 37.5% is reasonably below the TTM which gives me comfort in the conservativeness of my assumption.

I think investors shouldn’t pay attention to GAAP earnings, as the accounting rules require unrealized performance allocations to be factored into the income statement. The total investment income severely distorts the true distributable earnings power of the company, as under GAAP rules all investment gains and losses must be accounted for. I think the non-GAAP measures are more accurate as they show earnings that are able to be distributed into dividends.

Investor Presentation Q4 2023

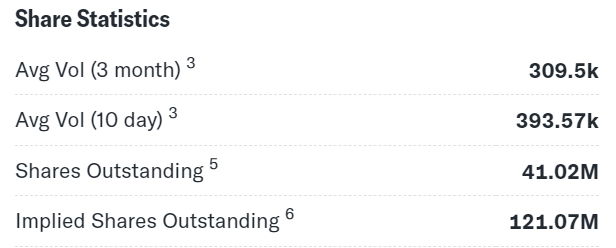

So, the TTM distributable net margin for 2023 was 45%, so my 37.5% net margin forecast looks conservative. Divide $150 million of distributable earnings by implied shares outstanding of 121 million gets me EPS of $1, rounded down. I think implied shares outstanding is more appropriate to account for the conversion of all convertible subsidiary equity into common shares. The reason I used implied shares outstanding is for conservatism sakes and also to account for partnership interests that may dilute shareholders in the future. Also, given the market cap of $830 million, investors can see that Seeking Alpha calculates the market cap based on implied shares outstanding (121 million implied shares x $6.80 share price = ~$830 million market cap).

Yahoo Finance

Apply a sector median of 10x earnings gets me a fair value of $10. I believe the distributable earnings cover the dividend nicely, as $1 of earnings is higher than the 56 cents in dividends for TTM. So, the 8% yield to me looks safe and sustainable. Investors can also see that on a multiple basis the company trades at below average historical valuations. At 1.6x cash flow and a 8% yield, the stock clearly trades cheap.

Risks

The risks for an alternative investment manager like Bridge Investment stem from what happens to AUM. If performance is bad and clients pull out their AUM, reputation, and fees will all decrease, which will likely pressure the stock down.

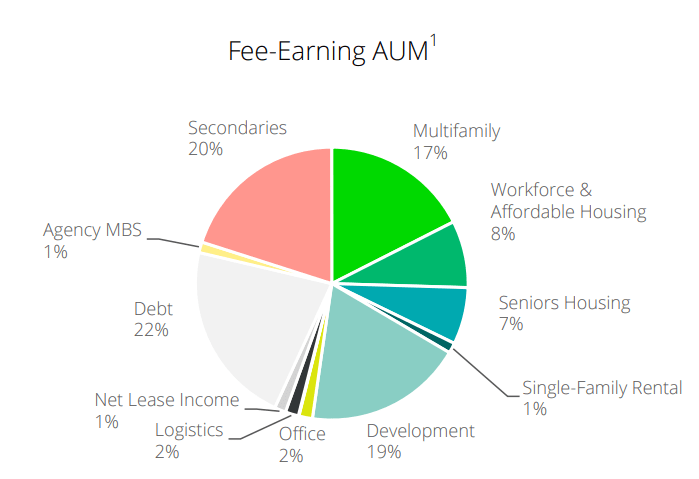

Economic shocks could harm the portfolio of multifamily real estate and dramatically cause realized or unrealized losses in the portfolio. Despite the company’s well-diversified funds, I believe their focus on real estate could be a concentrated risk as multifamily and development make up a large chunk of their fee-earning AUM.

Investor Presentation Q4 2023

Competition is very fierce, as there are more investment managers than ever to choose from. As more people pour money into alternative investments, the number of funds will likely increase, and competition for performance will become more challenging. This could impact Bridge Investments’ performance as more people compete for deals, profits, and AUM.

Regulations may restrict how much money goes into alternative investments, as some regulators may see a risk in having a lot of the nation’s savings into private equity, real estate, and credit. Also, changes in how alternative investments are taxed may make alternative investments less attractive as governments may want to tap into the investment gains as a source of tax revenue.

Buy Bridge Investment

The story here can be quite simple in my eyes. If AUM continues to grow, fees will follow, and the stock should re-rate higher. An alternative investment manager needs to perform well through up and down cycles, and Bridge Investment has proven to do so with their AUMs continually rising even through the pandemic. I think going forward their multifamily and development investments will perform quite well, satisfying both new and old clients. The stock trades cheaply and the dividends seem well covered, so investors who want solid dividends should consider buying Bridge Investment.

{kind=link}