")

Eva-Katalin/E+ via Getty Images

Agricultural commodities are the backbone of the global economy, feeding and powering the world. In 2022, we saw a surge in CBOT corn and soybean prices, reaching multiyear highs and almost breaking the 2012 record peaks. The war in Europe’s breadbasket further fueled supply fears, increasing prices. However, the leading grain and oilseed futures markets corrected in 2023, with nearby corn futures falling by over 30.5%, soybean futures dropping nearly 15%, and the soft red winter wheat futures posting an over 20% loss. This trend continued into 2024, with grain and oilseed prices declining over the first three months.

Soft commodities are also agricultural products. While the grain sector plunged in 2023, soft commodities prices went the other way. The composite grain sector fell over 13% in 2023, while soft commodities, including world free-market sugar, Arabica coffee beans, cocoa beans, cotton, and frozen concentrated orange juice futures, soared over 24%. The bullish price action continued in Q1 2024 as cocoa futures took the bullish baton and experienced a parabolic rally, taking prices to record highs.

Soft commodities continue to rally in 2024

In 2023, soft commodities results were as follows:

- Sugar: a 2.69% gain, closing 2023 at 20.58 cents per pound.

- Coffee: a 12.55% gain, closing 2023 at $1.8830 per pound.

- Cocoa: a 61.38% gain, closing 2023 at $4,196 per ton.

- Cotton: a 2.84% gain, closing 2023 at 81 cents per pound.

- Frozen concentrated orange juice: a 46.41% gain, closing 2023 at $3.022 per pound.

Cotton and Arabica coffee futures rose to the highest prices since 2011 in 2022, and sugar futures reached their highest since 2011 in 2023. FCOJ rose to a record high in 2023, while cocoa futures reached their highest price level since 1977 in 2023.

The bullish price action continued in Q1 2024:

- Sugar: at 22.52 cents on March 29, 2024, sugar futures were 9.4% higher in Q1.

- Coffee: at $1.8885 at the end of Q1 2024, Arabica coffee futures were 0.29% higher than at the end of 2023

- Cocoa: at $9,766 per ton, cocoa led the soft commodities sector and the commodities asset class in Q1 2024 with an explosive 132.75% gain.

- Cotton: at 91.38 per pound, nearby ICE cotton futures were 12.81% higher in Q1 2024.

- Frozen concentrated orange juice: at $3.6325 per pound, nearby ICE frozen concentrated orange juice futures moved 20.2% higher in Q1 2024.

Soft commodities posted across-the-board gains in Q1 2024.

Cocoa takes the leadership baton

In 2022, cotton and Arabica coffee futures led the soft commodities higher, reaching eleven-year highs. In 2023, world sugar futures rose to a twelve-year high, while cocoa reached its highest price since 1977. Frozen concentrated orange juice futures took a leadership role last year as the price reached a record peak.

In Q1 2024, cocoa was the undisputed leader of the soft commodities and entire commodities asset class.

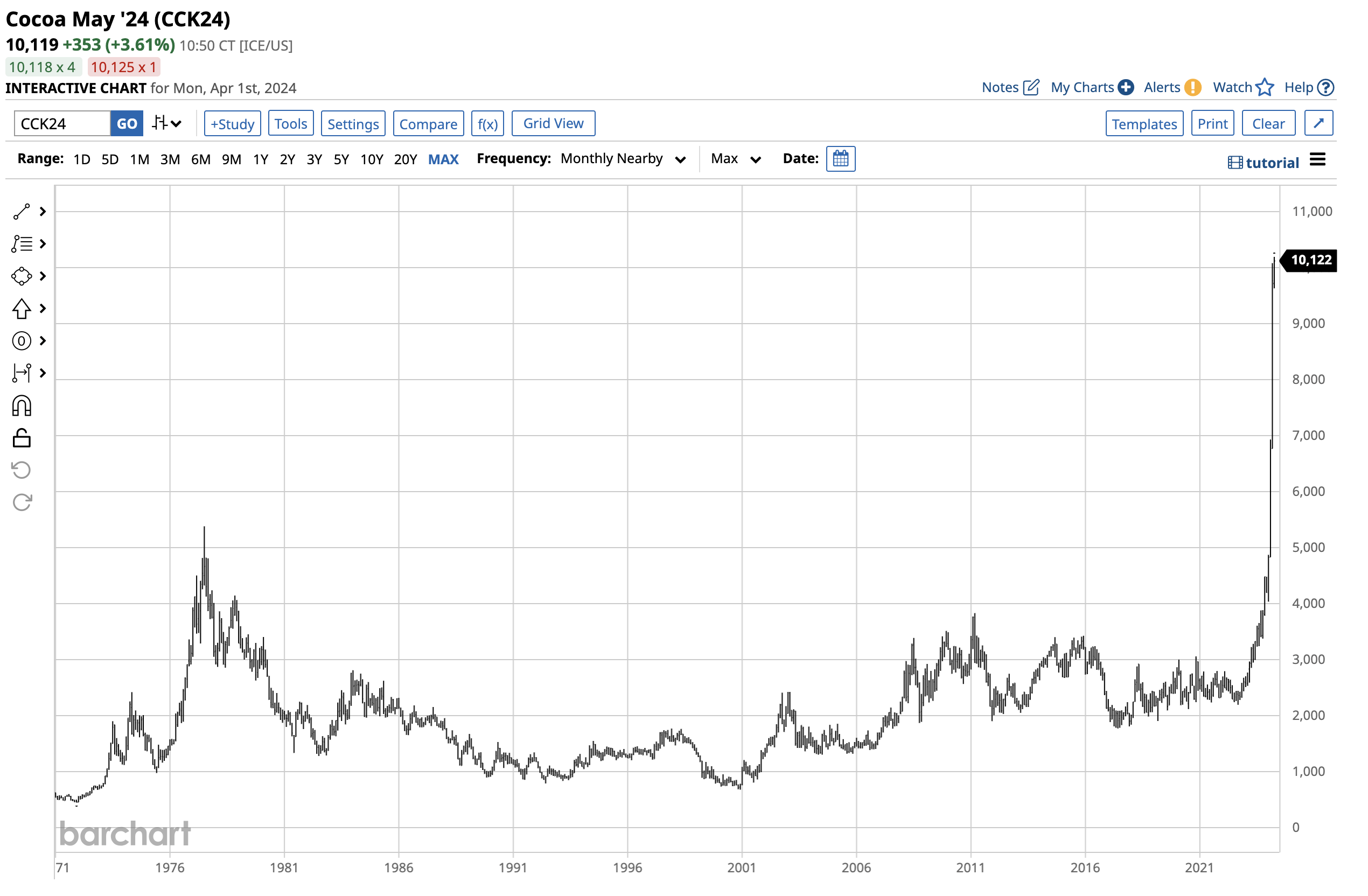

Long-Term ICE U.S. Cocoa Futures Chart (Barchart)

As the monthly chart dating back to 1970 highlights, cocoa futures blew through the 1977 $5,379 per ton record high like a hot knife goes through butter in February 2024, but the parabolic move was just getting started. Cocoa futures reached uncharted territory and rose to a $10,193 per ton high on April 1, after closing March at over the $9,750 level. Cocoa has taken the leadership baton as the price has over doubled since the end of last year.

West African weather and crop issues create the parabolic rally

West African countries are the OPEC of the cocoa market. While approximately 70% of the world’s cocoa beans come from the Ivory Coast, Ghana, Nigeria, and Cameroon, the Ivory Coast and Ghana are the dominant producers, with more than 50% of the world’s annual cocoa output. The equatorial climate supports cocoa production.

Adverse weather conditions in West Africa have pushed the cocoa market into a fundamental deficit, with demand exceeding available supplies. The latest rally and push above the $10,000 per ton level occurred as the Ivory Coast expects the mid-crop to decline this season. A recent Hightower report said, “The West African supply situation remains extremely tight going into the start of the mid-crop harvest next week, and that continues to underpin cocoa prices.”

“When it rains, it pours,” the old saying goes. In cocoa, soggy weather conditions in West Africa have caused an outbreak of fungal black pod disease, infecting pods, flower cushions, young vegetative shoots, stems, and roots of cocoa trees. Simultaneously, the swollen shoot virus, which decreases cacao yield within the first year of infection and typically kills the tree in subsequent years, has damaged crops. Therefore, while prices are sky-high, there is no relief in sight.

Commodity cyclicality – The trend is your friend, but shooting stars can experience significant corrections

Commodities are usually cyclical markets. When prices fall, production costs and output tend to decline, inventories decrease, and demand increases, causing prices to bottom and recover. Conversely, parabolic rallies often lead to increased production and rising inventories, and the elasticity of demand leads to fewer consumer purchases, leading to price tops.

Meanwhile, cocoa price dynamics could keep prices high for the foreseeable future. While Indonesia, Ecuador, and Brazil are cocoa-producing countries, the West African leaders could see output decline over the coming years. However, $10,000 per ton is a steep price that could lead the leading chocolate manufacturers and consumers to seek alternatives, using less chocolate and other ingredients.

The cost of goods sold by two companies weighs on their stocks

The cocoa rally is wreaking havoc with the leading chocolate companies’ cost of goods sold and earnings.

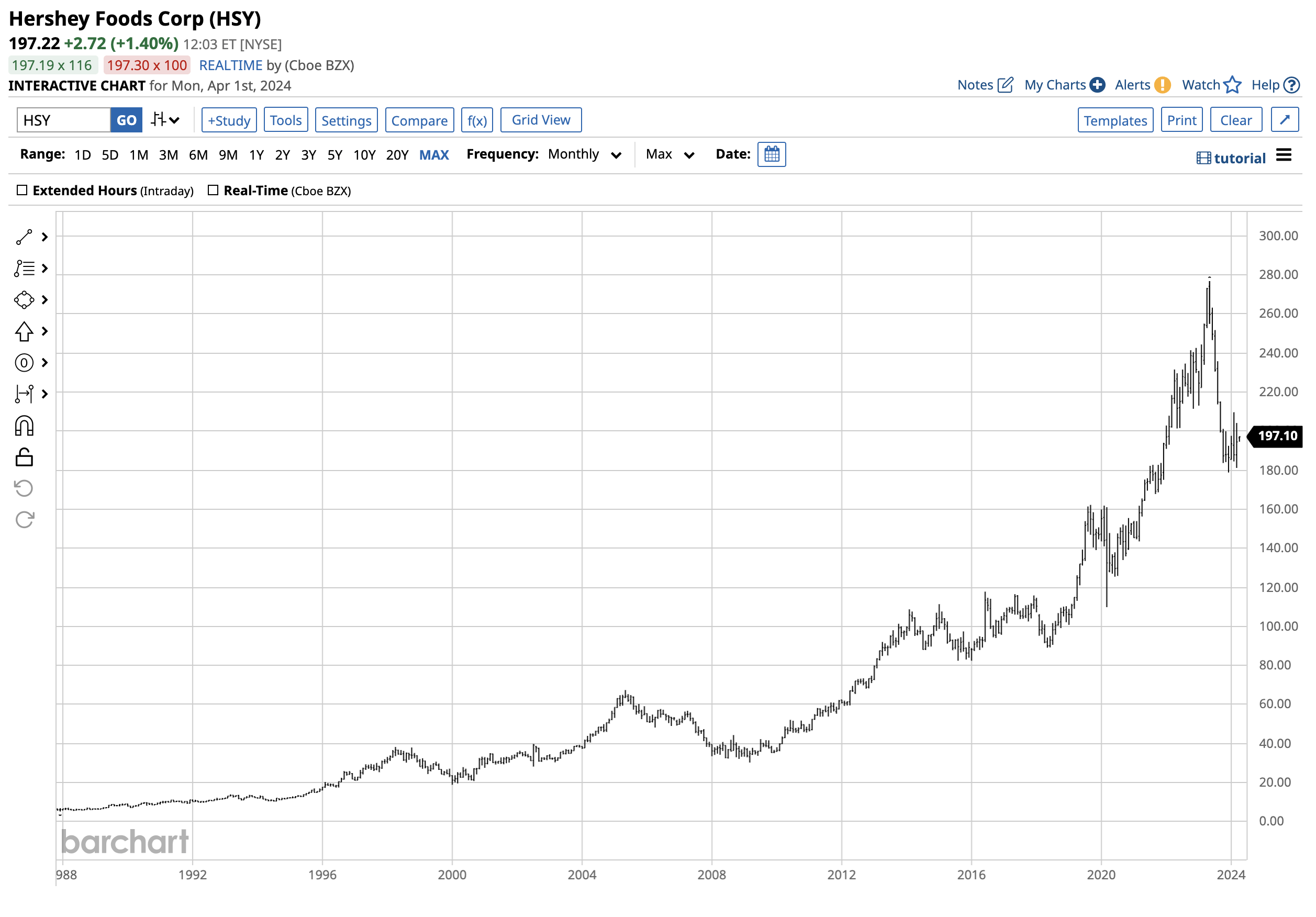

Long-Term Chart of HSY Shares (Barchart)

After reaching a record $276.88 high in May 2023, The Hershey Company (HSY) shares, a company synonymous with chocolate, have dropped over 29.5% to below $195 as of the end of Q1 2024.

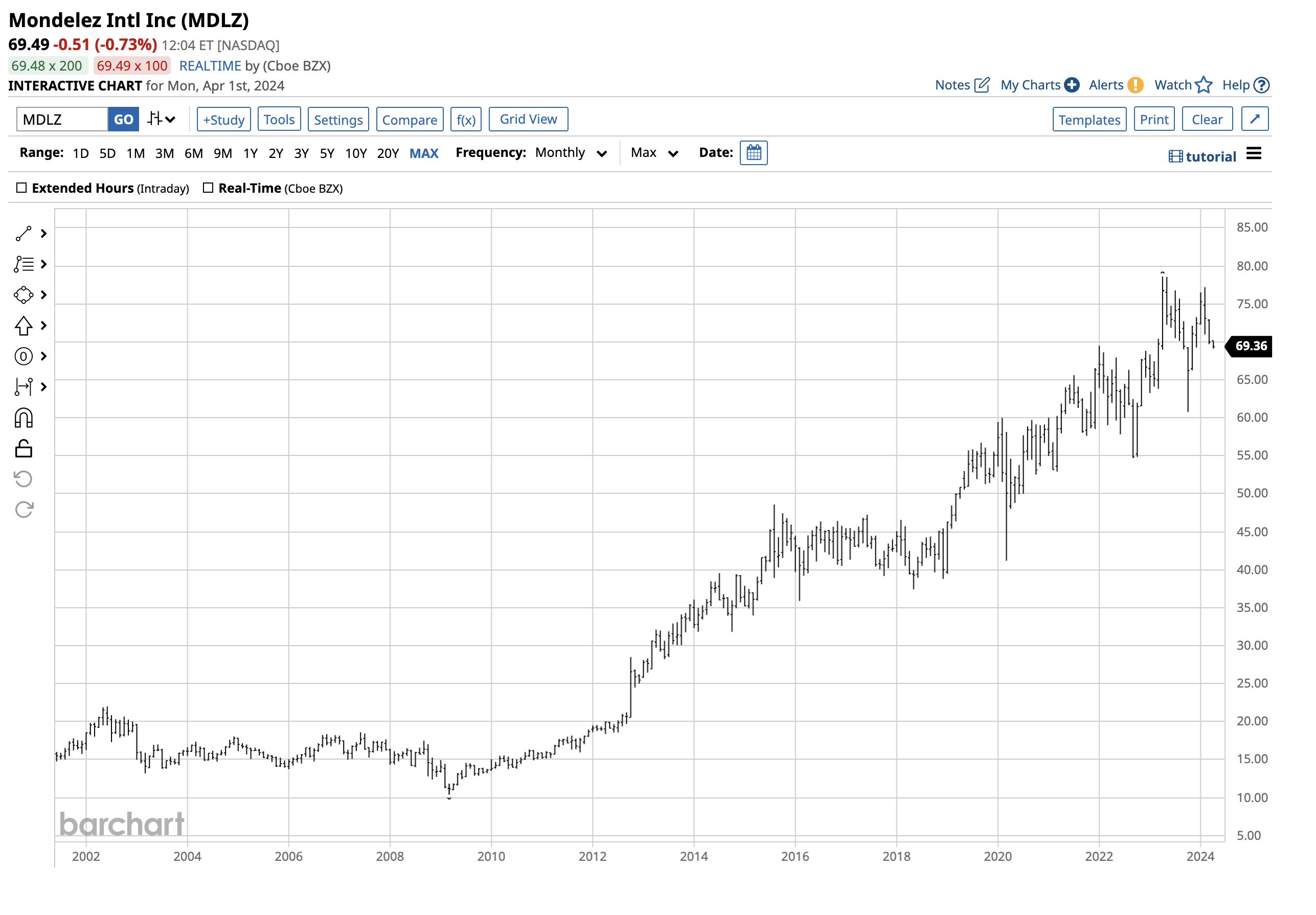

Long-Term Chart of MDLZ Shares (Barchart)

Mondelez International, Inc. (MDLZ) shares have declined over 10% from a record $78.59 high in April 2023 to the $70 level as of March 29, 2024.

The two leading chocolate manufacturers, M&M Mars and Ferrero Group, are privately held, while HSY and MDLZ, the third and fourth leading companies, are publicly traded. Nestle is the fifth manufacturer, and its shares have declined.

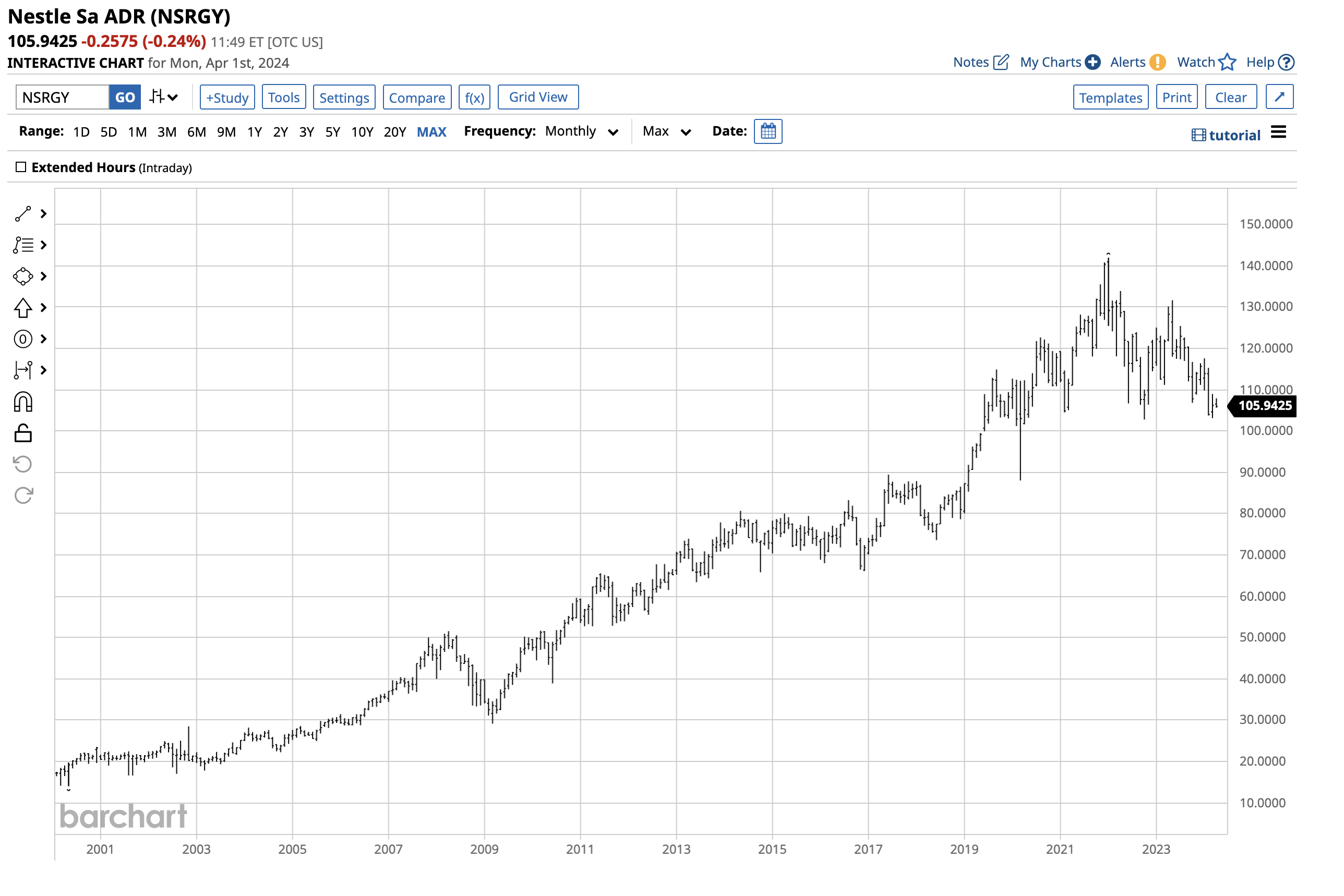

Long-term Chart of NSRGY Shares (Barchart)

The chart shows that NSRGY ADRs have declined over 25% from a record $141.95 high in January 2022 to the $106 level on March 29, 2024.

Chocolate manufacturers suffer from all-time high cocoa bean prices and supply challenges, causing the world’s chocoholics to pay ever-increasing prices for their daily fix of the epicurean treat. While cocoa prices have reached a level that increases the odds of a sudden downdraft, technical support at the 1977 $5,379 per ton high is far below the current price, meaning elevated chocolate prices are likely to stick around for a long time. Meanwhile, production problems in West Africa are an issue for the countries that rely on cocoa revenues.

{kind=link}