JHVEPhoto

Micron Technology, Inc. (NASDAQ:MU) has been on a roll over the past year as the market gobbles up anything related to artificial intelligence (“AI”). Over that time period, the company has returned almost 70% on the fact that its more efficient memory is being used in Nvidia (NVDA) next-generation GPUs. Despite that, Micron stock is atrociously overvalued for a company worth more than $100 billion.

Micron Technology and Artificial Intelligence

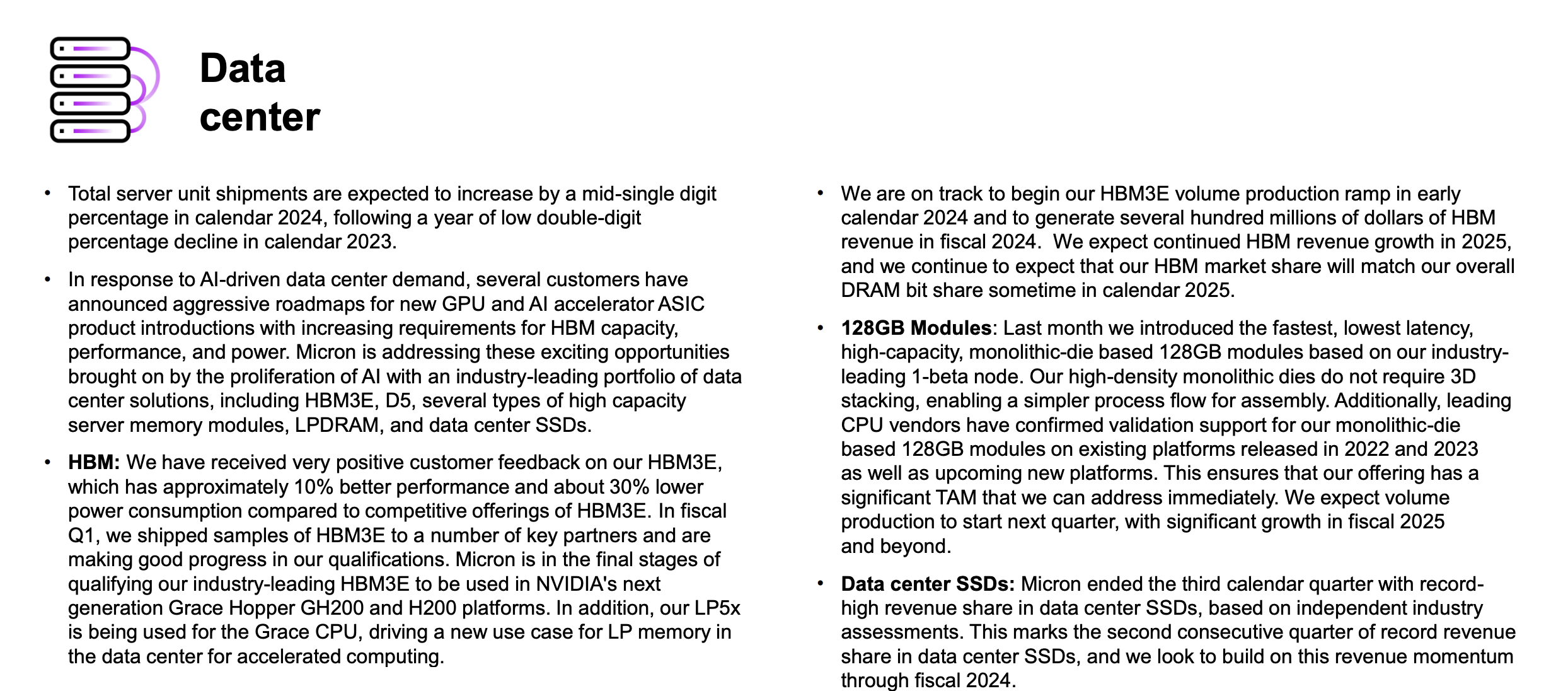

The connection between Micron and artificial intelligence is clear. GPUs are the dominant asset used for artificial intelligence, and the company’s HBM3E memory is a leader in the memory used on GPUs. Nvidia supplier SK Hynix is sold out of HBM3 memory for 2024, meaning that Micron has a clear market here, with higher margins.

However, memory is still a commodity. For 2024, a year with arguably the most significant artificial intelligence GPU purchases, especially as the H200 comes out, Micron only expects “several hundred $ million” in HBM3E revenue. It’s worth noting that Micron has some of the weakest market positioning in HBM3e (10% est.) with its competitors being sold out being a principle driver.

Micron Investor Presentation

The company’s view on the business is visible here, where the company expects mid-single digit increases. The company has built a strong product with HBM3e, but it doesn’t expect market share to catch-up until 2025. Even with substantial YoY growth, the company’s path to even $1 billion in annual revenue is tough to see right now.

That makes it a single-digit % of the company’s revenue. Given immediate capital costs and the strong performance of competitors, we don’t see this as a game changer. Micron is simply catching up, it’s not outperforming. Given that in the DRAM markets margins with its two competitors have been tight, we don’t see 2024 as a year of outperformance.

Micron End Market Performance

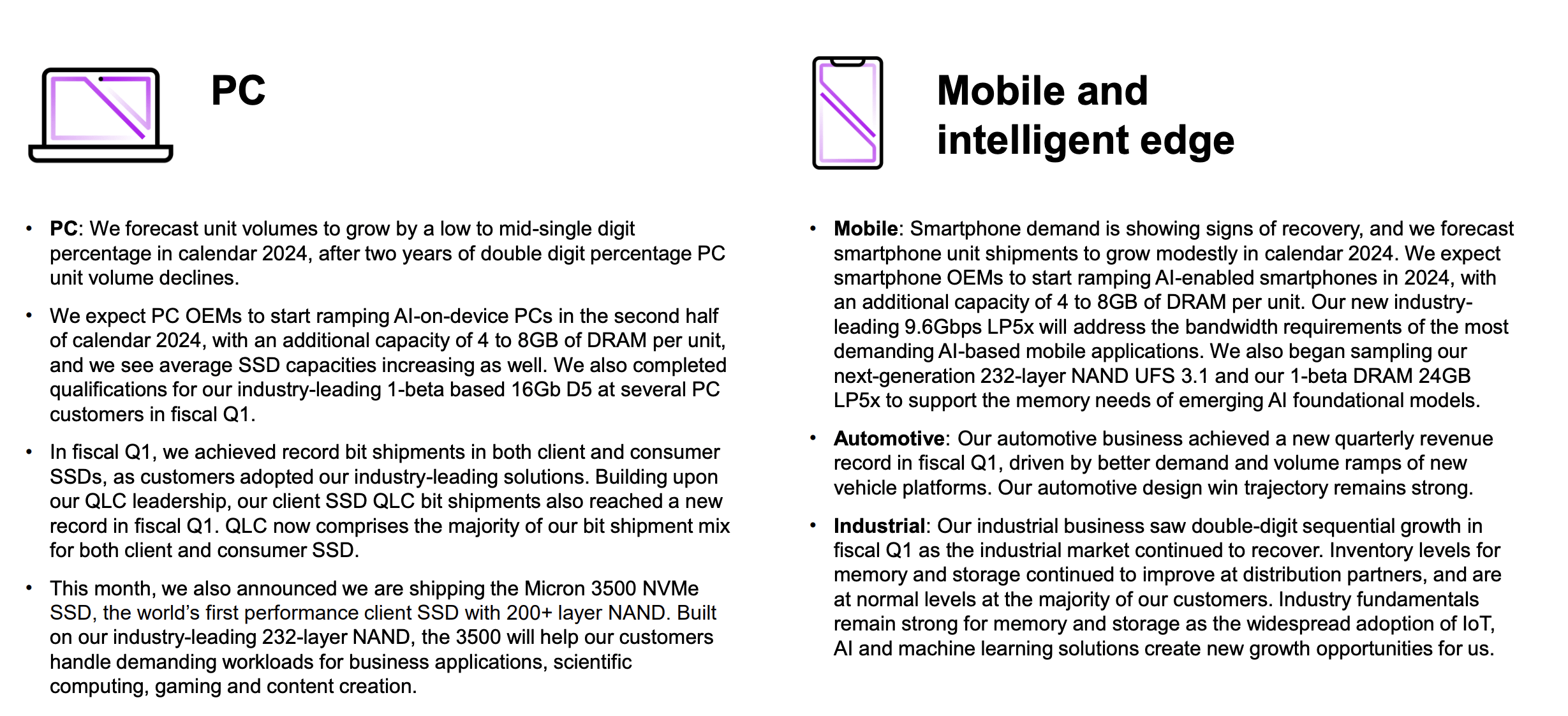

Micron’s core end markets continue to struggle, even with some opportunism.

Micron Investor Presentation

The company sees a bit capacity increasing for both DRAM and SSD capacities, but volumes are still expected to grow just a few %. The company expects the potential for several G more DRAM per PC, which isn’t unrealistic, but is wholly non-significant for the industry’s long-term demand, especially as the average increase of DRAM amount in laptop has slowed down.

For perspective, the 2010 15″ MBP came with 8 GB ram by default, a configuration that is still default for MBP today. That shows how slowly demand has grown, while production costs have come down and competition has increased. The company’s mobile business is more likely to get a boost in our view as AI capabilities move to devices.

This could help the company and demand in the short term, especially as wafers are redirected to HBM3. There is some potential here, but nothing that we see that will drive the company to drive substantial returns.

Micron Outlook

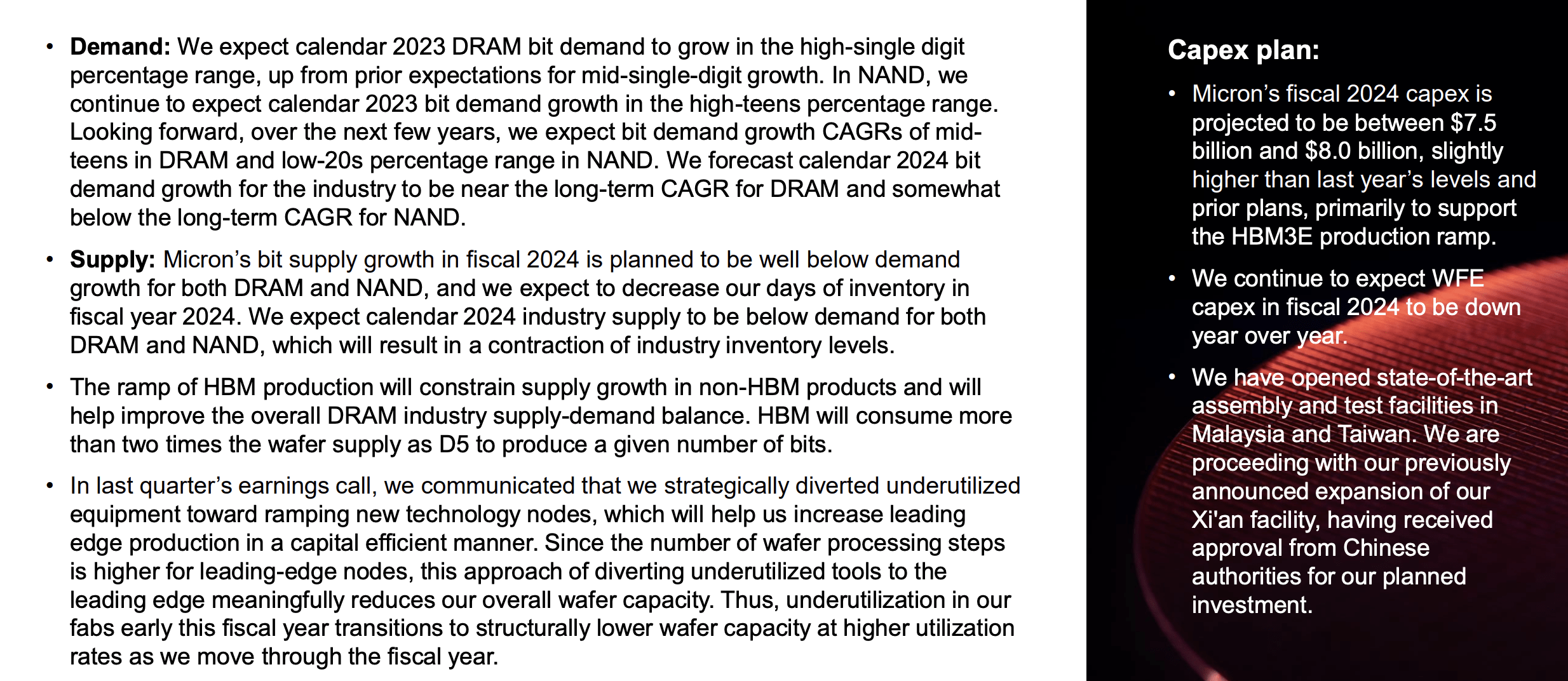

The company’s outlook is for a recovery in prices, but impacted by massive capital spending.

Micron Investor Presentation

The company is upgrading forecasts for DRAM demand a bit growth, but still expects it to be weaker than usual. It does expect demand to recover over the next several years, but the market is very volatile. The company expects inventory to decline as supply declines, but it is also using significant wafers on HBM memory.

The company’s capital expenditures remain lofty, and we see $7+ billion as being a long-term capital level. Unfortunately, the company is the smallest of its peers, and Samsung (OTCPK:SSNLF) continues to push to increase its market share.

Micron Financial Performance

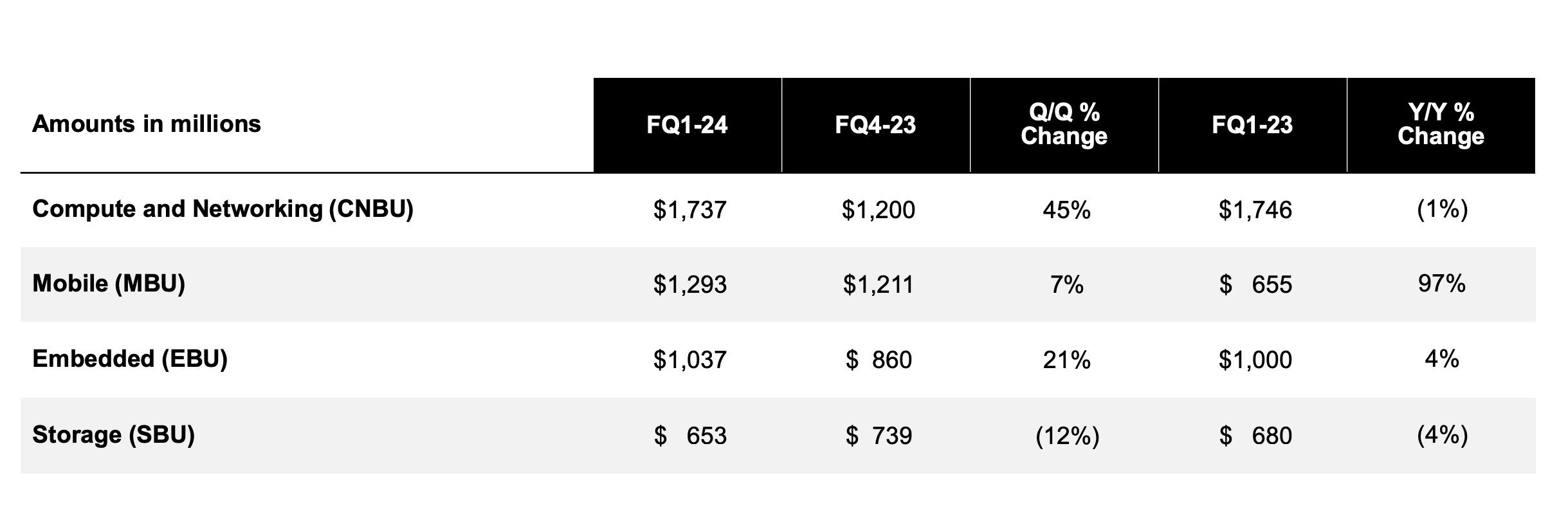

The company’s financial performance has improved YoY, but also shows the company’s tough market.

Micron Investor Presentation

The company has seen strong performance from the data center segment. However, its storage business has suffered and growth in mobile has been low. That means overall revenue growth hasn’t been particular strong. Especially worth indicating is that YoY revenue growth is much weaker than its share price would indicate.

Micron Investor Presentation

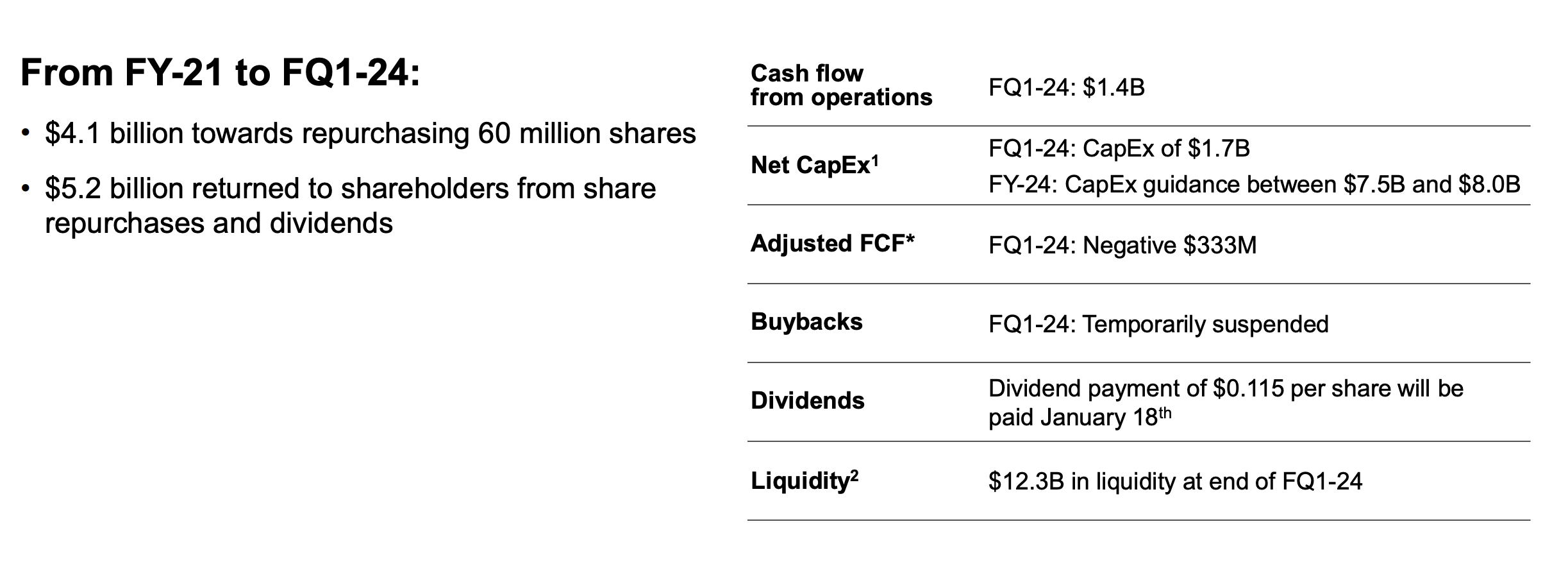

However, the real concern is the expenses of managing the company’s business. The company’s $4.7 billion in revenue for the quarter was a mere 1% in gross margin. The company’s net income was -$1 billion and the company’s cash flow was negative. That’s for a year when the company has already released HBM3E.

Over the last 3 years, the company has returned $5.2 billion to shareholders, a mere 5% cumulative yield in what was a strong time for stocks. The company’s capex guidance remains ~$1.8-9 billion / quarter, meaning even with the company’s guidance for ~10% QoQ growth in FQ2, we still expect FCF to be negative or close.

Thesis Risk

The largest risk to our thesis is the continued concentration of the memory market. From many companies we’re now down to 3: Sk Hynix, Samsung, and Micron. Increased competition for AI GPUs could knock that down to 2. That would make the market less of a commodity market and more of a normal market with profit potential.

Conclusion

There’s no denying that Micron’s products are great. The company is a leader in cutting edge DRAM / NAND and has recently announced some exciting results from its HBM3E DRAM. However, that doesn’t change the thesis around a $100 billion company that needs to actively drive returns for shareholders, to the tunes of billions of dollars / year.

Even with a reasonable market, Micron Technology, Inc. has only managed to drive 5% cumulative returns over the past 3 years. The company remains stymied by substantial competition, especially from Samsung, which is growing its market share, and massive capital obligations. As a result, we expect Micron Technology’s share price to decline substantially over the coming years.

Tunnel")

{kind=link}