")

spooh

A guest post by D Coyne

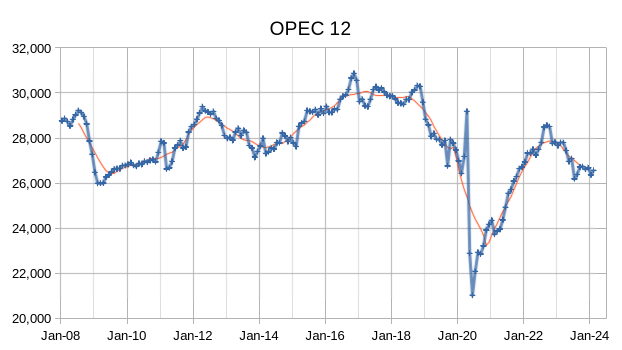

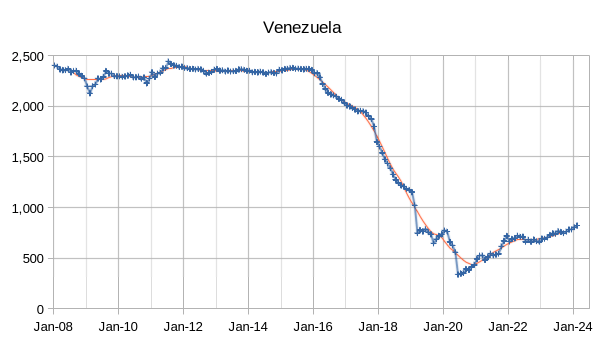

The OPEC Monthly Oil Market Report (MOMR) for March 2024 was published recently. The last month reported in most of the OPEC charts that follow is February 2024 and output reported for OPEC nations is crude oil output in thousands of barrels per day (kb/d). In the OPEC charts that follow the blue line with markers is monthly output and the thin red line is the centered twelve-month average (CTMA) output.

There was no update on World Liquids in the March MOMR, which is different from every other MOMR I have read.

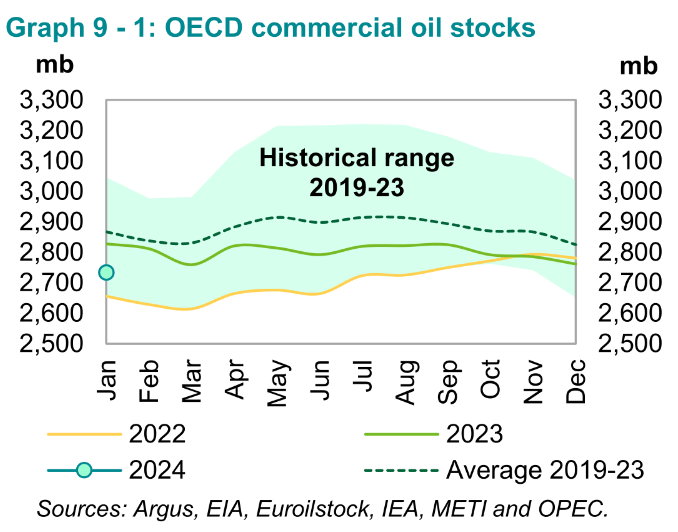

Preliminary January 2024 data shows total OECD commercial oil stocks down by 26.8 Mb, m-o-m. At 2,735 Mb, they were 94 Mb lower than the same time one year ago, 132 Mb lower than the latest five-year average and 192 Mb below the 2015-2019 average. In short, OECD commercial stocks are low.

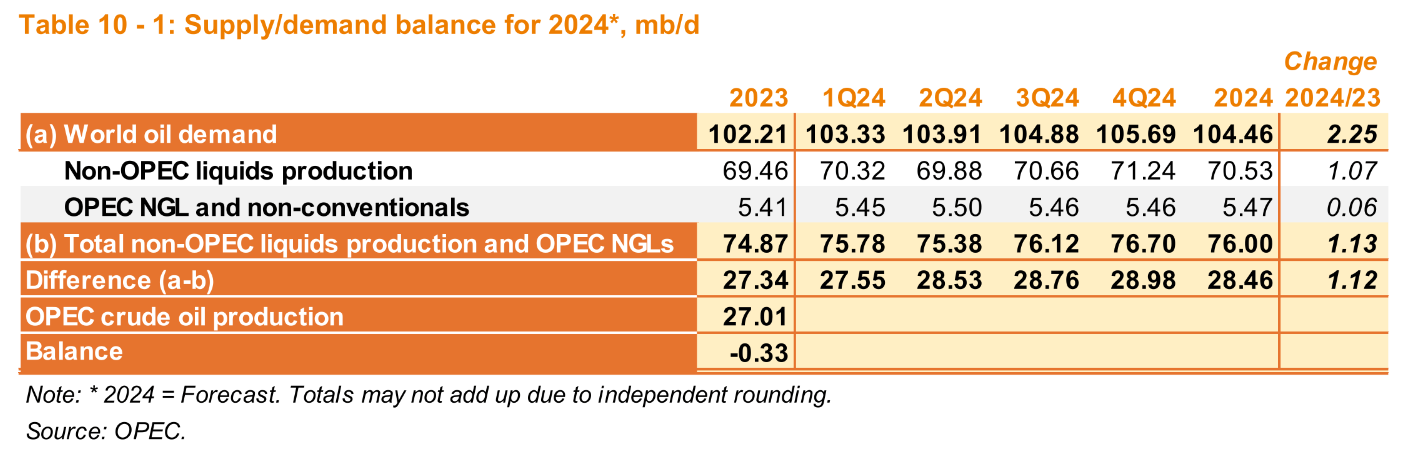

OPEC expects robust growth in World Demand for Liquid fuel in 2024 (2.25 Mb/d) and 2025 (1.85 Mb/d). The growth in liquids demand expected by the EIA is about 1.4 Mb/d in 2024 and is similar to the IEA’s estimate in their March Oil Market report of 1.3 Mb/d. In addition, the EIA has a 1.24 Mb/d lower estimate for World liquids demand in 2023 than OPEC.

The chart above shows the different estimates of the “call” on OPEC for crude in the March STEO and MOMR reports. These estimates may represent wishful thinking on the part of both agencies, and reality may fall somewhere between these two estimates. My guess is that demand for OPEC crude may be closer to the EIA’s STEO, but I am often wrong in my predictions of the future.

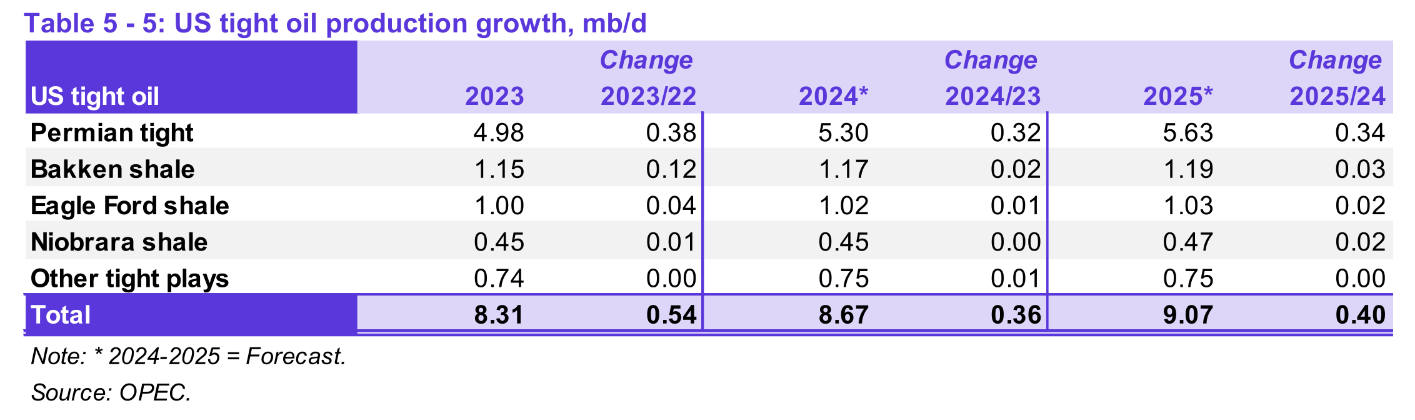

The OPEC estimate for future US tight oil growth in output is unchanged from last month, about 4% growth in 2024 and 5% growth in 2025.

{kind=link}