Economic uncertainty and weak operating rates are expected to limit prospects for a petrochemicals recovery in 2024. Demand is showing signs of stabilization, but oversupply will continue to weigh on margins.

Chemical makers will face challenging markets again in 2024 as weak economic growth and oversupply weigh on prospects.

Demand for most petrochemicals was weaker than expected in 2023 due to severe inventory destocking and weak demand. Producers are seeing hopeful signs that the demand is starting to stabilize but are hesitant to predict the pace of any recovery. Higher inflation, interest rates, and geopolitical tensions also present challenges and risks to growth in the year ahead.

The outlook for the broader economy and energy markets is also mixed. Economic prospects by region continue to vary with the US showing surprising strength through late 2023, China struggling to regain lost momentum and the Eurozone headed for a recession. Annual global real GDP growth is forecast to slow to 2.3% in 2024, down from 2.6% in 2023, with the risk of a more prolonged period of weakness increasing, according to S&P Global.

Dated Brent prices are forecast to decline from $93/b in October to $81/b in March 2024, according to S&P Global Commodity Insights, but with potential for volatility owing to geopolitical turmoil and economic uncertainties. Prices are expected to rise after the first quarter of 2024. S&P Global’s annual average forecast for Dated Brent is $85/b in 2024 and $76/b in 2025.

Download the latest Commodity Insights Magazine. Features include:

*Financing the energy transition

*Oversupply weighs on global petrochemicals

*Global gas market’s trauma

US-headquartered Dow recently said it expects challenging market conditions to persist through the fourth quarter but noted some indications that things could improve in next year.

“Third quarter was the first [in 2023] with year-over-year volume growth in the core business,” said Jim Fitterling, Dow chairman and CEO. “This slowdown in the industrial economy started in the middle of last year from our perspective, which puts us 12-15 months into a downturn.”

“And usually in a market correction like we’ve been seeing, we start to see things turn back the other direction in the 12- to 18-month time period. We’re watching carefully.”

Typically, one of Dow’s strongest recovery indicators is monoethylene glycol (MEG) pricing, Fitterling added.

“We’re starting to see spot MEG pricing move up,” he said. “Polyester production rates in China are above 70%. They haven’t been that high for quite some time. MEG has always been the highest correlation leading indicator. I don’t think we’ve seen enough yet to say we’re turning the corner, but if it looks like interest rate increases are going to slow or stop, and things stabilize here, then I think there’s room for things to move up in 2024.”

Surplus builds

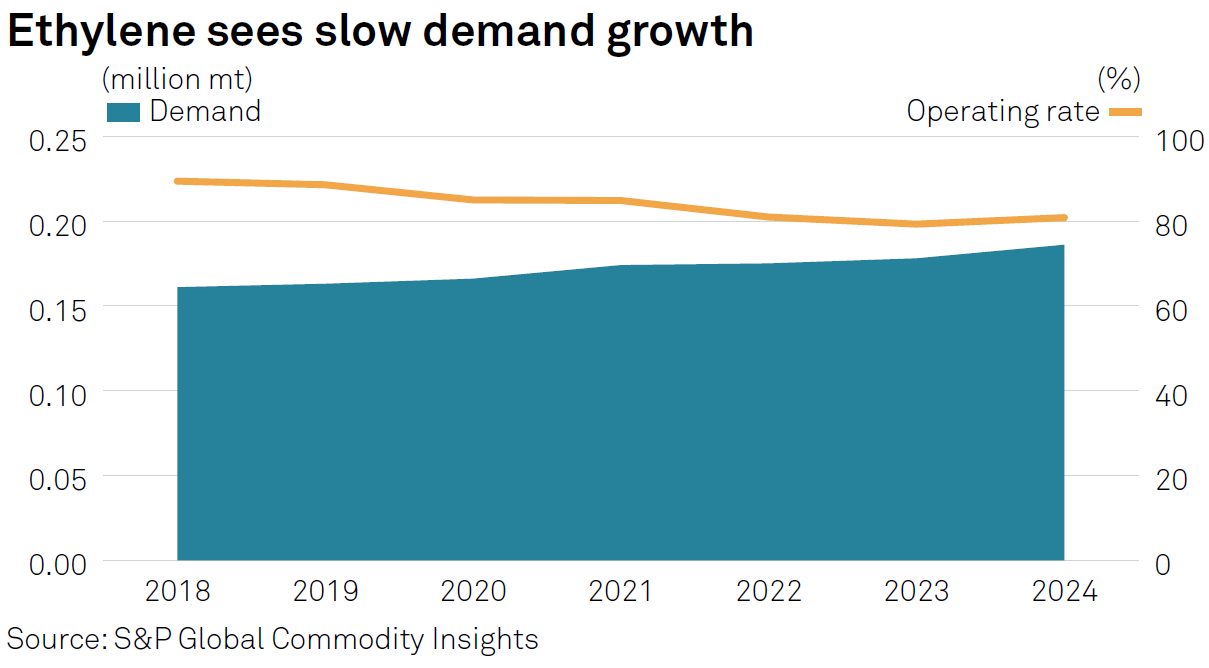

The global ethylene market serves as a proxy for petrochemicals, signaling a supply-driven surplus through 2026, said Robert Stier, senior lead for global petrochemical analytics at S&P Global Commodity Insights.

Plastics demand has been lower than expected on inventory restocking and weak durable goods demand. A major polymer destocking has distorted underlying demand comparisons. Year-on-year global demand growth in 2023 is forecast to be close to zero for polyethylene and polyvinyl chloride, Stier said. Global polypropylene demand is expected to rebound to 3%-4% in 2023 after a weak 2022 where annual demand growth was essentially zero.

“We are forecasting 2024 polymer demand to increase back to GDP levels or slightly higher after two weak years,” Stier said. “It’s all about Asian growth in 2024, however, as the rest of the world is slowing down.”

The demand forecast is somewhat optimistic assuming “stable GDP and some end-user inventory restocking at zero margin and low prices,” Stier added. “However, there is no realistic demand scenario that makes 2024 plastics margins sustainably bullish.”

Global ethylene margins based on naphtha feedstock will remain challenged through 2024 regardless of demand scenarios due to all the new capacity.

“And 2025 is also going to be a low-margin environment globally unless there is meaningful industry consolidation and rationalization,” Stier said.

S&P Global’s base case assumption around ethylene capacity is that there will be about 10 million-15 million mt of ethylene capacity rationalization over the next two or three years, to enable sustainable margin recovery starting around 2026.

Overall, global petrochemicals prices appear to have reached a peak in October and are forecast to grind lower into early-2024 following energy and feedstock prices lower. Naphtha margins remain most challenged with naphtha-based feedstock ethylene margins below seasonal averages in all three regions since mid-2023 and European and Northeast Asian spot ethylene margins close to zero in November. Europe remains the weakest region with low ethylene margins and disappointing derivative demand.

US petrochemical producers should remain relatively advantaged, thanks to benefit from significant natural gas and ethane feedstock cost advantages, and this edge should continue into 2024.

The downturn has not diminished urgency around the need for energy transition and industry continues to invest in decarbonization to cut CO2 emissions and in advanced recycling projects to address plastic waste.

Currently, 76% of the Billion-Dollar Club – Chemical Week’s annual ranking of the world’s top 100 chemical makers with publicly disclosed revenues – has committed to carbon neutral or net-zero goals by 2050, and 88% have set interim reductions for 2030, according to a survey of climate-related disclosures.

This article first appeared in the December edition of

Commodity Insights Magazine

.

{kind=link}