Two buyout firms behind a soured 2021 software deal are trading allegations of incompetence and fraud, suing one another in duelling cases that have breached unwritten rules of the private equity industry.

HIG Capital has filed a complaint against fellow middle-market specialist Audax Group, which sold telecoms software company Mobileum to HIG for $915mn in early 2022.

The investment has proven disastrous. Mobileum in December failed to make an interest payment on a portion of $540mn in floating-rate term loans. S&P Global Ratings and Moody’s have declared its debt to be in default, while the company and its creditors have hired lawyers for a possible loan restructuring.

In mid-December Mobileum terminated longtime chief executive Bobby Srinivasan, brought in by Audax in 2016 and later retained by HIG, over what it described as “serious personal and professional misconduct”.

Busted buyouts are common. But rather than move on, HIG has sought redress in a Delaware state court, accusing Audax of directing a “brazen, massive, systemic” accounting fraud at Mobileum to juice the selling price.

Audax has countersued and pinned blame on the buyer. “HIG promptly ran what was a high-performing business into the ground,” the firm alleged in court papers. Audax went as far as to describe a HIG-led inquiry into Mobileum’s accounting practices as a “Stalinist show trial”.

One private equity firm going directly after another is regarded as a breakdown of decorum in a province of Wall Street where a measure of professional comity among peers still persists.

“It is extremely rare for private equity firms to sue each other directly like this, both because of legal and contractual hurdles that make it difficult, and because both sides are likely to take a reputational hit,” said Elisabeth de Fontenay, a former corporate lawyer and current law professor at Duke University.

The brawl also comes at a difficult moment for the private equity industry, as deals struck in an era of low interest rates struggle to meet heightened debt obligations, and their valuations fall.

Audax and HIG have been among the most successful on Wall Street in buying smaller, privately held companies, the area where most corporate dealmaking occurs, and then selling them to other private equity firms in so-called secondary buyouts. “Those two firms are two peas in a pod,” said one private equity executive who had experience negotiating against both.

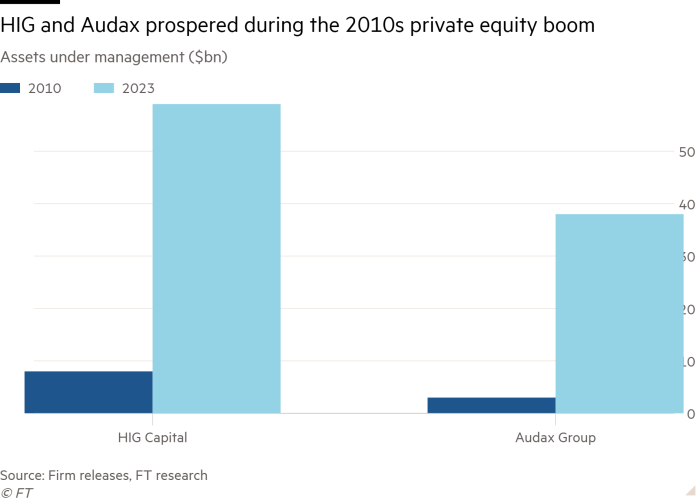

Miami-based HIG first made a name for itself with deals that hived off unloved business lines that were tucked inside larger conglomerates. The firm’s assets under management have jumped from less than $10bn in 2010 to nearly $60bn, as it enjoyed strong returns and fundraising at a time of rock-bottom interest rates and steady economic growth.

Audax, which manages $36bn from its base in Boston, had acquired Mobileum in 2016 and boasted that it had used acquisitions to grow the company’s annual operating cash flow from $16mn to more than $80mn by the time HIG presented its buyout deal.

HIG said it calculated its $915mn purchase price by calculating a valuation of 13 times Mobileum’s 2021 earnings before interest, taxes, depreciation and amortisation.

But after closing the transaction, HIG said it quickly came to believe that “Mobileum was caused to prematurely recognise revenues, and thus earnings, on long-term projects using falsified time sheets or time entries”.

HIG also said in its complaint that the company had inflated software “bookings”, customer contracts that eventually lead to revenue in future periods.

“Mobileum created and recorded sham bookings and new orders,” wrote HIG, even accusing Audax of locating a nascent company that allegedly sent fake orders to Mobileum in order to juice its growth rate.

The alleged profit manipulation caused HIG to overpay by at least $250mn, the firm said, while conceding that a remainder of Mobileum retained some financial value.

The two investment firms declined to comment for this article.

As in most private company acquisitions, Mobileum’s deal contract with HIG included representations and warranties that vouched for the accuracy of its financial statements. Breaches of those provisions, however, are typically capped at a small dollar amount and any liability is typically directed at the company itself.

De Fontenay said that by pursuing a fraud claim, HIG could bypass the typical limitations on a representation-and-warranty claim. Moreover, by suing Audax, HIG was pursuing a target with far deeper pockets than that of the deeply distressed Mobileum. HIG’s lawsuit, filed under the names of multiple affiliates, said they “had no basis and were not in a position to uncover this fraud in the [due] diligence”.

Audax typically takes over companies in sectors such as healthcare and software then buys smaller competitors in strategies known as “roll-ups”.

In these, a buyout firm will buy several businesses and combine them before selling the broader company to another private equity firm. Such deals account for about 75 per cent of private equity dealmaking activity, according to PitchBook. Audax rolled six acquisitions into Mobileum, more than trebling its revenues from $69mn in 2016 to $242mn in 2021.

“They do a lot of those tuck-in build-ups. It’s their stock and trade,” said one private equity executive who characterised Audax deals as “amongst the most complicated” in the industry because of the number of companies being merged.

Bankers and private equity executives ventured that Mobileum represented “mission creep” for HIG, a firm that is best known for buying inexpensive or distressed assets and then using leverage and operational improvements to juice returns.

But like many peers in the private equity industry, HIG had in recent years expanded its investment focus, using success in corporate buyouts to push into strategies spanning real estate credit, infrastructure, software and biotechnology-oriented investments.

In its defence, Audax has pointed out that its own capital is at risk from any failure at Mobileum. Audax still owns a quarter of the company’s equity through $140mn that was rolled into the HIG buyout, a fact it says proves it had little incentive to cheat HIG.

HIG purchased Mobileum with capital from a maiden technology fund that it had launched a few months before the deal. The firm has now backtracked from that approach, saying future tech deals will come from general buyout vehicles rather than dedicated tech funds.