adds ₩13b to market cap in")

While it may not be enough for some shareholders, we think it is good to see the Daesung Private Equity, Inc. (KOSDAQ:027830) share price up 18% in a single quarter. But that doesn’t change the fact that the returns over the last three years have been disappointing. Regrettably, the share price slid 57% in that period. So the improvement may be a real relief to some. Perhaps the company has turned over a new leaf.

While the stock has risen 13% in the past week but long term shareholders are still in the red, let’s see what the fundamentals can tell us.

See our latest analysis for Daesung Private Equity

There is no denying that markets are sometimes efficient, but prices do not always reflect underlying business performance. By comparing earnings per share (EPS) and share price changes over time, we can get a feel for how investor attitudes to a company have morphed over time.

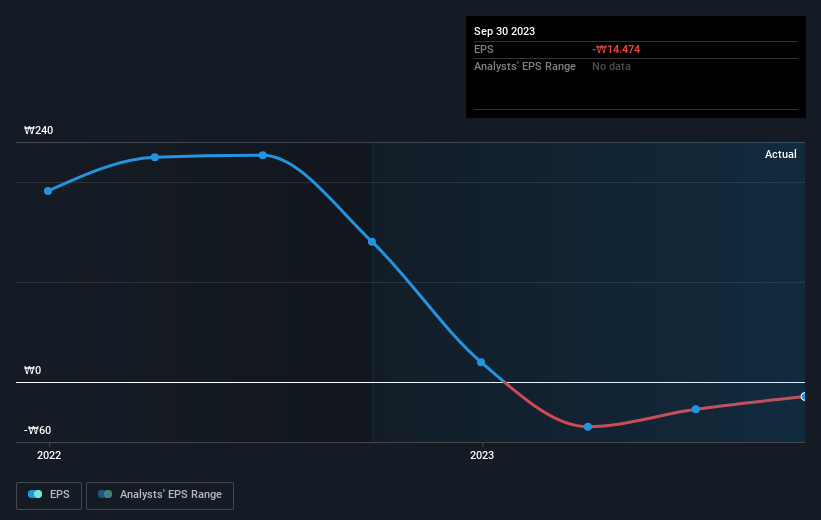

Over the three years that the share price declined, Daesung Private Equity’s earnings per share (EPS) dropped significantly, falling to a loss. Extraordinary items contributed to this situation. Since the company has fallen to a loss making position, it’s hard to compare the change in EPS with the share price change. But it’s safe to say we’d generally expect the share price to be lower as a result!

The graphic below depicts how EPS has changed over time (unveil the exact values by clicking on the image).

Dive deeper into Daesung Private Equity’s key metrics by checking this interactive graph of Daesung Private Equity’s earnings, revenue and cash flow.

What About The Total Shareholder Return (TSR)?

We’d be remiss not to mention the difference between Daesung Private Equity’s total shareholder return (TSR) and its share price return. The TSR attempts to capture the value of dividends (as if they were reinvested) as well as any spin-offs or discounted capital raisings offered to shareholders. Daesung Private Equity hasn’t been paying dividends, but its TSR of -54% exceeds its share price return of -57%, implying it has either spun-off a business, or raised capital at a discount; thereby providing additional value to shareholders.

A Different Perspective

While the broader market gained around 14% in the last year, Daesung Private Equity shareholders lost 0.5%. However, keep in mind that even the best stocks will sometimes underperform the market over a twelve month period. Longer term investors wouldn’t be so upset, since they would have made 2%, each year, over five years. It could be that the recent sell-off is an opportunity, so it may be worth checking the fundamental data for signs of a long term growth trend. It’s always interesting to track share price performance over the longer term. But to understand Daesung Private Equity better, we need to consider many other factors. Take risks, for example – Daesung Private Equity has 3 warning signs we think you should be aware of.

We will like Daesung Private Equity better if we see some big insider buys. While we wait, check out this free list of growing companies with considerable, recent, insider buying.

Please note, the market returns quoted in this article reflect the market weighted average returns of stocks that currently trade on South Korean exchanges.

Valuation is complex, but we’re helping make it simple.

Find out whether Daesung Private Equity is potentially over or undervalued by checking out our comprehensive analysis, which includes fair value estimates, risks and warnings, dividends, insider transactions and financial health.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

{kind=link}