Part 1: Navigating the Opportunity

The semiconductor industry is on the cusp of a new growth cycle.

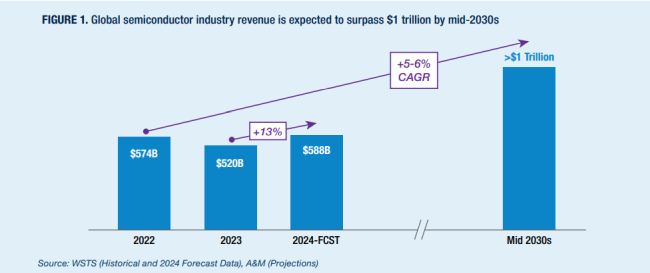

A&M sees a path to a staggering $1 trillion global revenue in

the sector by the mid-2030s, up from the record revenue of $574

billion achieved in 2022.1

The remarkable expansion and opportunity are set against a

backdrop of increasing complexity within both the industry’s

own evolving dynamics and the broader geopolitical landscape. Such

complexity is expected to usher in an era of change, challenging

companies to adapt the ways they operate in all aspects of the

business while adapting to the shifting customer and value chain

landscapes.

Join our team as we embark on a series of papers first seeking

to understand the sources of the opportunity as well as the

increasing complexity and key implications, then exploring specific

strategic areas. The series will explore, among some of the topics,

how companies can:

- Adapt their talent recruitment and development

processes; - Improve their selection and execution of research

and development (R&D) projects; - Better hone their go-to-market efforts;

and - Make more strategic capital expenditure (CapEx)

decisions

A Trillion-Dollar Global Industry

The global semiconductor industry reached a peak revenue of $574

billion in 2022 while 2023 saw a 9.4 percent decline — not

unexpected in a typically cyclical industry. We are now on a new

growth path fueled by advancements in artificial intelligence (AI)

and other innovative applications like automotive Advanced Driver

Assistance Systems, or ADAS, and many more. The speed at which

these technologies are expanding is considered rapid even by

seasoned industry experts.

The World Semiconductor Trade Statistics (WSTS), which tracks

data and trends in the industry, expects a rebound from 2023 and

forecasts 2024 revenue growing at 13% and topping the previous

record at $588 billion, driven by a strong recovery of the memory

segment and robust performances by logic and microelectronic

semiconductors. A&M’s expectation is that the growth will

continue beyond 2024 and, despite the inevitable corrections in

between, we expect the industry to surpass the $1 trillion mark by

the mid-2030s (Figure 1).

Semiconductors are and will continue to be at the core of the

key technologies that ensure our productivity, national security

and way of life, and new and exciting applications will almost

certainly drive specific market sub-segments.

The first major driver appears likely to come from technology

players and their customers who are racing to develop artificial

intelligence platforms and use cases. The first step is to

establish the hardware platform — the actual foundation on

which complex models can be trained and run. We see this effort not

only in the recently released quarter earnings from one of the

early AI semiconductor leaders, NVIDIA, showing a staggering 265

percent revenue growth from the prior year,2 but also in

the reports that Sam Altman, CEO of OpenAI, is seeking partners to

enter the semiconductor design and manufacturing business

directly.3 More evidence indicating a focus on the

foundational hardware is Intel’s recent announcement that it

will develop custom chips for Microsoft4 and in the $52

billion CHIPS and Science Act that the U.S. Government has

allocated to the industry.

The second step, once the foundational hardware is available, is

for companies to go beyond the hype and develop robust use cases

for AI. Despite the dream of a true artificial general intelligence

(AGI) promising to solve any kind of problem, companies still need

to hone the models and perfect the platforms for their own

environments. This will spur even more requirements for the

hardware and continue the cycle of innovation.

The Automotive segment is another very promising end market. We

expect the segment to reach $300 billion by the mid-2040s, up from

approximately $40 billion to $50 billion at the beginning of this

decade. Despite some short-term woes, the interest in electric

vehicles continues to grow5 and the momentum of Chinese

manufacturers, especially in Asia and Europe, will help drive

prices down and demand up.6

Finally, it is important to remember that while leading-edge

technologies often trigger exciting news, segments like industrial

and even some automotive applications rely on more proven

technologies still manufactured on 200 mm wafers, and the

investment opportunity lies in strengthening or expanding the

ecosystem, as we argued in our prior papers.7

Dissecting the Complexity: Understanding the Variables

Semiconductor design and manufacturing have always pushed the

limit of what is possible. When Intel co-founder Gordon Moore

predicted in 1965 that transistors on an integrated circuit (IC)

would double every year for the next 10 years (later revised to two

years), it was amazing to have up to 100 transistors per IC. Today,

companies are working on “50 billion transistors on a chip the

size of a fingernail” and features as small as 1 and 2

nanometers,8 essentially the diameter of a human DNA

strand! The innovation and resources that make it possible to

design and manufacture at such a small scale cannot be

underestimated. To put this in perspective, today there is only one

company in the world, ASML, that can manufacture the key EUV

(extreme ultraviolet) lithography tool that makes this

possible.

Designing at such small scales requires novel design and

simulation techniques,9 new packaging materials and

layouts, such as 3D stacking and heterogenous packaging, and new

testing techniques. In each one of these areas, we see incredible

feats of innovation and the early adoption of new tools and

techniques.

New design architectures could emerge that can potentially upend

the industry, exactly what happened when ARM embraced a different

architecture for mobile devices in contrast with Intel’s

approach at the same time. Additionally, on top of the complexity

of designing and manufacturing these small devices with repeated

and economically viable yields and cost at scale, the industry

faces increasingly harsher and more demanding requirements, such as

in automotive or consumer applications.

The industry complexity doesn’t show any sign of slowing

down and the players will need to continue investing resources in

the form of money and talent to remain competitive.

Industry and Geopolitical Dynamics: a Closer Look

As wonderfully recounted by Professor Chris Miller in his book

“Chip War: The Fight for the World’s Most Critical

Technology,” the semiconductor industry that was originally

encouraged by the U.S. government has evolved into a complex,

globally connected and highly interdependent business requiring

billions of dollars to continue to grow. Globalization in the

industry, companies locating certain steps of the supply chain in

lower-labor-cost and economically-friendly countries and businesses

specializing in specific sub-steps within the value chain made the

industry the size it is today.

Unfortunately, recent years’ events highlighted the

challenges resulting from such globalization and interdependence

coupled with the high costs that prevented any redundancy. Issues

ranging from climate-driven challenges that constrained water usage

at the leading foundry10 to global pandemics,

accidents11 and frigid winter conditions12

that forced the closure of key manufacturing facilities have

strained the existing supply chain.

This, in turn, triggered the panicked reaction of customers and

manufacturers that induced a massive bull-whip effect and huge

order backlogs. Geopolitical instability created another layer of

challenges. Prolonged wars have limited certain raw materials while

trade tariffs and outright trade limitations lowered or prevented

shipments of certain devices to specific countries and

customers.13

Governments all over the world have responded with investments

to prop up manufacturing on national soil, but this is unlikely to

completely solve the issue given the prohibitive amount of money

needed to open new Fabs. This opens the door for private investment

to step in and reap the benefits of expanding the ecosystem, as we

outlined in prior papers.

Implications on the Semiconductor Industry

The increased complexity and geopolitical uncertainty are

forcing companies to devise new ways to do business. The increased

costs to build new advanced manufacturing facilities have forced

companies to move past statements such as “real men have

Fabs.”14 Additionally, semiconductor talent is no

longer as easily available as it once was — the Semiconductor

Industry Association predicts a shortage of up to 67,000 workers by

203015 — and job opportunities have extended

beyond the core industry into automotive and technology companies,

thus increasing competition for the available talent. While there

was a time when Chinese customers represented a great new

opportunity for semiconductor companies, this situation has been

limited by trade restrictions and China’s development of its

own supply chain.

This is an opportunity for companies to think about their supply

chains, their investments, their customers and their talent in a

new way.

Challenges and Opportunities for the Industry and its

Investors

We recently discussed how the U.S. CHIPS Act is creating novel

investment opportunities for Private Equity investors both in the

U.S. and in Latin America.16 We now contend that

companies have the opportunity to rethink their overall business

strategies. For example, they can reconsider their go-to-market

approaches by updating which customers they serve and how, their

supply chain plans by deciding where to manufacture or source their

products, their R&D investments and their talent management

policies, among others.

As the industry changes, existing proven approaches may no

longer work in the sector; for example, employees’ benefits

structures and hiring processes might need to change and new growth

and investment areas might appear.

We believe that a time of change is a time of opportunity.

Join us as we explore the implications of the increased

complexity and uncertainty that the industry must navigate as it

grows toward the trillion-dollar mark.

Footnotes

2. NVIDIA Corporation – NVIDIA Announces Financial

Results for Fourth Quarter and Fiscal 2024

3. Sam Altman Seeks Trillions of Dollars to Reshape

Business of Chips and AI – WSJ

4. Intel Launches World’s First Systems Foundry

Designed for the AI Era :: Intel Corporation (INTC)

5. People want to buy EVs. Why are electric car sales

so sluggish? : NPR

6. China’s electric carmakers take on Europeans

on their own turf : NPR

9. What is AI Chip Design? – How it Works |

Synopsys

10. The Chip Shortage Is Bad. Taiwan’s Drought

Threatens to Make It Worse. – WSJ

11. Japan’s Renesas sees fire-damaged chip plant

back to full capacity by mid-June | Reuters

12. Severe Winter Weather In Texas Will Impact Many

Supply Chains Beyond Chips (forbes.com)

13. Exclusive: Russia’s attack on Ukraine halts

half of world’s neon output for chips | Reuters

14. Real men have fabs…or do they? – EE

Times

Originally published by 26 March, 2024

The content of this article is intended to provide a general

guide to the subject matter. Specialist advice should be sought

about your specific circumstances.

{kind=link}