")

blackred

A while ago, I wrote a cautious article on the BlackRock Innovation & Growth Term Trust (NYSE:BIGZ). At the time, we were in the midst of the 2022 equity bear market and risk appetites were being pulled back, so I did not think it was the best time to invest in the BIGZ fund given its risky venture capital-like portfolio.

In hindsight, November 2022 was near the lows of the equity bear market, markets have since rebounded to all-time highs. What about the performance of the BIGZ fund?

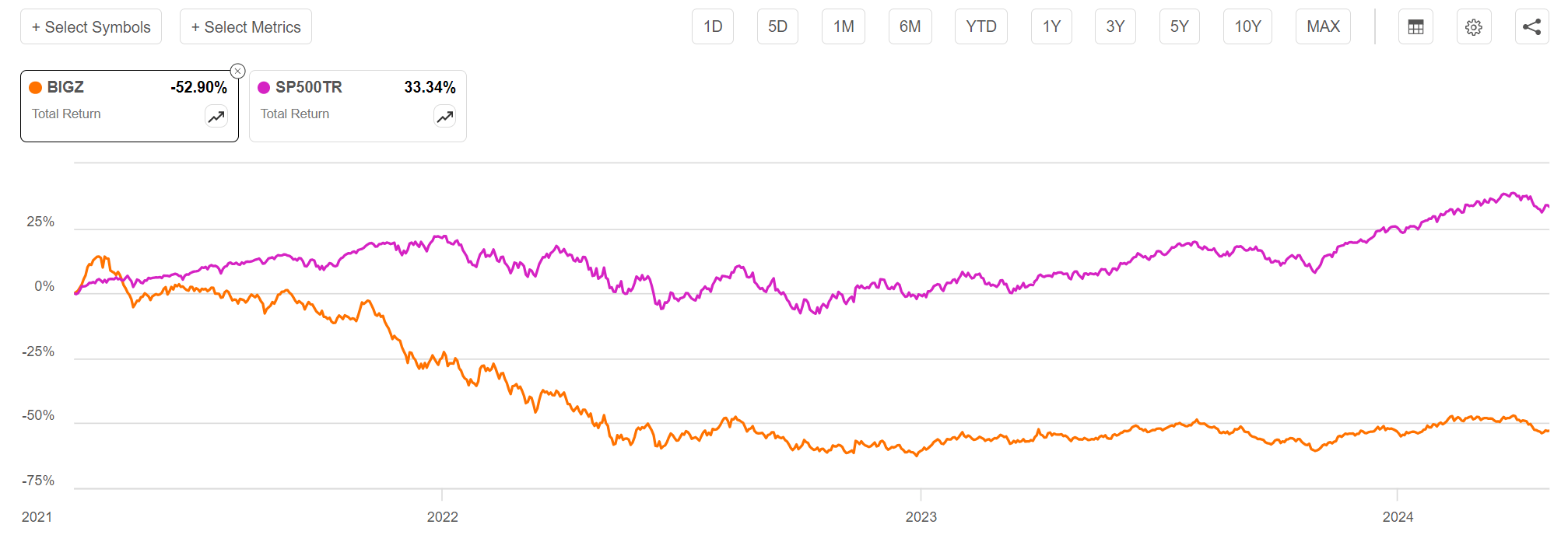

While the S&P 500 has rocketed to new all-time highs, the BIGZ fund is still more than 50% lower than its inception valuation, and almost 60% lower than its peak valuation (Figure 1). So my caution on the BIGZ was definitely warranted.

Figure 1 – BIGZ is still deeply underwater (Seeking Alpha)

In recent months, with the equity markets pushing to new highs, we have seen many high profile private companies come to the market, including Arm Holdings (ARM), Reddit (RDDT), and most recently, Rubrik (RBRK). With the IPO markets thawing, I thought it would be timely to revisit the BIGZ fund, to see if now might be a good time to invest in BIGZ and its venture capital portfolio.

Unfortunately, looking through BIGZ’s portfolio, there is not a lot to get excited about. Except for a few names, BIGZ’s venture portfolio appear to be a mishmash of venture companies that may struggle to find an exit in the current environment.

Until risk appetite for small-cap growth companies improve, I suggest staying on the sidelines.

Brief Fund Overview

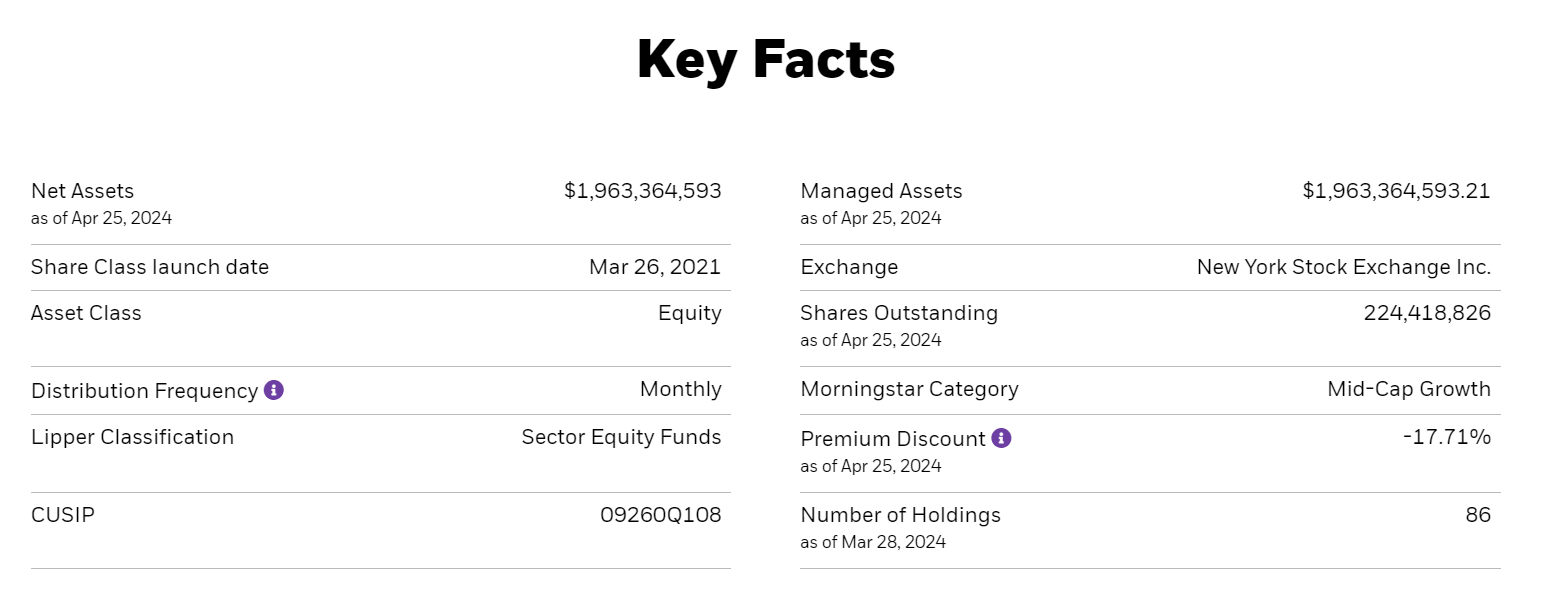

The BlackRock Innovation & Growth Term Trust is a closed-end fund (“CEF”) that primarily invests in small to mid-capitalization ‘innovative’ companies. With almost $2 billion in assets, the BIGZ fund is definitely on the larger side of closed-end funds (Figure 2).

Figure 2 – BIGZ overview (blackrock.com)

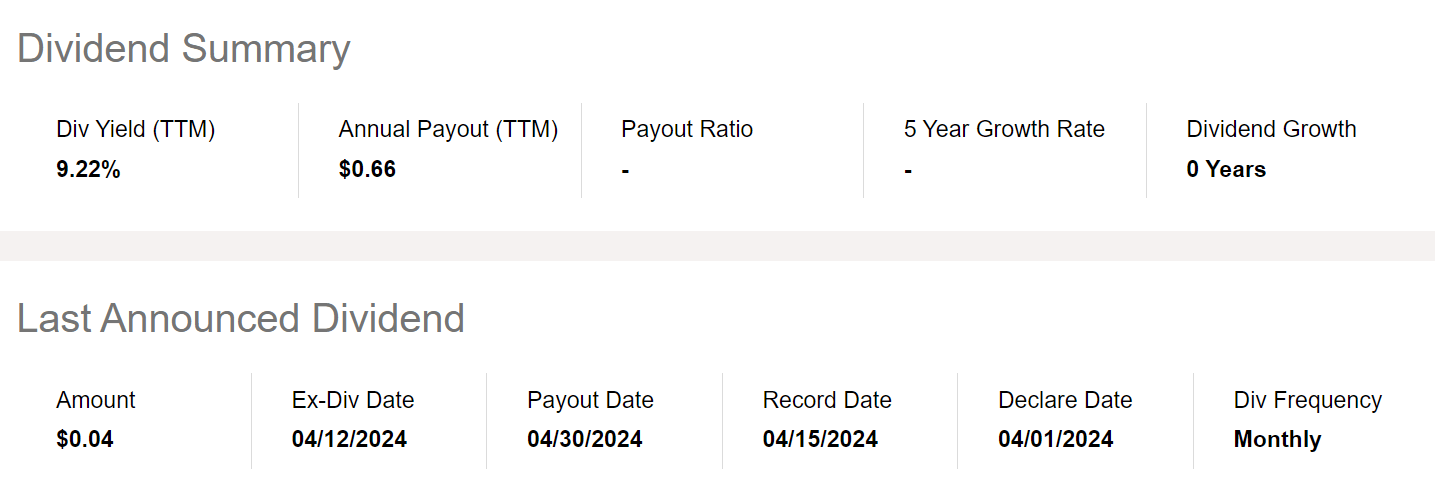

There are two main features that investors should be aware of for the BIGZ fund. First, for a fund that primarily invests in high growth ‘innovation’ companies, the BIGZ fund pays a very high distribution yield, with trailing 12 month distribution of $0.66 / share or 9.2% (Figure 3).

Figure 3 – BIGZ pays a high distribution yield (Seeking Alpha)

BIGZ Has Been Cutting Distributions

However, this trailing yield is misleading. As I noted in my prior article, the BIGZ fund does not earn sufficient income to support its yield, so its yield is actually funded from NAV amortizing ‘return of capital’ (“ROC”).

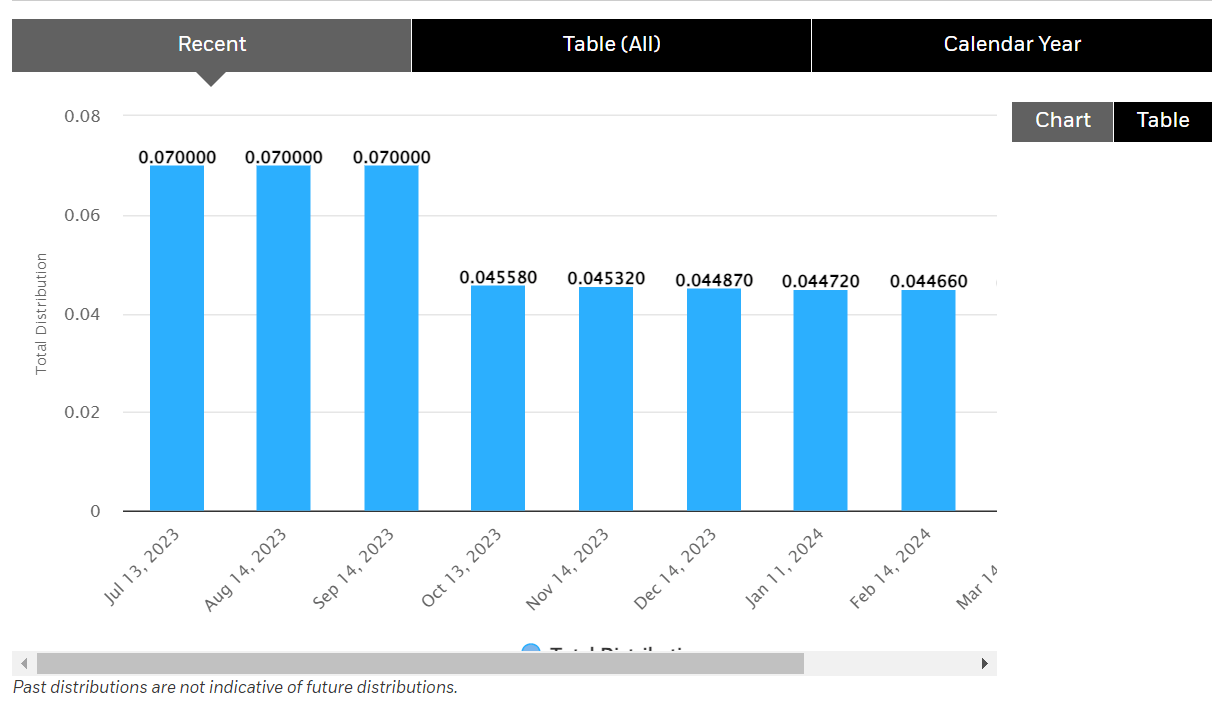

In order to stem its NAV erosion, the BIGZ fund had previously cut its monthly distribution from $0.10 / share at inception to $0.07 / share, and more recently, a variable ‘managed distribution’ that yields 6% on a rolling NAV (Figure 4).

Figure 4 – BIGZ has repeated cut its distribution (blackrock.com)

Although a distribution cut is certainly undesirable, I believe this move by management should actually be commended, as a variable distribution payment yielding 6% appears much more sustainable then a fixed distribution amount that eats away at NAV.

When the market turns and the BIGZ fund starts to generate positive returns, investors should expect to see their distributions grow along with the fund’s NAV.

Venture Capital Fund In Disguise

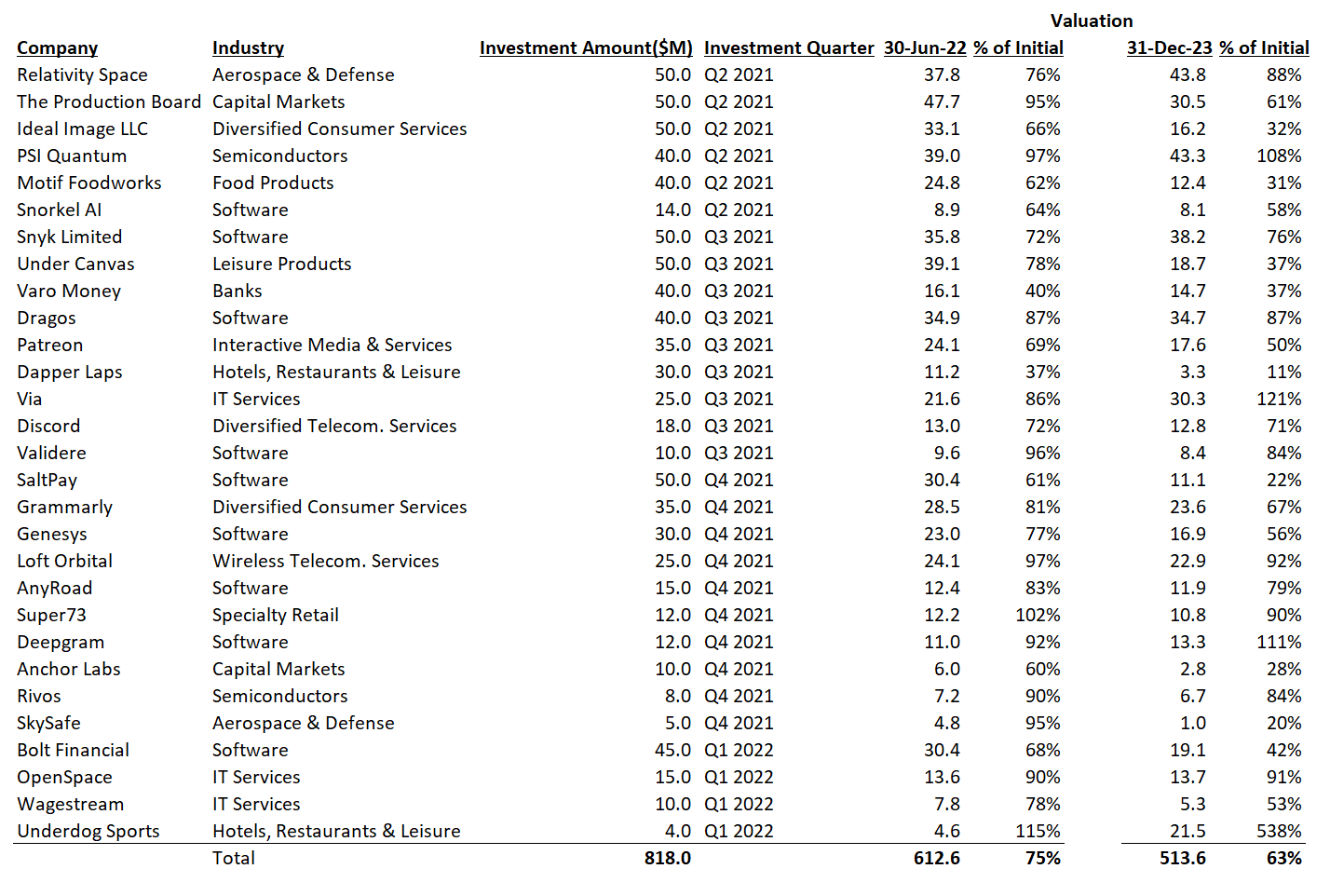

The other main feature of the BIGZ fund is its sizeable ‘private equity / venture capital’ portfolio. The fund stated aim is to invest up to 25% of assets into private investments and as of December 31, 2023, the fund held : 29 private companies that accounted for 25.3% of the portfolio.

As I have written, pre-IPO private investments can offer tremendous returns for early investors. For example, Sequoia Capital famously turned a $60 million investment in messaging app WhatsApp into $3 billion when the app was sold to Facebook in 2014. However, venture capital investing is also fraught with risks, as venture capital returns follow the Pareto principle, where 80% of returns come from 20% of the investments.

It is not uncommon to see venture capital funds lose money on most of its investments, but 1 or 2 home runs will ‘carry’ the portfolio to strong absolute returns. However, it is impossible to know beforehand which investment is going to be a winner and which is going to be a loser.

Furthermore, due to the unpredictable nature of exits, private equity investments are usually unavailable to mutual funds / ETFs, which require daily liquidity.

This is where BIGZ’s closed-end fund structure comes in handy. One feature of closed-fund funds is their ‘permanent capital’, i.e. when the funds are issued, the fund raises a certain amount of capital that permanently stays with the fund. Investors can buy or sell units of the fund just like a stock, and the price of the fund can fluctuate, but when investors sell, they are selling their units to another investor or to a dealer, and cash does not leave the fund.

Therefore, the closed-end fund structure is perfect for those looking to implement a venture capital / private equity strategy for retail investors.

Venture Portfolio Stagnant Since 2022

In my prior article, I noted that BIGZ’s privates portfolio was significantly underwater, with the whole portfolio trading at 75% of invested capital. Unfortunately, even with the passage of time, that figure has not improved. As of December 31, 2023, the privates portfolio was trading on average 63% of invested capital (Figure 5).

Figure 5 – BIGZ privates portfolio (Author created from fund commentary)

Furthermore, it is notable that even after 18 months, there has not been a single exit from this portfolio, even with booming equity markets. Undoubtedly, there are some potential high quality investments such as PSI Quantum, a quantum computing company, and Discord, an emerging messaging/social media platform, but the inability for these portfolio companies to find an exit raises the question of whether BIGZ’s ragtag group of investments are part of the 80% chaff or 20% gems in the pareto distribution.

Venture Capital Needs High Risk Appetites

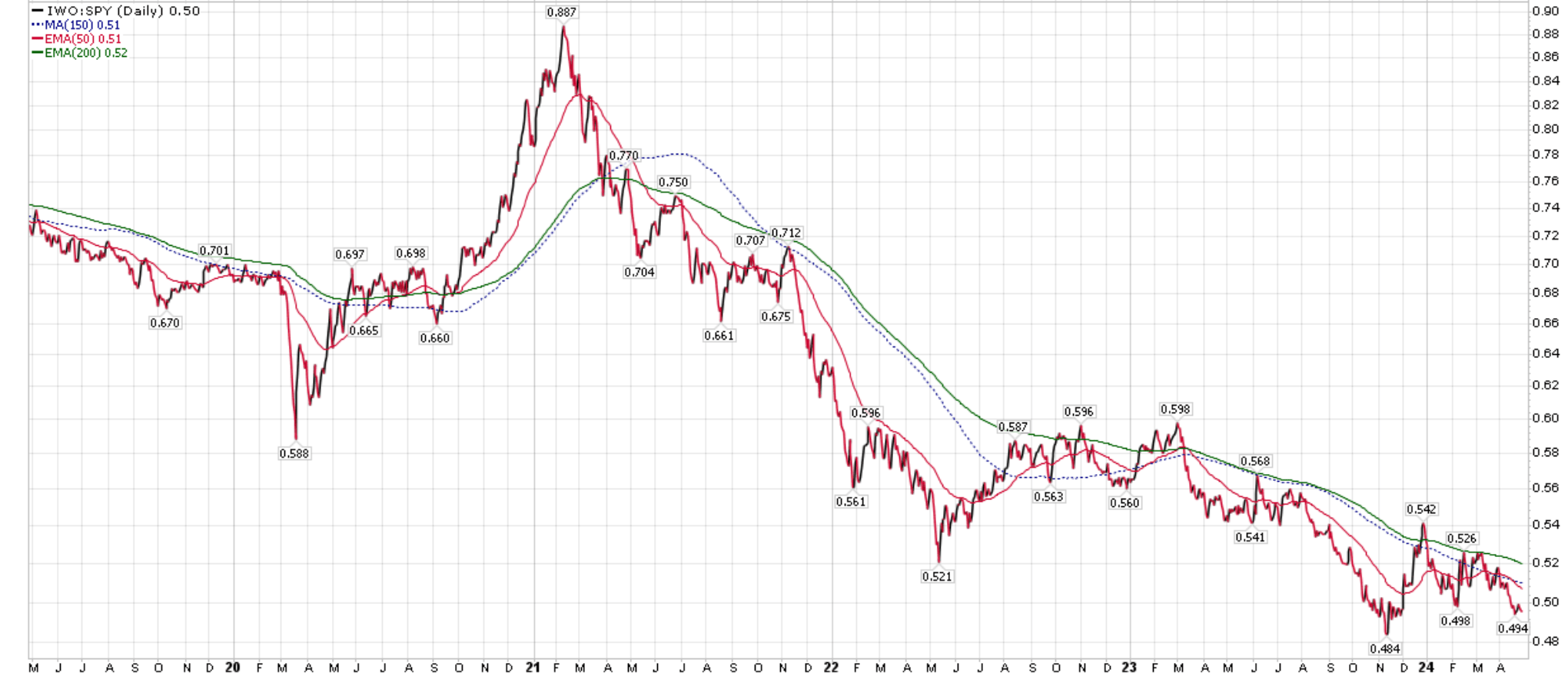

In fact, it is my long-held belief that high-risk investments like venture capital need buoyant risk appetites to truly outperform. So far, the equity market rally we have seen has been led by mega-cap companies like the ‘Magnificent 7’, and small-cap, growth companies have not really participated.

For example, the iShares Russell 2000 Growth ETF (IWO) has massively underperformed the SPDR S&P 500 ETF (SPY) since risk appetites peaked in early 2021 (Figure 6).

Figure 6 – IWO / SPY ratio (Author created with stockcharts.com)

Until this ratio turns up, it is hard to see the BIGZ fund outperforming.

Conclusion

The BlackRock Innovation & Growth Term Trust is a venture capital fund wrapped in a CEF structure. It holds a 25% allocation to private equity / venture capital investments that retail investors typically do not have access to.

Revisiting the fund after more than a year, I still do not see reason to be excited. The fund’s privates portfolio remains stagnant and has further decreased in value compared to my last update from late 2022. Despite buoyant equity markets, BIGZ’s privates have not been able to find exits. This is a red flag.

As we know, venture investing follows the pareto distribution where 80% of returns are generated from 20% of investments. While BIGZ’ portfolio certainly includes some high potential investments like PSI Quantum, I fear it may have a higher chaff/gem ratio than normal, since its investments were mostly made at the peak of the cycle.

I remain cautious on BIGZ until risk appetites for small-cap growth investments turn higher such that BIGZ’s private investments can find exits. Investors can monitor this using the ratio between the IWO ETF and the SPY ETF.

{kind=link}