Venture capital (VC) funding increased by 11% in Q1 2024, driven by massive deals in generative artificial intelligence (gen AI), including Amazon’s US$2.75 billion investment in Anthropic and Alibaba’s US$2.5 billion investment in Moonshot AI, new data released by business analytics platform CB Insights show.

This surge underscores the ongoing enthusiasm for gen AI among investors, with major tech players viewing it as a pivotal innovation catalyst, promising efficiency enhancements and new market opportunities.

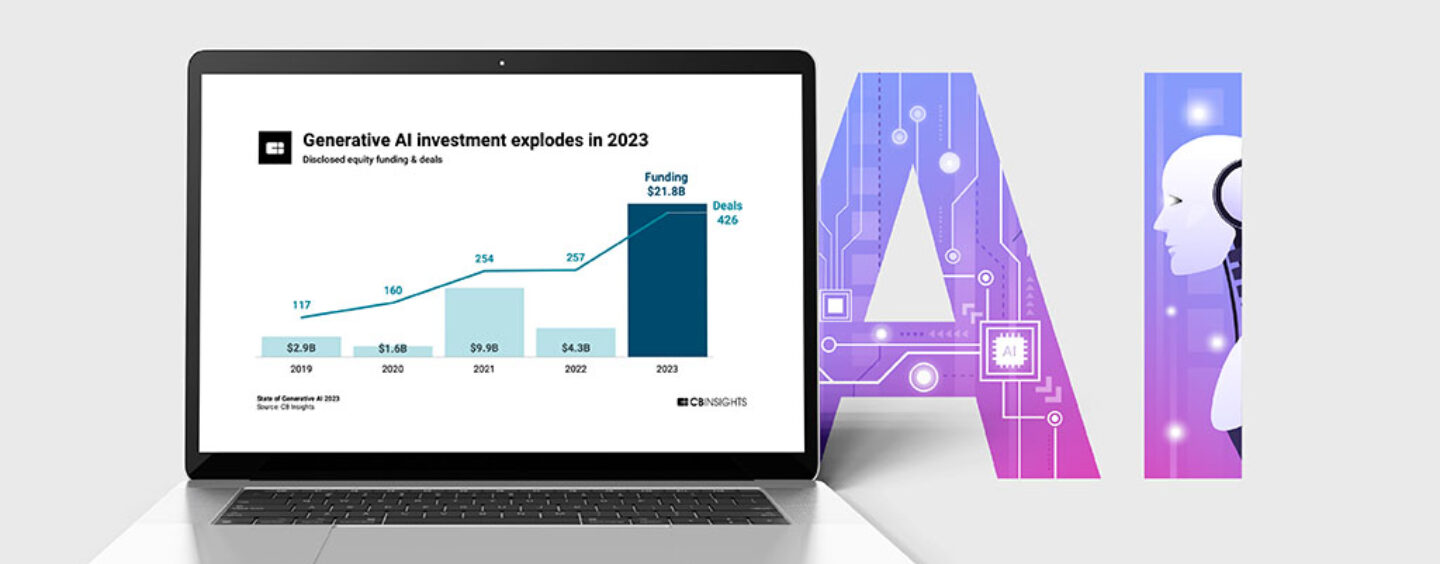

This momentum in gen AI builds on the sector’s remarkable performance in 2023 during which VC funding shot up five times compared to the previous year while deals increased by 66%. In 2023, gen AI startups amassed a record-breaking US$21.8 billion across 426 deals, data from CB Insights reveal, with the largest deals going to OpenAI (US$10 billion), Inflection AI (US$1.3 billion), Anthropic (US$1.8 billion), Databricks (US$504 million) and Aleph Alpha (US$500 million).

Disclosed generative AI equity funding and deals, Source: State of Generate AI 2023, CB Insights, Feb 2024

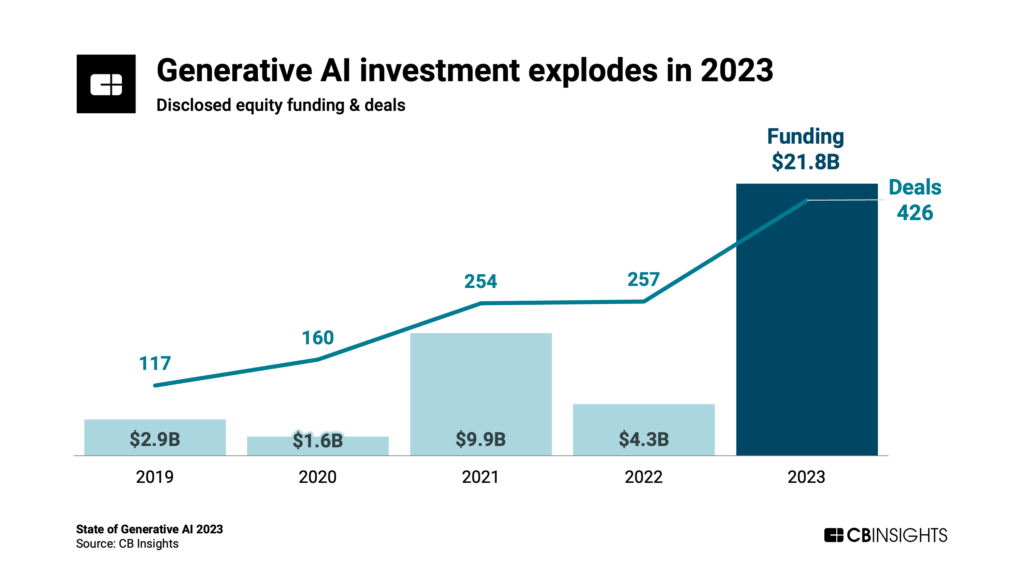

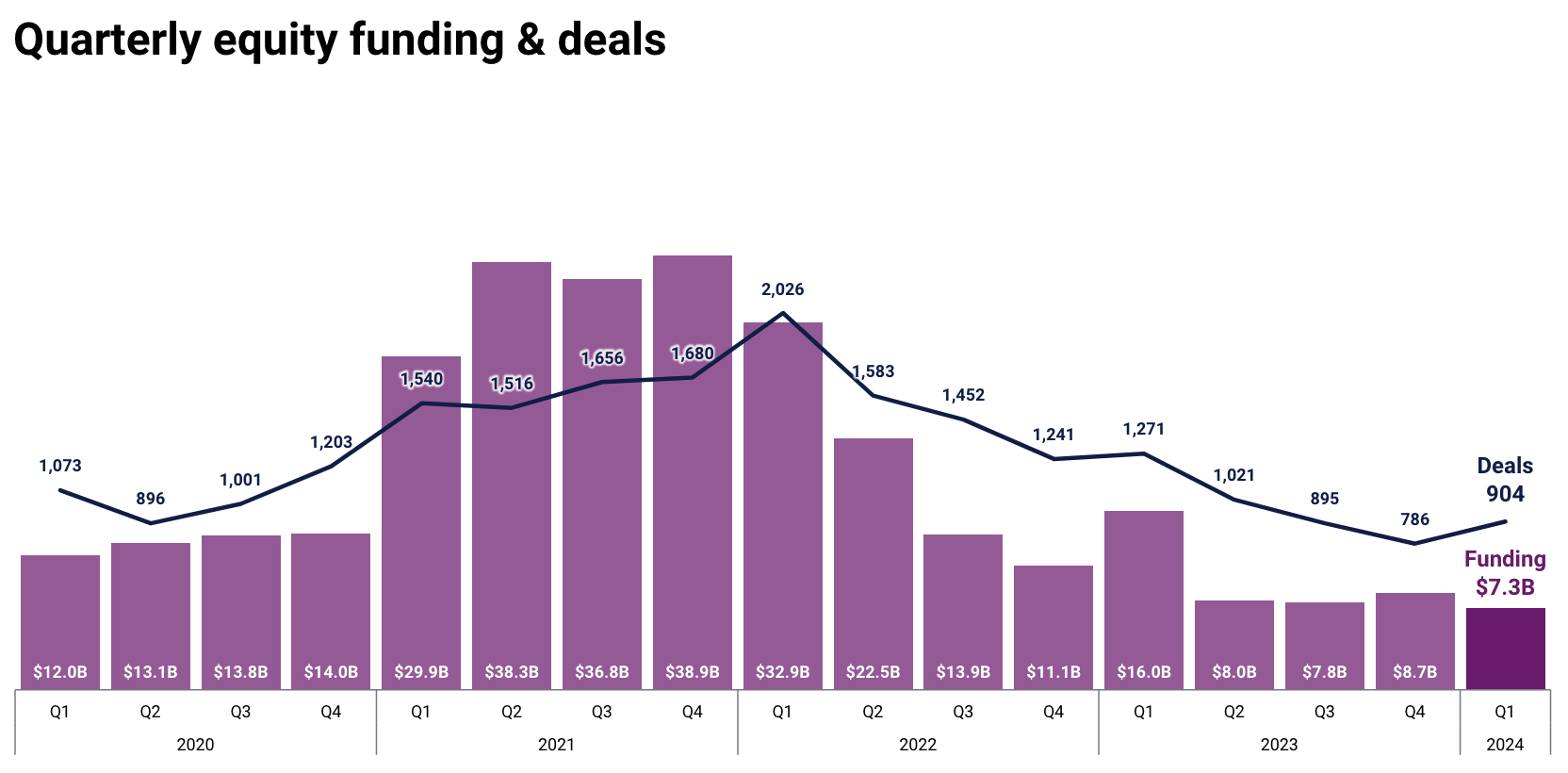

Booming investment activity in gen AI helped sustain global VC funding, which increased slightly in Q1 2024 and reached US$58.4 billion, up from US$52.8 billion in Q4 2023, the data show. However, the figure represents a 21% year-over-year (YoY) decline compared to Q1 2023’s US$74 billion, putting quarterly VC funding roughly where it was in 2017.

Quarterly equity funding and deals, Source: State of Venture Q1 2024, CB Insights, Apr 2024

Meanwhile, VC dealmaking continued to decline in Q1 2024, slipping for an eighth straight quarter and falling 7% quarter-on-quarter (QoQ) to 6,238. Asia and Europe saw 8% and 9% declines, respectively, in VC deal activity, while the US bucked the global trend, seeing deals tick up 1% QoQ.

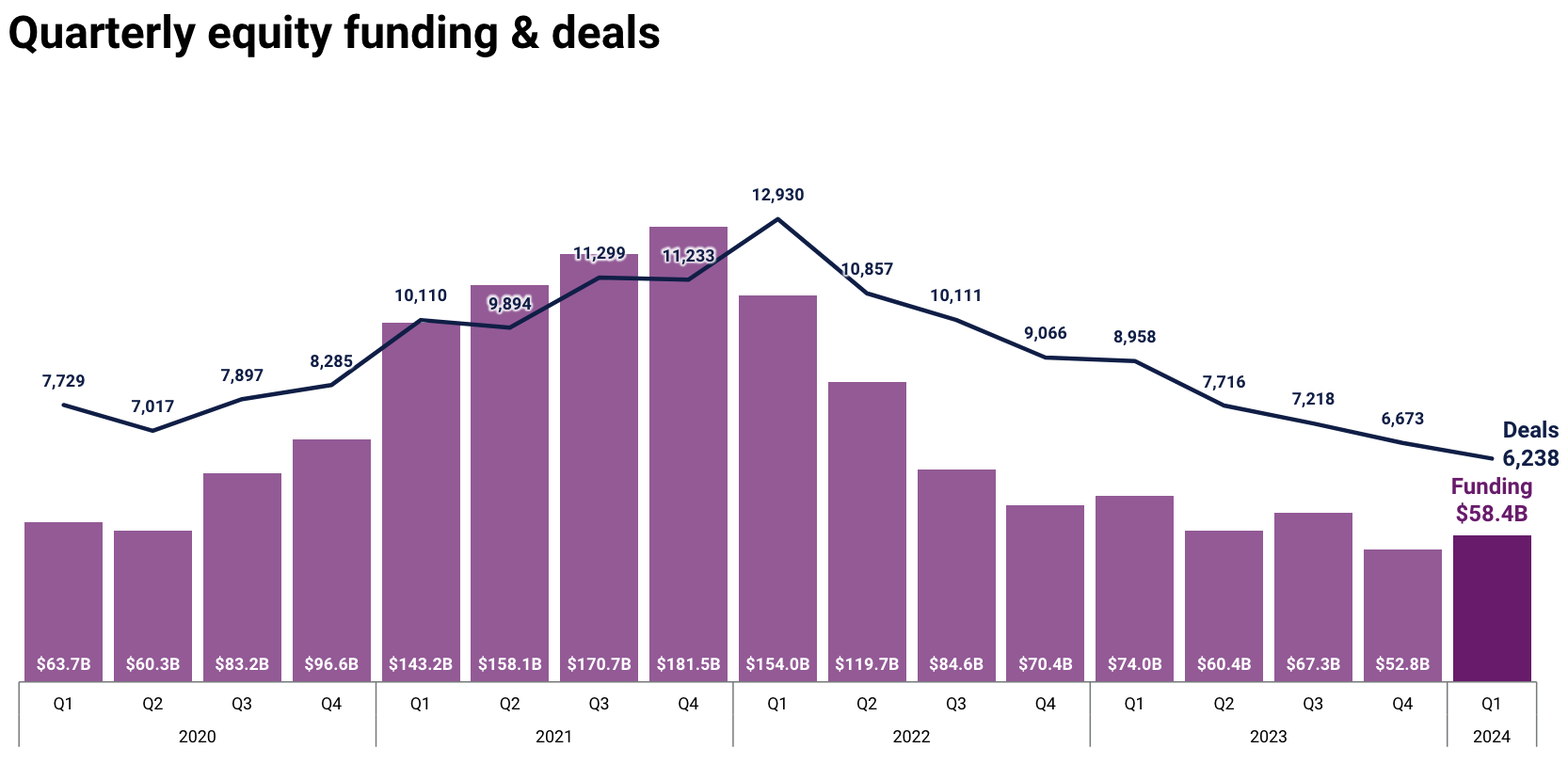

Mega-rounds rise 30%

VC rounds worth US$100 million and over, also known as mega-rounds, were the bright spot in Q1 2024, increasing by 30% quarter-over-quarter (QoQ) and by 14% YoY to reach 105 rounds. Corporate investors like Amazon, Disney, and Alibaba were behind some of the quarter’s largest rounds, pointing to investors’ sustained interest in blockbuster deals in capital-intensive areas, the report says.

At US$26.2 billion, funding from mega-rounds represented 45% of Q1 2024’s total funding, a rebound from 34% in Q4 2023.

Quarterly mega-rounds as percent of funding, Source: State of Venture Q1 2024, CB Insights, Apr 2024

Q1 2024 saw 19 startups reach unicorn status, down slightly from 23 in Q4 2023. These new billion-dollar companies were distributed across the US (8 new unicorns), Asia (6), and Europe (5).

Europe’s total, which represented a five-quarter high in unicorn births for the continent, included new unicorns like Italy’s Bending Spoons (US$2.6 billion valuation) and Netherlands-based Mews (US$1.2 billion).

Fintech faces decline

Data from CB Insights show that the fintech sector experienced a setback. In Q1 2024, fintech startups amassed a total of US$7.3 billion through 904 VC rounds, down 16% from US$8.7 billion in Q4 2023 but up 13% from 786 deals. The figures represent a 119% YoY decline in VC funding and a 40.6% YoY decline in deal count.

Quarterly fintech equity funding and deals, Source: State of Fintech Q1 2024, CB Insights, Apr 2024

The fintech sector also saw its new unicorn count slip from eight in Q4 2023 to six in Q1 2024. Notable additions to the unicorn club in Q1 2024 include HashKey from Hong Kong, Mews and DataSnipper from the Netherlands, Uzum from Uzbekistan, Perfios from India and Polyhedra Network from the US.

Europe stood out as the only major global region to see fintech funding increase in Q1 2024, growing by 22% QoQ to US$2.2 billion. In the continent, the UK and the Netherlands secured some of the quarter’s biggest deals, with examples including Monzo’s US$431 million Series I (UK), Flagstone’s US$139 million round (UK), Mews’ US$110 million Series D (Netherlands), and DataSnipper’s US$100 million Series B (Netherlands).

The quarterly funding decline in the fintech sector reflects a continued downward trend observed in the global fintech funding landscape in 2022 and 2023. This trend has been driven by economic uncertainties, soaring inflation and a looming global recession. Global fintech funding dropped by 50% in 2023, falling from US$78.6 billion in 2022 to US$39.2 billion. These figures are a far cry from the record of US$140.8 billion secured in 2021.

Featured image credit: Edited from freepik

{kind=link}