UNITED

STATES SECURITIES AND EXCHANGE COMMISSION Washington, D.C. 20549

FORM

N-CSR

CERTIFIED

SHAREHOLDER REPORT OF REGISTERED MANAGEMENT INVESTMENT COMPANIES

Investment

Company Act file number: 811-21831

ALTERNATIVE

INVESTMENT PARTNERS ABSOLUTE RETURN FUND STS

(Exact

name of Registrant as specified in Charter)

100

Front Street, Suite 400 West Conshohocken, Pennsylvania 19428-2881

(Address

of principal executive offices)

Registrant’s

Telephone Number, including Area Code: (610) 260-7600

Kara

Fricke, Esq. Morgan Stanley Investment Management Inc. 1633 Broadway New York, New York 10019

(Name

and address of agent for service)

COPY

TO:

Allison

M. Fumai, Esq. DECHERT LLP 1095 Avenue of the Americas New York, NY 10036-6797 (212) 698-3500

Date of fiscal year

end: December 31

Date of reporting

period: December 31, 2023

ITEM

1.

REPORTS

TO STOCKHOLDERS. The Registrant’s annual report transmitted to shareholders

pursuant to Rule 30e-1 under the Investment Company Act of 1940 is as follows:

ALTERNATIVE INVESTMENT PARTNERS

ABSOLUTE RETURN FUND STS

Consolidated Financial Statements with Report of

Independent Registered Public Accounting Firm

For the Year Ended December 31, 2023

Oath and Affirmation

To the best of my knowledge and belief, the information contained in this document is accurate and

complete.

Lee Spector, Executive Director of Morgan Stanley Alternative Investment LLC, the General Partner

of Morgan Stanley AIP GP LP, the Commodity Pool Operator of Alternative Investment Partners

Absolute Return Fund STS

(This oath is required by Section 4.12(c)(3) of the Commodity Futures Trading Commission Regulations under the

Commodity Exchange Act, as amended.)

Audited financial statements for Alternative Investment Partners Absolute Return Fund for the year ended December 31, 2023

are attached to these consolidated financial statements and are an integral part thereof.

Alternative Investment Partners Absolute Return Fund STS

Consolidated Financial Statements with Report of Independent

Registered Public Accounting Firm

For the Year Ended December 31, 2023

Contents

Management’s Discussion of Fund Performance (Unaudited)………………………………………1

Report of Independent Registered Public Accounting Firm …………………………………………………….. 4

Audited Consolidated Financial Statements

Consolidated Statement of Assets and Liabilities …………………………………………………………………… 5

Consolidated Statement of Operations ………………………………………………………………………………….. 6

Consolidated Statements of Changes in Net Assets ………………………………………………………………… 7

Consolidated Statement of Cash Flows ………………………………………………………………………………… 8

Notes to Consolidated Financial Statements ………………………………………………………………………….. 9

Proxy Voting Policies and Procedures and Proxy Voting Record (Unaudited) …………………………. 15

Quarterly Portfolio Schedule (Unaudited) …………………………………………………………………………… 15

Information Concerning Trustees and Officers (Unaudited) ………………………………………………….. 16

1

Alternative Investment Partners Absolute Return Fund STS

Management’s Discussion of Fund Performance

Investment Objective and Strategy Summary

Alternative Investment Partners Absolute Return Fund STS’s (the “Fund”) investment objective is to seek

capital appreciation.

The Fund, through the investment of substantially all of its assets in Alternative Investment Partners

Absolute Return Fund (the “Master Fund”), invests substantially all its assets in private investment funds

(commonly referred to as hedge funds) that are managed by a select group of alternative investment

managers that employ different “absolute return” investment strategies in pursuit of attractive risk-adjusted returns consistent with the preservation of capital. “Absolute return” refers to a broad class of

investment strategies that are managed without reference to the performance of equity, debt and other

markets. “Absolute return” investment strategies allow unaffiliated third-party investment managers the

flexibility to use leveraged or short-sale positions to take advantage of perceived inefficiencies across the

global capital markets. These strategies are in contrast to the investment programs of “traditional”

registered investment companies, such as mutual funds. Absolute return strategies can be contrasted with

“relative return strategies” which generally seek to outperform a corresponding benchmark equity or fixed

income index. The Master Fund seeks attractive “risk-adjusted” returns, which are returns adjusted to take

into account the volatility of those returns. The Master Fund intends to invest in private investment funds

that employ the following principal strategies: relative value strategies, security selection strategies,

specialist credit strategies and directional strategies.

Performance Discussion

Total Returns

One Year Five Years Ten Years

Alternative Investment Partners Absolute Return Fund STS 5.75% 6.30% 4.47%

Average Annual

2

Alternative Investment Partners Absolute Return Fund STS

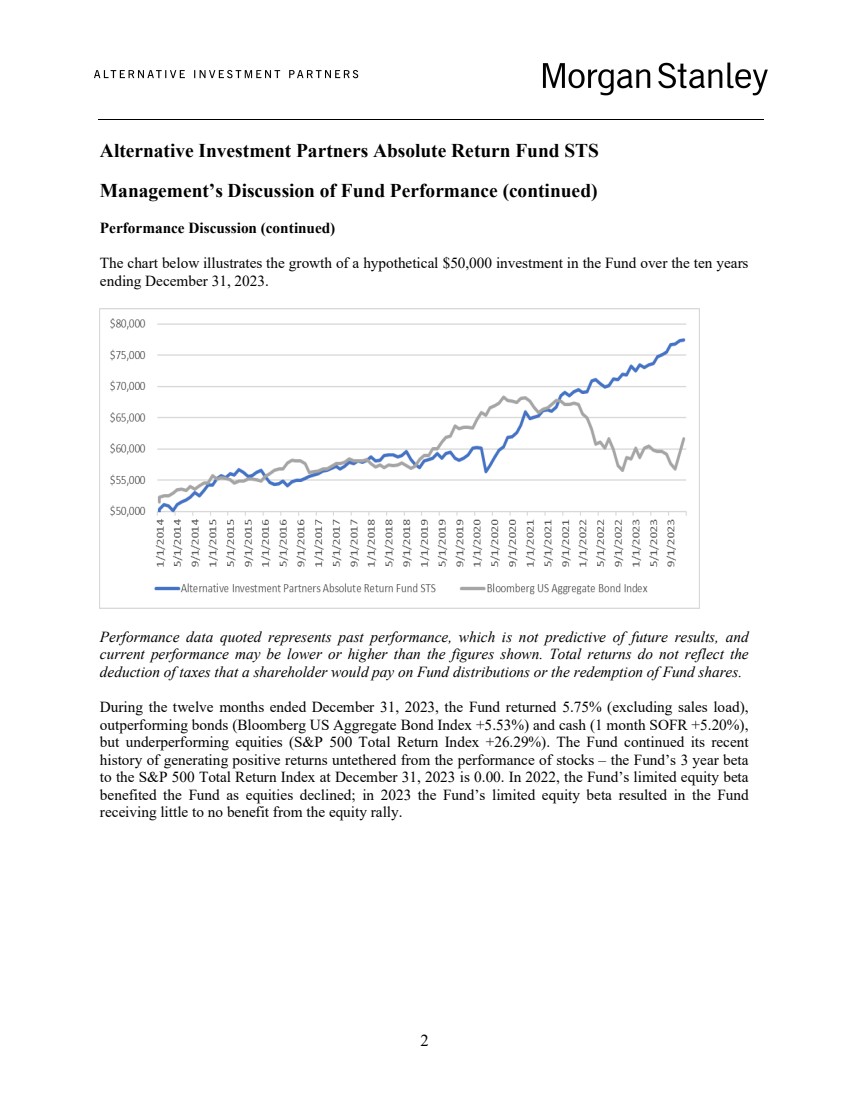

Management’s Discussion of Fund Performance (continued)

Performance Discussion (continued)

The chart below illustrates the growth of a hypothetical $50,000 investment in the Fund over the ten years

ending December 31, 2023.

Performance data quoted represents past performance, which is not predictive of future results, and

current performance may be lower or higher than the figures shown. Total returns do not reflect the

deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares.

During the twelve months ended December 31, 2023, the Fund returned 5.75% (excluding sales load),

outperforming bonds (Bloomberg US Aggregate Bond Index +5.53%) and cash (1 month SOFR +5.20%),

but underperforming equities (S&P 500 Total Return Index +26.29%). The Fund continued its recent

history of generating positive returns untethered from the performance of stocks – the Fund’s 3 year beta

to the S&P 500 Total Return Index at December 31, 2023 is 0.00. In 2022, the Fund’s limited equity beta

benefited the Fund as equities declined; in 2023 the Fund’s limited equity beta resulted in the Fund

receiving little to no benefit from the equity rally.

3

Alternative Investment Partners Absolute Return Fund STS

Management’s Discussion of Fund Performance (continued)

Performance Discussion (continued)

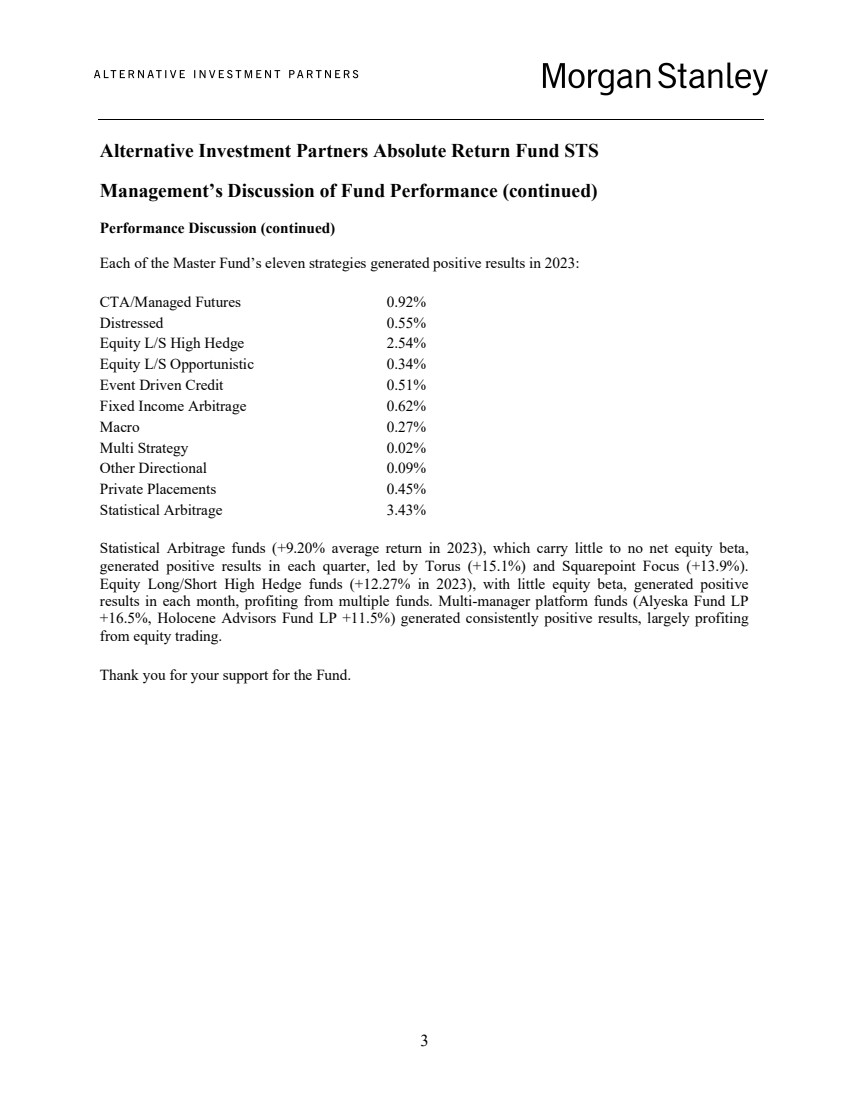

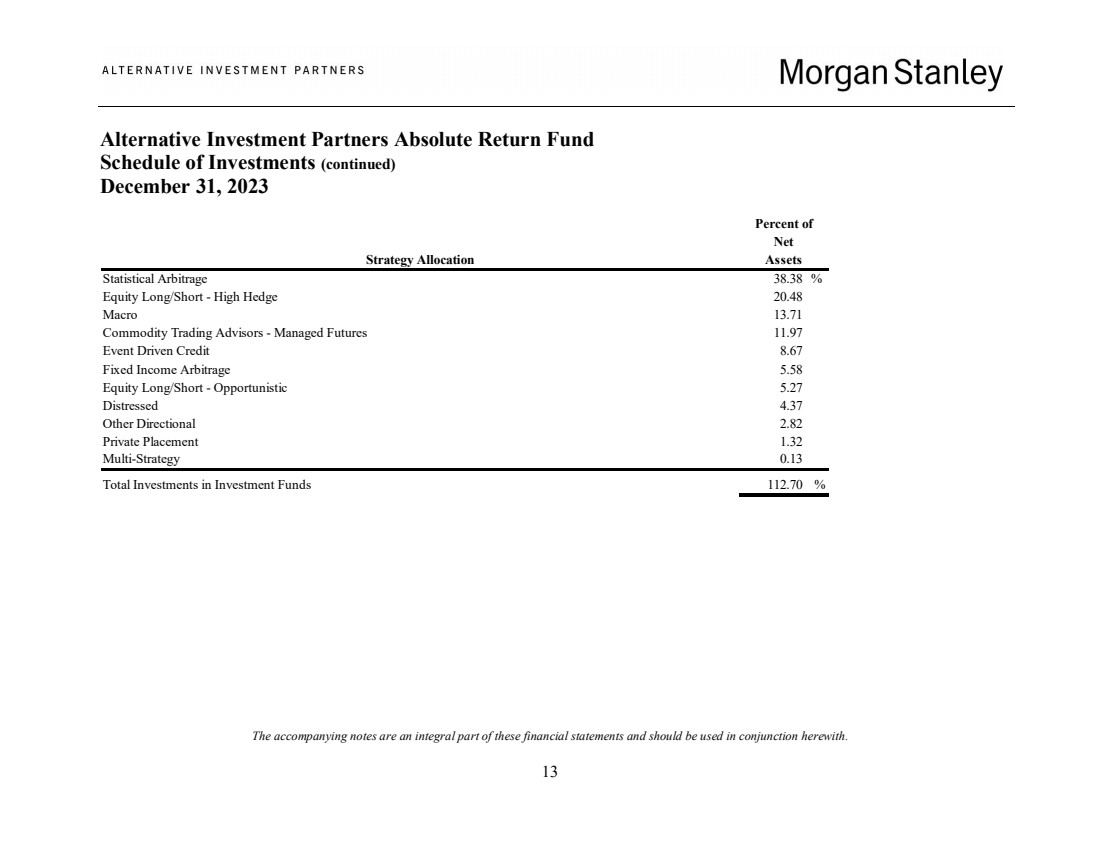

Each of the Master Fund’s eleven strategies generated positive results in 2023:

CTA/Managed Futures 0.92%

Distressed 0.55%

Equity L/S High Hedge 2.54%

Equity L/S Opportunistic 0.34%

Event Driven Credit 0.51%

Fixed Income Arbitrage 0.62%

Macro 0.27%

Multi Strategy 0.02%

Other Directional 0.09%

Private Placements 0.45%

Statistical Arbitrage 3.43%

Statistical Arbitrage funds (+9.20% average return in 2023), which carry little to no net equity beta,

generated positive results in each quarter, led by Torus (+15.1%) and Squarepoint Focus (+13.9%).

Equity Long/Short High Hedge funds (+12.27% in 2023), with little equity beta, generated positive

results in each month, profiting from multiple funds. Multi-manager platform funds (Alyeska Fund LP

+16.5%, Holocene Advisors Fund LP +11.5%) generated consistently positive results, largely profiting

from equity trading.

Thank you for your support for the Fund.

4

Report of Independent Registered Public Accounting Firm

To the Shareholders and Board of Trustees of Alternative Investment Partners Absolute Return Fund STS

Opinion on the Financial Statements

We have audited the accompanying consolidated statement of assets and liabilities of Alternative Investment

Partners Absolute Return Fund STS (the “Fund”), as of December 31, 2023, and the related consolidated

statements of operations and cash flows for the year then ended, the consolidated statements of changes in net

assets for each of the two years in the period then ended and the related notes (collectively referred to as the

“financial statements”). In our opinion, the financial statements present fairly, in all material respects, the

consolidated financial position of the Fund at December 31, 2023, the consolidated results of its operations and

its cash flows for the year then ended and the consolidated changes in its net assets for each of the two years in

the period then ended, in conformity with U.S. generally accepted accounting principles.

Basis for Opinion

These financial statements are the responsibility of the Fund’s management. Our responsibility is to express an

opinion on the Fund’s financial statements based on our audits. We are a public accounting firm registered with

the Public Company Accounting Oversight Board (United States) (“PCAOB”) and are required to be

independent with respect to the Fund in accordance with the U.S. federal securities laws and the applicable rules

and regulations of the Securities and Exchange Commission and the PCAOB.

We conducted our audits in accordance with the standards of the PCAOB. Those standards require that we plan

and perform the audit to obtain reasonable assurance about whether the financial statements are free of material

misstatement, whether due to error or fraud. The Fund is not required to have, nor were we engaged to perform,

an audit of the Fund’s internal control over financial reporting. As part of our audits, we are required to obtain

an understanding of internal control over financial reporting but not for the purpose of expressing an opinion on

the effectiveness of the Fund’s internal control over financial reporting. Accordingly, we express no such

opinion.

Our audits included performing procedures to assess the risks of material misstatement of the financial

statements, whether due to error or fraud, and performing procedures that respond to those risks. Such procedures

included examining, on a test basis, evidence regarding the amounts and disclosures in the financial statements.

Our procedures included confirmation of investments owned as of December 31, 2023, by correspondence with

the transfer agent. Our audits also included evaluating the accounting principles used and significant estimates

made by management, as well as evaluating the overall presentation of the financial statements. We believe that

our audits provide a reasonable basis for our opinion.

We have served as the auditor of one or more Morgan Stanley investment companies since 2000.

Boston, Massachusetts

February 29, 2024

See accompanying notes and attached audited financial statements for Alternative Investment Partners Absolute Return Fund.

5

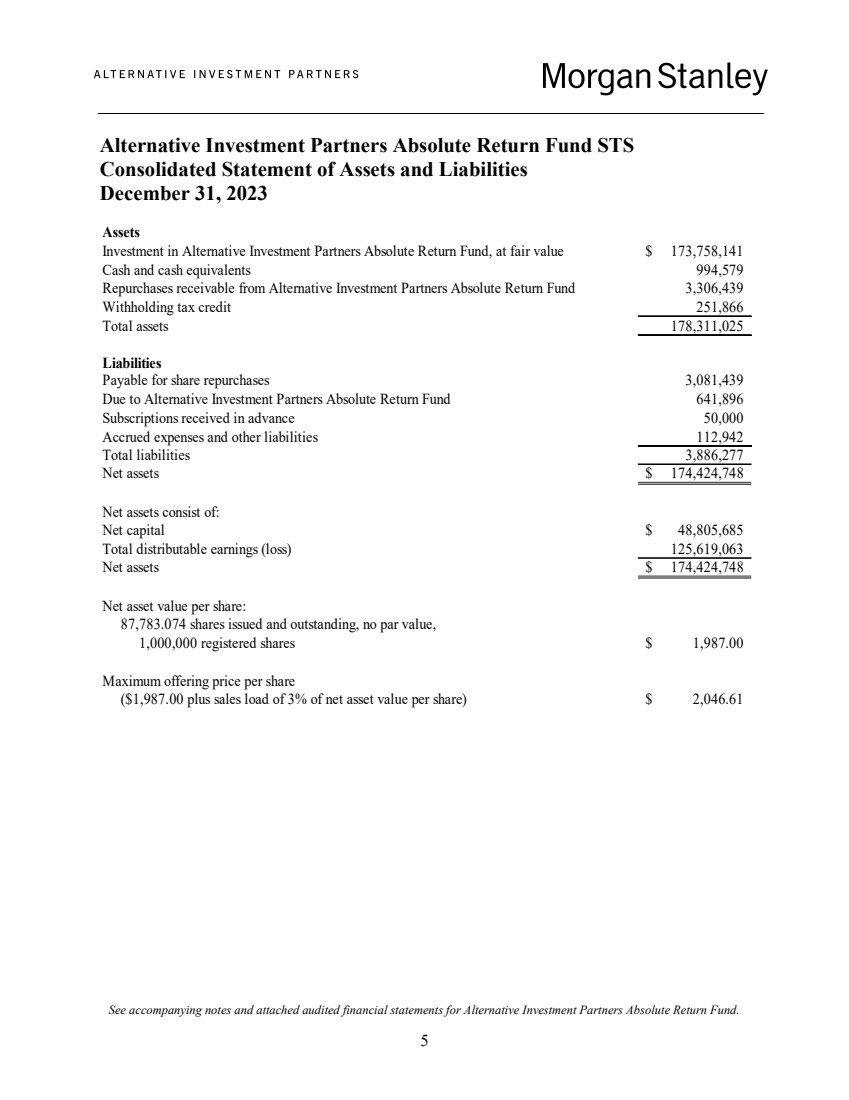

Alternative Investment Partners Absolute Return Fund STS

Consolidated Statement of Assets and Liabilities

December 31, 2023

Assets

Investment in Alternative Investment Partners Absolute Return Fund, at fair value 173,758,141 $

Cash and cash equivalents 994,579 Repurchases receivable from Alternative Investment Partners Absolute Return Fund 3,306,439 Withholding tax credit 251,866

Total assets 178,311,025 Liabilities

Payable for share repurchases 3,081,439

Due to Alternative Investment Partners Absolute Return Fund 641,896 Subscriptions received in advance 50,000 Accrued expenses and other liabilities 112,942

Total liabilities 3,886,277 Net assets $ 174,424,748

Net assets consist of:

Net capital 48,805,685 $

Total distributable earnings (loss) 125,619,063 Net assets $ 174,424,748

Net asset value per share:

87,783.074 shares issued and outstanding, no par value,

1,000,000 registered shares 1,987.00 $

Maximum offering price per share

($1,987.00 plus sales load of 3% of net asset value per share) 2,046.61 $

See accompanying notes and attached audited financial statements for Alternative Investment Partners Absolute Return Fund.

6

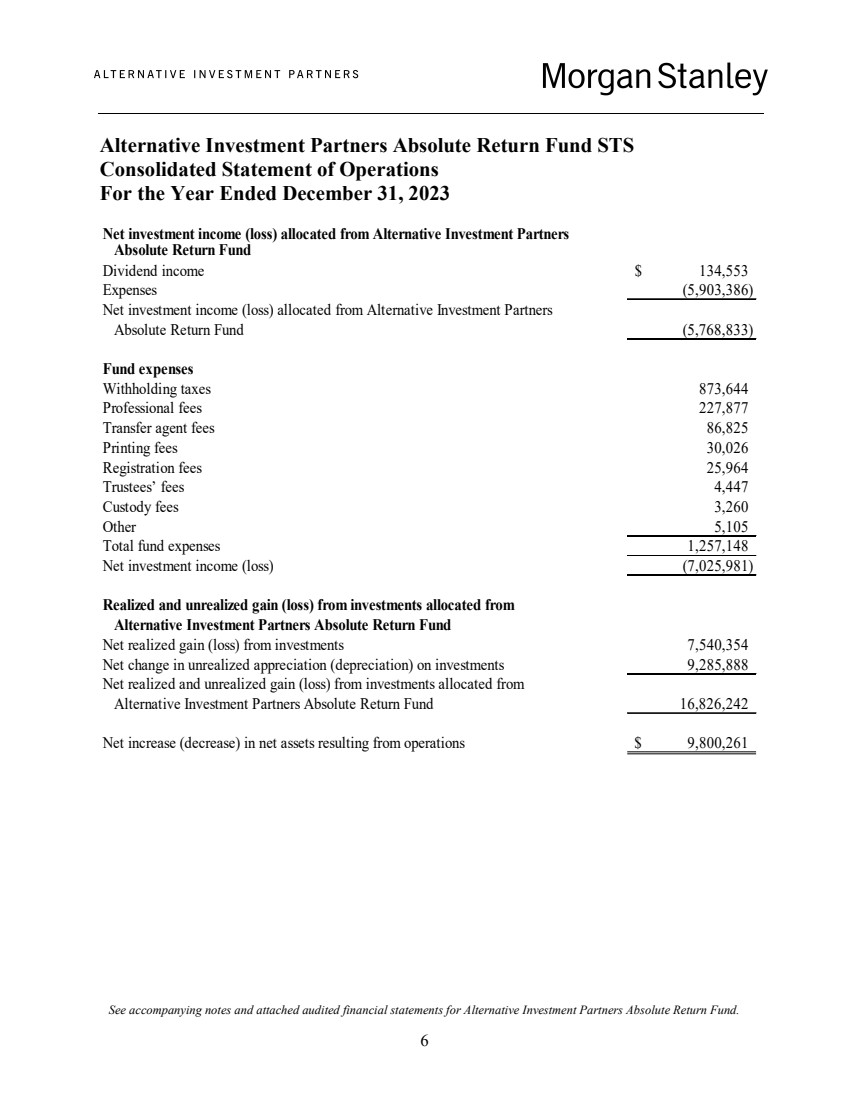

Alternative Investment Partners Absolute Return Fund STS

Consolidated Statement of Operations

For the Year Ended December 31, 2023

Net investment income (loss) allocated from Alternative Investment Partners

Absolute Return Fund

Dividend income 134,553 $

Expenses (5,903,386) Net investment income (loss) allocated from Alternative Investment Partners

Absolute Return Fund (5,768,833)

Fund expenses

Withholding taxes 873,644 Professional fees 227,877

Transfer agent fees 86,825 Printing fees 30,026

Registration fees 25,964

Trustees’ fees 4,447 Custody fees 3,260

Other 5,105

Total fund expenses 1,257,148 Net investment income (loss) (7,025,981) Realized and unrealized gain (loss) from investments allocated from

Alternative Investment Partners Absolute Return Fund

Net realized gain (loss) from investments 7,540,354 Net change in unrealized appreciation (depreciation) on investments 9,285,888 Net realized and unrealized gain (loss) from investments allocated from

Alternative Investment Partners Absolute Return Fund 16,826,242 Net increase (decrease) in net assets resulting from operations 9,800,261 $

See accompanying notes and attached audited financial statements for Alternative Investment Partners Absolute Return Fund.

7

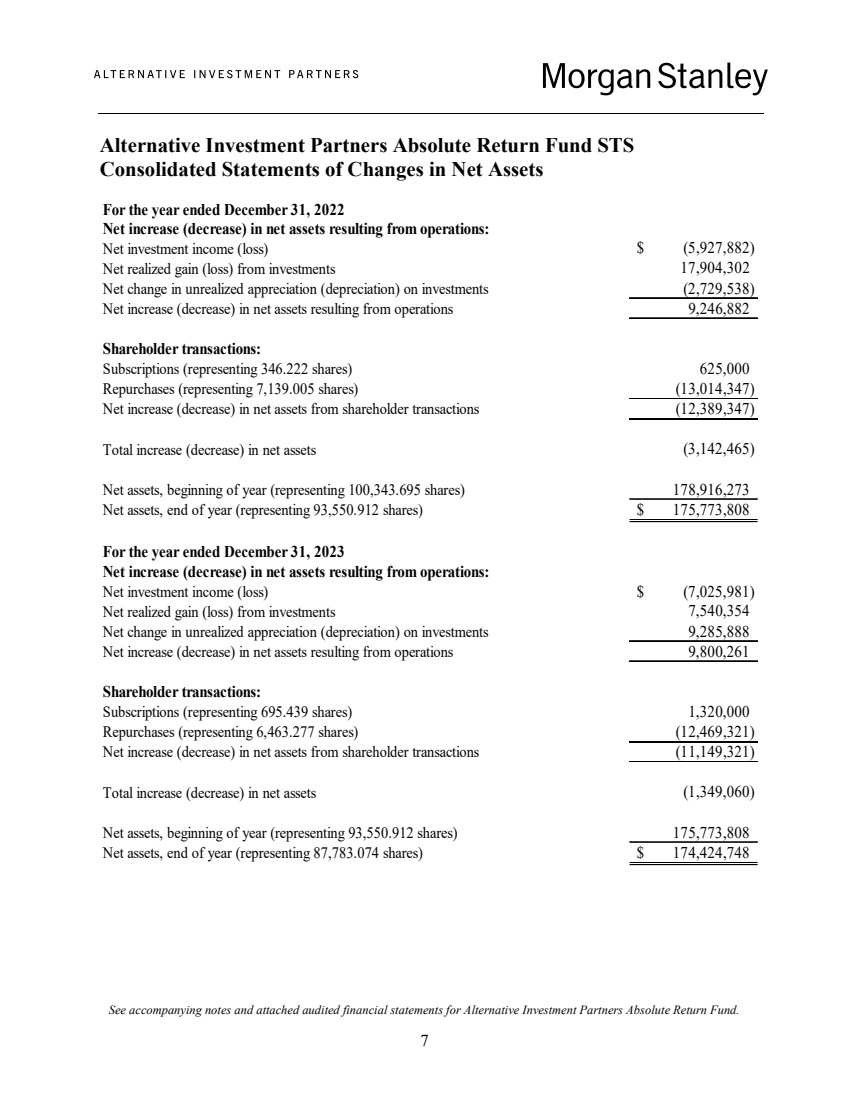

Alternative Investment Partners Absolute Return Fund STS

Consolidated Statements of Changes in Net Assets

For the year ended December 31, 2022

Net increase (decrease) in net assets resulting from operations:

Net investment income (loss) $ (5,927,882)

Net realized gain (loss) from investments 17,904,302

Net change in unrealized appreciation (depreciation) on investments (2,729,538)

Net increase (decrease) in net assets resulting from operations 9,246,882

Shareholder transactions:

Subscriptions (representing 346.222 shares) 625,000

Repurchases (representing 7,139.005 shares) (13,014,347)

Net increase (decrease) in net assets from shareholder transactions (12,389,347)

Total increase (decrease) in net assets (3,142,465)

Net assets, beginning of year (representing 100,343.695 shares) 178,916,273

Net assets, end of year (representing 93,550.912 shares) $ 175,773,808

Net increase (decrease) in net assets resulting from operations:

Net investment income (loss) $ (7,025,981)

Net realized gain (loss) from investments 7,540,354

Net change in unrealized appreciation (depreciation) on investments 9,285,888

Net increase (decrease) in net assets resulting from operations 9,800,261

Shareholder transactions:

Subscriptions (representing 695.439 shares) 1,320,000

Repurchases (representing 6,463.277 shares) (12,469,321)

Net increase (decrease) in net assets from shareholder transactions (11,149,321)

Total increase (decrease) in net assets (1,349,060)

Net assets, beginning of year (representing 93,550.912 shares) 175,773,808

Net assets, end of year (representing 87,783.074 shares) $ 174,424,748

For the year ended December 31, 2023

See accompanying notes and attached audited financial statements for Alternative Investment Partners Absolute Return Fund.

8

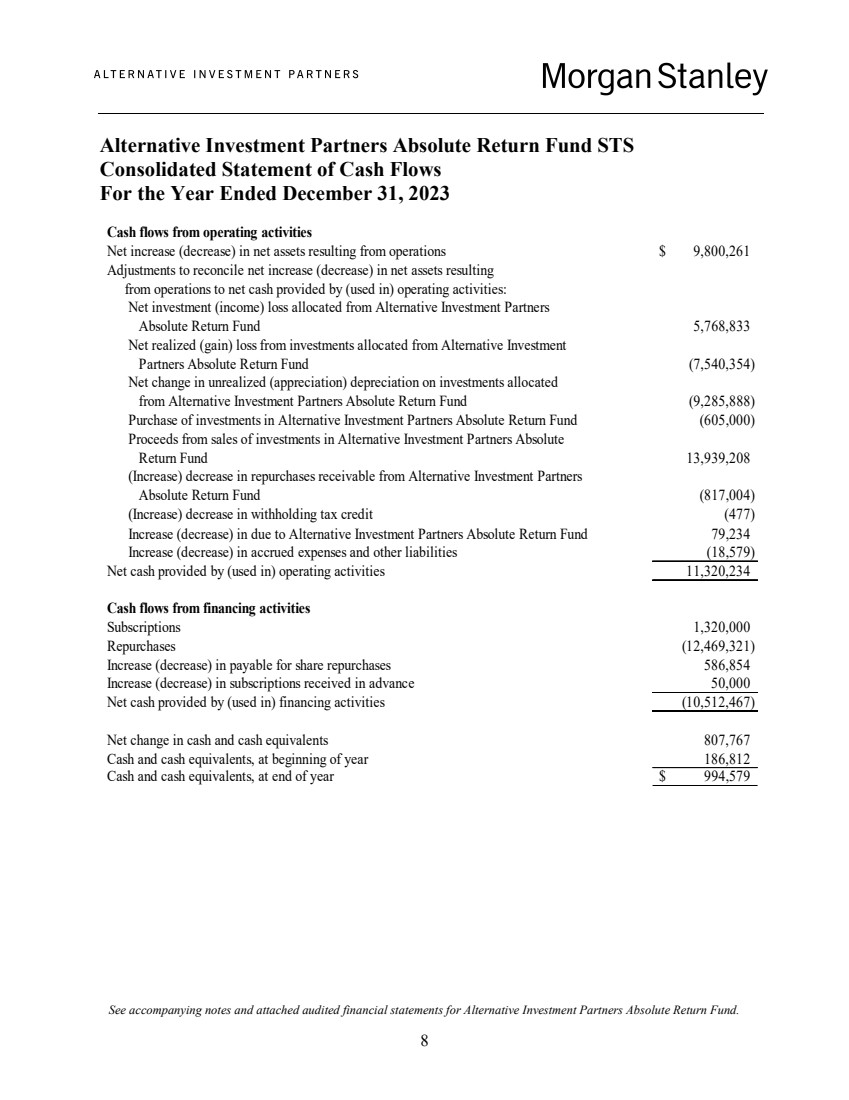

Alternative Investment Partners Absolute Return Fund STS

Consolidated Statement of Cash Flows

For the Year Ended December 31, 2023

Cash flows from operating activities

Net increase (decrease) in net assets resulting from operations 9,800,261 $

Adjustments to reconcile net increase (decrease) in net assets resulting

from operations to net cash provided by (used in) operating activities:

Net investment (income) loss allocated from Alternative Investment Partners

Absolute Return Fund 5,768,833 Net realized (gain) loss from investments allocated from Alternative Investment

Partners Absolute Return Fund (7,540,354) Net change in unrealized (appreciation) depreciation on investments allocated

from Alternative Investment Partners Absolute Return Fund (9,285,888)

Purchase of investments in Alternative Investment Partners Absolute Return Fund (605,000) Proceeds from sales of investments in Alternative Investment Partners Absolute

Return Fund 13,939,208 (Increase) decrease in repurchases receivable from Alternative Investment Partners

Absolute Return Fund (817,004) (Increase) decrease in withholding tax credit (477) Increase (decrease) in due to Alternative Investment Partners Absolute Return Fund 79,234 Increase (decrease) in accrued expenses and other liabilities (18,579) Net cash provided by (used in) operating activities 11,320,234 Cash flows from financing activities

Subscriptions 1,320,000 Repurchases (12,469,321) Increase (decrease) in payable for share repurchases 586,854 Increase (decrease) in subscriptions received in advance 50,000 Net cash provided by (used in) financing activities (10,512,467) Net change in cash and cash equivalents 807,767 Cash and cash equivalents, at beginning of year 186,812

Cash and cash equivalents, at end of year $ 994,579

Alternative Investment Partners Absolute Return Fund STS

Notes to Consolidated Financial Statements

December 31, 2023

See attached audited financial statements for Alternative Investment Partners Absolute Return Fund.

9

1. Organization and Consolidation

Alternative Investment Partners Absolute Return Fund STS (the “Fund”) was organized under the laws of

the State of Delaware as a statutory trust on October 31, 2005. The Fund commenced operations on

September 1, 2006 and operates pursuant to an Agreement and Declaration of Trust (the “Trust Deed”).

The Fund is registered under the U.S. Investment Company Act of 1940, as amended (the “1940 Act”), as

a closed-end, non-diversified management investment company. The Fund’s term is perpetual unless the

Fund is otherwise terminated under the terms of the Trust Deed or unless and until required by law.

The Fund is a “Feeder” fund in a “Master-Feeder” structure whereby the Fund invests substantially all of

its assets in AIP Absolute Return Fund LDC (the “Offshore Fund”), a Cayman Islands limited duration

company, which in turn invests substantially all of its assets in Alternative Investment Partners Absolute

Return Fund (the “Master Fund”). The Master Fund is a statutory trust organized under the laws of the

State of Delaware and is registered under the 1940 Act, as a closed-end, non-diversified, management

investment company. Morgan Stanley AIP GP LP serves as the Master Fund’s investment adviser (the

“Investment Adviser”). The Investment Adviser is an affiliate of Morgan Stanley and is registered as an

investment adviser under the U.S. Investment Advisers Act of 1940, as amended and as a commodity

trading adviser and a commodity pool operator with the Commodity Futures Trading Commission

(“CFTC”) and the National Futures Association (“NFA”). The Fund and the Offshore Fund have the same

investment objective as the Master Fund. The Master Fund’s investment objective is to seek capital

appreciation principally through investing in investment funds (“Investment Funds”) managed by third-party investment managers who employ a variety of “absolute return” investment strategies in pursuit of

attractive risk-adjusted returns consistent with the preservation of capital. “Absolute return” refers to a

broad class of investment strategies that are managed without reference to the performance of equity,

debt, and other markets. “Absolute return” investment strategies allow investment managers the flexibility

to use leveraged or short-sale positions to take advantage of perceived inefficiencies across the global

capital markets. The Master Fund may seek to gain investment exposure to certain Investment Funds or to

adjust market or risk exposure by entering into derivative transactions such as total return swaps, options,

and futures.

The Fund consolidates the Offshore Fund, a wholly-owned subsidiary, and has included all of the assets

and liabilities and revenues and expenses of the Offshore Fund in the accompanying financial statements.

Intercompany balances have been eliminated through consolidation. As of December 31, 2023, the Fund

had a 59.56% indirect ownership interest in the Master Fund. The financial statements of the Master

Fund, including the Schedule of Investments, are attached to this report and should be read in conjunction

with the Fund’s consolidated financial statements.

The Fund has a Board of Trustees (the “Board”) that has overall responsibility for monitoring and

overseeing the Fund’s investment program and its management and operations. A majority of the

members of the Board (the “Trustees”) are not “interested persons” (as defined by the 1940 Act) of the

Fund or the Investment Adviser. The same Trustees also serve as the Master Fund’s Board of Trustees.

Alternative Investment Partners Absolute Return Fund STS

Notes to Consolidated Financial Statements (continued)

See attached audited financial statements for Alternative Investment Partners Absolute Return Fund.

10

2. Significant Accounting Policies

The following significant accounting policies are in conformity with U.S. generally accepted accounting

principles (“US GAAP”). Such policies are consistently followed by the Fund in preparation of its

consolidated financial statements. Management has determined that the Fund is an investment company in

accordance with the Financial Accounting Standards Board (“FASB”) Accounting Standards Codification

(“ASC”) Topic 946, “Financial Services – Investment Companies”, for the purpose of financial reporting.

The preparation of financial statements in conformity with US GAAP requires management to make

estimates and assumptions that affect the reported amounts of assets and liabilities and disclosure of

contingent assets and liabilities at the date of the financial statements and the reported amounts of

increases or decreases in net assets from operations during the reporting period. Actual results could differ

from those estimates. The Fund’s financial statements are stated in United States dollars.

Investment in the Fund

The Fund offers on a continuous basis through Morgan Stanley Distribution, Inc. (the “Distributor”), an

affiliate of Morgan Stanley, 1,000,000 shares of beneficial interest (“Shares”). The initial closing date

(“Initial Closing Date”) for public offering of Shares was September 1, 2006. Shares were offered until

the Initial Closing Date at an initial offering price of $1,000 per Share, plus any applicable sales load, and

have been continuously offered thereafter for purchase as of the first day of each calendar month at the

Fund’s then current net asset value per Share, plus any applicable sales load. The Distributor may enter

into selected dealer agreements with various brokers and dealers (“Selling Agents”), some of which are

affiliates of the Fund, that have agreed to participate in the distribution of the Fund’s Shares. Shares may

also be purchased through any registered investment adviser (a “RIA”) that has entered into an

arrangement with the Distributor for such RIA to recommend Shares to its clients in conjunction with a

“wrap” fee, asset allocation or other managed asset program by such RIA.

Shares are sold only to certain special tax status investors (“Shareholders”), namely tax-exempt and tax-deferred investors. These investors also must represent that they are “accredited investors” within the

meaning of Rule 501(a) of Regulation D promulgated under the U.S. Securities Act of 1933, as amended.

The Distributor or any Selling Agent or RIA may impose additional eligibility requirements for investors

who purchase Shares through the Distributor or such Selling Agent or RIA. The minimum initial

investment in the Fund by any Shareholder is $50,000. The minimum additional investment in the Fund

by any Shareholder is $25,000. The minimum initial and additional investments may be reduced by the

Fund with respect to certain Shareholders. Shareholders may only purchase their Shares through the

Distributor, a Selling Agent or a RIA.

The Distributor and Selling Agents may charge Shareholders a sales load of up to 3% of the

Shareholder’s purchase. The Distributor or a Selling Agent may, in its discretion, waive the sales load for

certain investors. In addition, purchasers of Shares in conjunction with certain “wrap” fee, asset allocation

or other managed asset programs sponsored by an investment adviser, including an affiliate of the

Adviser, or Morgan Stanley and its affiliates (including the Adviser) and the directors, partners,

principals, officers and employees of Morgan Stanley and its affiliates may not be charged a sales load by

the Distributor or Selling Agent.

Alternative Investment Partners Absolute Return Fund STS

Notes to Consolidated Financial Statements (continued)

See attached audited financial statements for Alternative Investment Partners Absolute Return Fund.

11

2. Significant Accounting Policies (continued)

Investment in the Fund (continued)

The Fund may from time to time offer to repurchase Shares (or portions of them) at net asset value

pursuant to written tenders by Shareholders. Any offer to repurchase Shares by the Fund is only made to

Shareholders at the same times as, and in parallel with, each repurchase offer made by the Master Fund to

its investors, including, indirectly, the Fund. Each such repurchase offer made by the Master Fund will

generally apply to up to 15% of the net assets of the Master Fund. Repurchases are made at such times, in

such amounts and on such terms as may be determined by the Board, in its sole discretion. In determining

whether the Fund should offer to repurchase Shares (or portions of them) from Shareholders, the Board

will consider the recommendations of the Adviser as to the timing of such an offer, as well as a variety of

operational, business and economic factors. The Adviser expects that it will recommend to the Board that

the Fund offers to repurchase Shares (or portions of them) from Shareholders quarterly, on each March

31, June 30, September 30, and December 31. In general, the Fund will initially pay at least 90% of the

estimated value of the repurchased Shares to Shareholders as of the later of: (1) a period of within 30 days

after the value of the Shares to be repurchased is determined, or (2) if the Master Fund has requested

withdrawals of its capital from any Investment Funds in order to fund the repurchase of Shares, within ten

business days after the Master Fund has received at least 90% of the aggregate amount withdrawn by the

Master Fund from such Investment Funds. The remaining amount (the “Holdback Amount”) will be paid

promptly after completion of the annual audit of the Fund and preparation of the Fund’s audited

consolidated financial statements. As of December 31, 2023, the total of all Shareholders’ Holdback

Amounts was $211,805 which includes any Holdback Amount for repurchases as of December 31, 2023,

and is included in payable for share repurchases in the Consolidated Statement of Assets and Liabilities.

Investment in the Master Fund

The Fund records its investment in the Master Fund at fair value which is represented by the Fund’s

proportionate indirect interest in the net assets of the Master Fund as of December 31, 2023. Valuation of

Investment Funds and other investments held by the Master Fund, including the Master Fund’s disclosure

of investments under the three-tier hierarchy, is discussed in the notes to the Master Fund’s financial

statements. The Fund records its pro rata share of the Master Fund’s income, expenses, and realized and

unrealized gains and losses. The performance of the Fund is directly affected by the performance of the

Master Fund. The financial statements of the Master Fund, which are attached, are an integral part of

these consolidated financial statements. Please refer to the accounting policies disclosed in the financial

statements of the Master Fund for additional information regarding significant accounting policies that

affect the Fund.

Cash and Cash Equivalents

Cash and cash equivalents consist of cash held on deposit and short term highly liquid investments that

are readily convertible to known amounts of cash and have maturities of three months or less. As of

December 31, 2023, the Fund did not hold any cash equivalents.

Alternative Investment Partners Absolute Return Fund STS

Notes to Consolidated Financial Statements (continued)

See attached audited financial statements for Alternative Investment Partners Absolute Return Fund.

12

2. Significant Accounting Policies (continued)

Income Recognition and Expenses

The Fund recognizes income and expenses on an accrual basis. Income, expenses, and realized and

unrealized gains and losses are recorded monthly. The Fund accrues its own expenses. The Fund does not

pay the Adviser a management fee. As an indirect holder of shares in the Master Fund, however, the Fund

does bear its allocable portion (based on the net asset value of the Master Fund attributable to the Fund)

of the expenses of the Master Fund, including the management fee paid to the Investment Adviser and

shareholder servicing fees paid to the Distributor as described in the Master Fund’s financial statements.

Please refer to the attached financial statements of the Master Fund for a discussion of the computation of

the management fee and shareholder servicing fee. Included in expenses allocated from the Master Fund

in the Consolidated Statement of Operations is $1,755,742 and $1,305,341, which are the Fund’s

proportionate share of management fees and shareholder servicing fees, respectively, incurred by the

Master Fund for the year ended December 31, 2023.

Third-Party Service Providers

State Street Bank and Trust Company (“State Street”) provides accounting and administrative services to

the Fund. State Street also serves as the Fund’s custodian.

UMB Fund Services, Inc. serves as the Funds transfer agent. Transfer agent fees are payable monthly

based on an annual Fund base fee, annual per Shareholder account changes, and out-of-pocket expenses

incurred by the transfer agent on the Fund’s behalf.

Income and Withholding Taxes

The Fund expects to be treated as a partnership for U.S. federal income tax purposes. No provision for

federal, state, or local income taxes is required in the consolidated financial statements. In accordance

with the U.S. Internal Revenue Code of 1986, as amended, each of the Shareholders is to include its

respective share of the Fund’s realized profits or losses in its individual tax returns. The Fund files tax

returns with the U.S. Internal Revenue Service and various states.

The Master Fund is required to withhold up to 30% U.S. tax from U.S. source dividends and 21% (33%

for non-corporate, non-U.S. investors) U.S. tax from effectively connected income allocable to its non-U.S. investors and remit those amounts to the U.S. internal Revenue Service on behalf of the non-U.S.

investors. If the Master Fund incurs a withholding tax or other tax obligation with respect to the share of

the Master Fund’s income allocable to any Shareholder, then the Master Fund, without limitation of any

other rights of the Fund, will cause a Share repurchase from the Master Fund in the amount of the tax

obligation. The amount of the tax obligation attributable to the Fund will be treated as an expense by the

Fund.

For the year ended December 31, 2023, the Master Fund recorded an estimated tax withholding amount of

$873,644 related to the Fund’s share of withholding taxes, which is included in the Fund’s Consolidated

Statement of Operations.

Alternative Investment Partners Absolute Return Fund STS

Notes to Consolidated Financial Statements (continued)

See attached audited financial statements for Alternative Investment Partners Absolute Return Fund.

13

2. Significant Accounting Policies (continued)

Income and Withholding Taxes (continued)

The Fund has concluded there are no significant uncertain tax positions that would require recognition in

the consolidated financial statements as of December 31, 2023. If applicable, the Fund recognizes interest

accrued related to unrecognized tax benefits in interest expense and penalties in other expenses in the

Consolidated Statement of Operations. Generally, open tax years under potential examination vary by

jurisdiction, but at least each of the tax years in the four-year period ended December 31, 2023, remains

subject to examination by major taxing authorities.

3. Market Risk

The value of an investment in the Fund is based on the values of the Fund’s investments, which change

due to economic and other events that affect markets generally, as well as those that affect particular

regions, countries, industries, companies or governments. The risks associated with these developments

may be magnified if certain social, political, economic and other conditions and events adversely interrupt

the global economy and financial markets. Securities in the Fund’s portfolio may underperform due to

inflation (or expectations for inflation), interest rates, global demand for particular products or resources,

natural disasters and extreme weather events, health emergencies (such as epidemics and pandemics),

terrorism, regulatory events and governmental or quasi-governmental actions. The occurrence of global

events similar to those in recent years, such as terrorist attacks around the world, natural disasters, health

emergencies, social and political (including geopolitical) discord and tensions or debt crises and

downgrades, among others, may result in market volatility and may have long term effects on both the

U.S. and global financial markets. It is difficult to predict when events affecting the U.S. or global

financial markets may occur, the effects that such events may have and the duration of those effects

(which may last for extended periods). These events may negatively impact broad segments of businesses

and populations and have a significant and rapid negative impact on the performance of the Fund’s

investments, and exacerbate pre-existing risks to the Fund. The occurrence, duration and extent of these

or other types of adverse economic and market conditions and uncertainty over the long term cannot be

reasonably projected or estimated at this time. The ultimate impact of public health emergencies or other

adverse economic or market developments and the extent to which the associated conditions impact the

Fund and its investments will also depend on other future developments, which are highly uncertain,

difficult to accurately predict and subject to change at any time. The financial performance of the Fund’s

investments (and, in turn, the Fund’s investment results) as well as their liquidity may be adversely

affected because of these and similar types of factors and developments, which may in turn impact

valuation, the Fund’s ability to sell securities and/or its ability to meet redemptions.

4. Contractual Obligations

The Fund enters into contracts that contain a variety of indemnifications. The Fund’s maximum exposure

under these arrangements is unknown. However, the Fund has not had prior claims or losses pursuant to

these contracts and expects the risk of loss to be remote.

Alternative Investment Partners Absolute Return Fund STS

Notes to Consolidated Financial Statements (continued)

See attached audited financial statements for Alternative Investment Partners Absolute Return Fund.

14

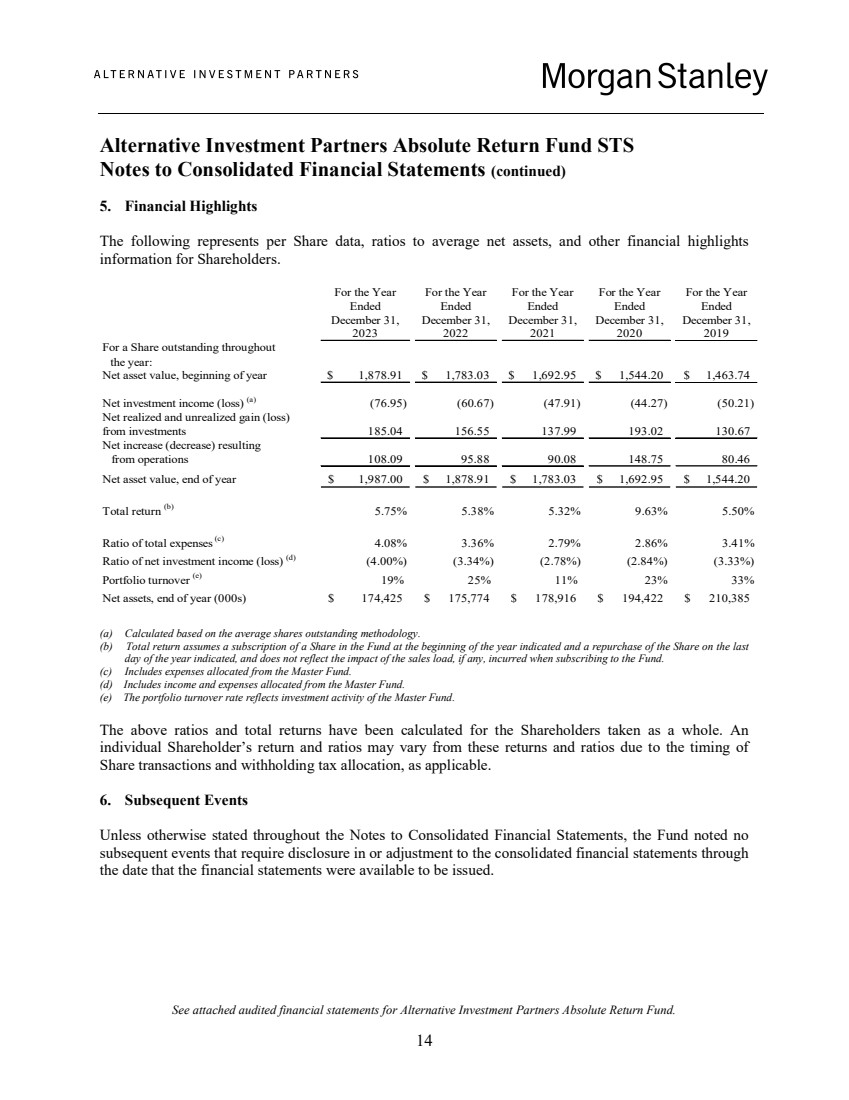

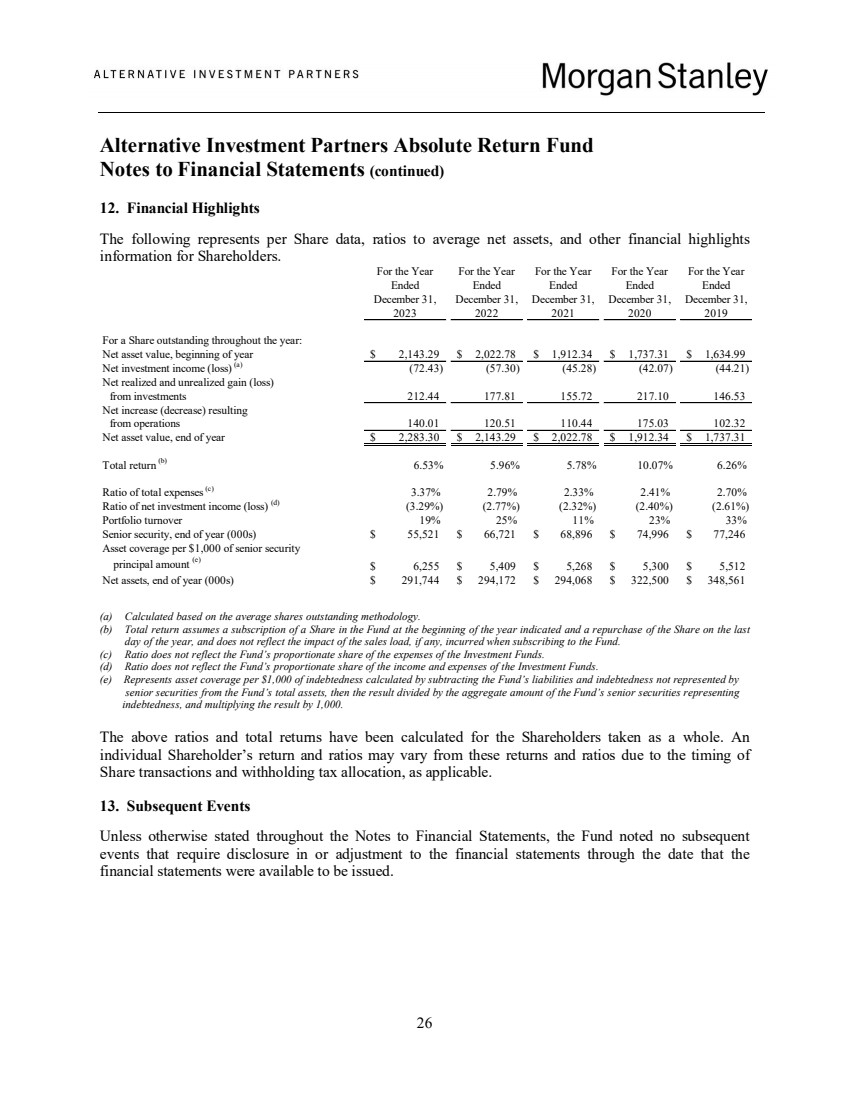

5. Financial Highlights

The following represents per Share data, ratios to average net assets, and other financial highlights

information for Shareholders.

For the Year For the Year For the Year For the Year For the Year

Ended Ended Ended Ended Ended

December 31, December 31, December 31, December 31, December 31,

2023 2022 2021 2020 2019

For a Share outstanding throughout

the year:

Net asset value, beginning of year 1,878.91 $ 1,783.03 $ 1,692.95 $ 1,544.20 $ 1,463.74 $

Net investment income (loss) (a) (76.95) (60.67) (47.91) (44.27) (50.21)

Net realized and unrealized gain (loss)

from investments 185.04 156.55 137.99 193.02 130.67 Net increase (decrease) resulting

from operations 108.09 95.88 90.08 148.75 80.46 Net asset value, end of year 1,987.00 $ 1,878.91 $ 1,783.03 $ 1,692.95 $ 1,544.20 $

Total return (b) 5.75% 5.38% 5.32% 9.63% 5.50%

Ratio of total expenses (c) 4.08% 3.36% 2.79% 2.86% 3.41%

Ratio of net investment income (loss) (d) (4.00%) (3.34%) (2.78%) (2.84%) (3.33%)

Portfolio turnover (e) 19% 25% 11% 23% 33%

Net assets, end of year (000s) 174,425 $ 175,774 $ 178,916 $ 194,422 $ 210,385 $

(a) Calculated based on the average shares outstanding methodology.

(b) Total return assumes a subscription of a Share in the Fund at the beginning of the year indicated and a repurchase of the Share on the last

day of the year indicated, and does not reflect the impact of the sales load, if any, incurred when subscribing to the Fund.

(c) Includes expenses allocated from the Master Fund.

(d) Includes income and expenses allocated from the Master Fund.

(e) The portfolio turnover rate reflects investment activity of the Master Fund.

The above ratios and total returns have been calculated for the Shareholders taken as a whole. An

individual Shareholder’s return and ratios may vary from these returns and ratios due to the timing of

Share transactions and withholding tax allocation, as applicable.

6. Subsequent Events

Unless otherwise stated throughout the Notes to Consolidated Financial Statements, the Fund noted no

subsequent events that require disclosure in or adjustment to the consolidated financial statements through

the date that the financial statements were available to be issued.

15

Alternative Investment Partners Absolute Return Fund STS

Proxy Voting Policies and Procedures and Proxy Voting Record (Unaudited)

If applicable, a copy of (1) the Fund’s policies and procedures with respect to the voting of proxies

relating to the Fund’s investments; and (2) how the Fund voted proxies relating to Fund investments

during the most recent year ended December 31, is available without charge, upon request, by calling the

Fund at 1-888-322-4675. This information is also available on the Securities and Exchange Commission’s

website at http://www.sec.gov.

Quarterly Portfolio Schedule (Unaudited)

The Fund also files a complete schedule of portfolio holdings with the Securities and Exchange

Commission for the Fund’s first and third fiscal quarters on Form N-PORT. The Fund’s Forms N-PORT

are available on the Securities and Exchange Commission’s website at http://www.sec.gov. and Morgan

Stanley’s public website, www.morganstanley.com/im/shareholderreports. Once filed, the most recent

Form N-PORT will be available without charge, upon request, by calling the Fund at

1-888-322-4675.

16

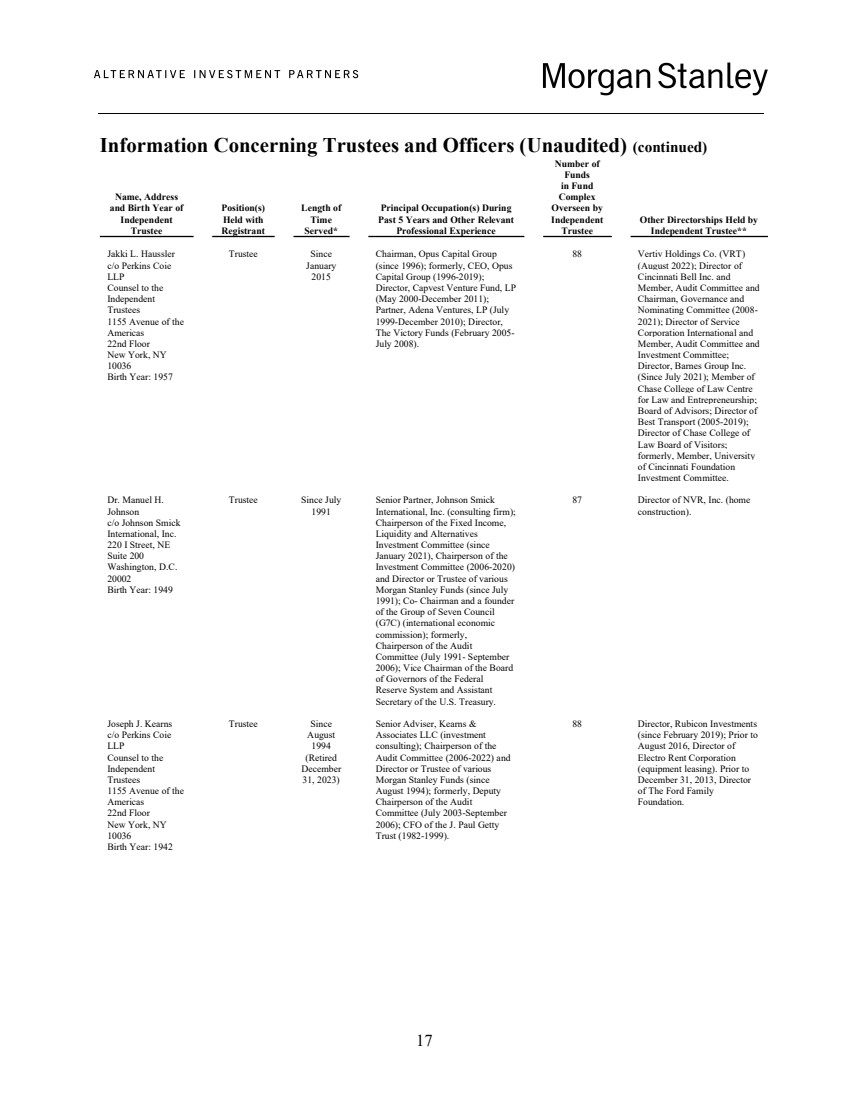

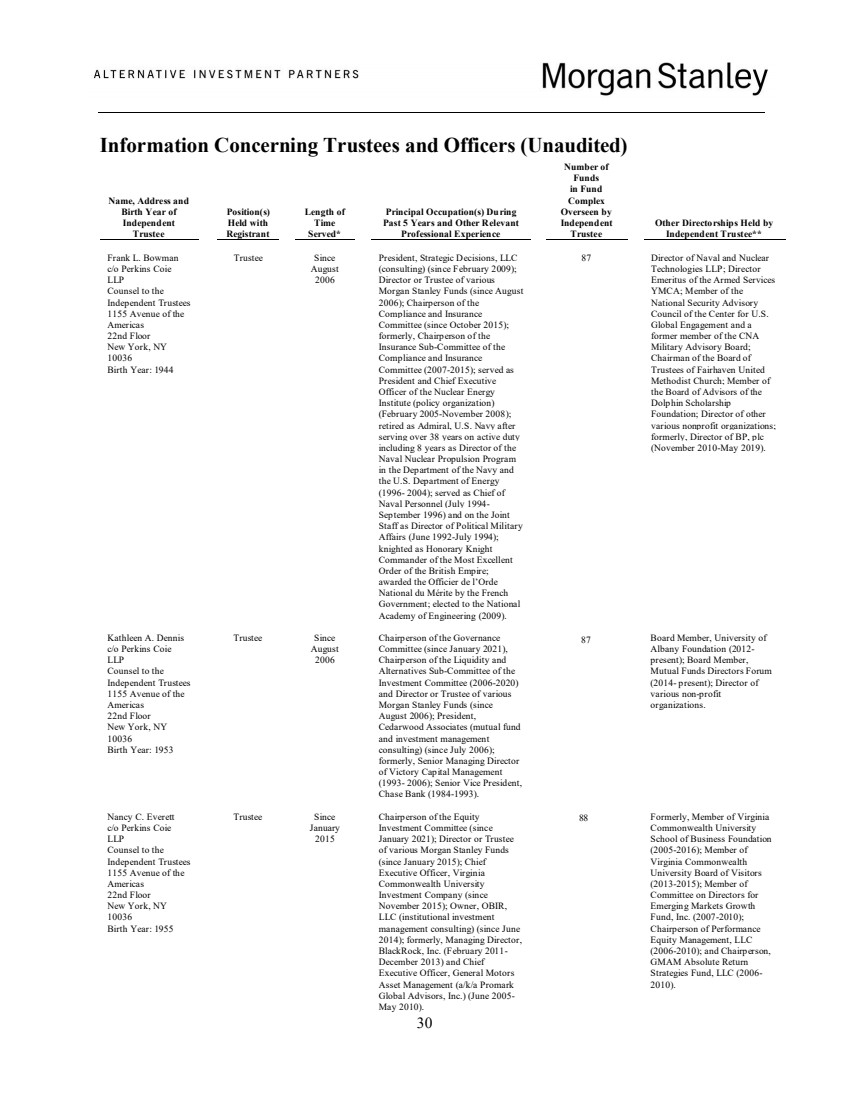

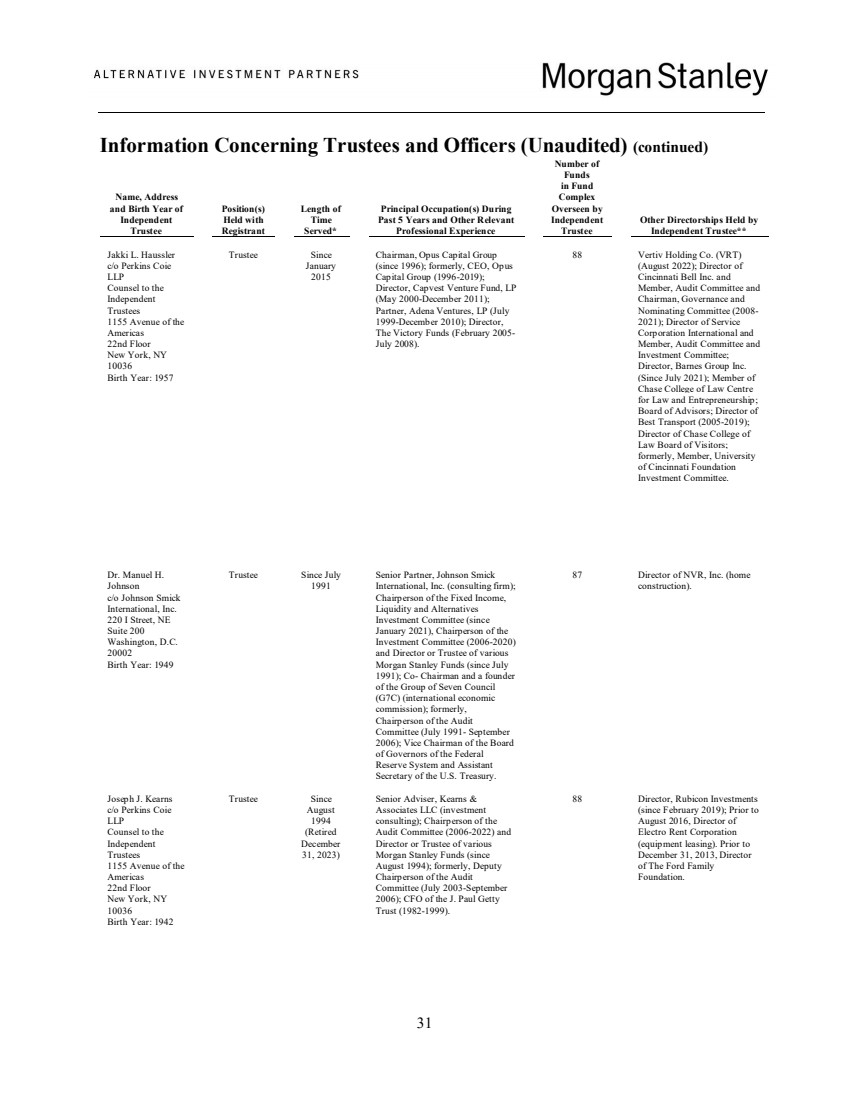

Information Concerning Trustees and Officers (Unaudited)

Name, Address and

Birth Year of

Independent

Trustee

Position(s)

Held with

Registrant

Length of

Time

Served*

Principal Occupation(s) During

Past 5 Years and Other Relevant

Professional Experience

Number of

Funds

in Fund

Complex

Overseen by

Independent

Trustee

Other Directorships Held

by Independent Trustee**

Frank L. Bowman

c/o Perkins Coie

LLP

Counsel to the

Independent Trustees

1155 Avenue of the

Americas

22nd Floor

New York, NY

10036

Birth Year: 1944

Trustee Since

August

2006

President, Strategic Decisions, LLC

(consulting) (since February 2009);

Director or Trustee of various

Morgan Stanley Funds (since

August 2006); Chairperson of the

Compliance and Insurance

Committee (since October 2015);

formerly, Chairperson of the

Insurance Sub-Committee of the

Compliance and Insurance

Committee (2007-2015); served as

President and Chief Executive

Officer of the Nuclear Energy

Institute (policy organization)

(February 2005-November 2008);

retired as Admiral, U.S. Navy after

serving over 38 years on active duty

including 8 years as Director of the

Naval Nuclear Propulsion Program

in the Department of the Navy and

the U.S. Department of Energy

(1996- 2004); served as Chief of

Naval Personnel (July 1994-

September 1996) and on the Joint

Staff as Director of Political Military

Affairs (June 1992-July 1994);

knighted as Honorary Knight

Commander of the Most Excellent

Order of the British Empire;

awarded the Officier de l’Orde

National du Mérite by the French

Government; elected to the National

Academy of Engineering (2009).

87 Director of Naval and

Nuclear Technologies LLP;

Director Emeritus of the

Armed Services YMCA;

Member of the National

Security Advisory Council

of the Center for U.S.

Global Engagement and a

former member of the CNA

Military Advisory Board;

Chairman of the Board of

Trustees of Fairhaven

United Methodist Church;

Member of the Board of

Advisors of the Dolphin

Scholarship Foundation;

Director of other various

nonprofit organizations;

formerly, Director of BP,

plc (November 2010-May

2019).

Kathleen A. Dennis

c/o Perkins Coie

LLP

Counsel to the

Independent Trustees

1155 Avenue of the

Americas

22nd Floor

New York, NY

10036

Birth Year: 1953

Trustee Since

August

2006

Chairperson of the Governance

Committee (since January 2021),

Chairperson of the Liquidity and

Alternatives Sub-Committee of the

Investment Committee (2006-2020)

and Director or Trustee of various

Morgan Stanley Funds (since

August 2006); President,

Cedarwood Associates (mutual fund

and investment management

consulting) (since July 2006);

formerly, Senior Managing Director

of Victory Capital Management

(1993-2006).; Senior Vice President,

Chase Bank (1984-1993).

87 Board Member, University

of Albany Foundation

(2012- present); Board

Member, Mutual Funds

Directors Forum (2014-

present); Director of various

non-profit organizations.

Nancy C. Everett

c/o Perkins Coie

LLP

Counsel to the

Independent Trustees

1155 Avenue of the

Americas

22nd Floor

New York, NY

10036

Birth Year: 1955

Trustee

Since

January

2015

Chairperson of the Equity Investment

Committee (since January 2021);

Director or Trustee of various Morgan

Stanley Funds (since January 2015);

Chief Executive Officer, Virginia

Commonwealth University Investment

Company (since November 2015);

Owner, OBIR, LLC (institutional

investment management consulting)

(since June 2014); formerly, Managing

Director, BlackRock, Inc. (February

2011-December 2013) and Chief

Executive Officer, General Motors

Asset Management (a/k/a Promark

Global Advisors, Inc.) (June 2005-

May 2010).

88

Formerly, Member of

Virginia Commonwealth

University School of

Business Foundation (2005-

2016); Member of Virginia

Commonwealth University

Board of Visitors (2013-

2015); Member of

Committee on Directors for

Emerging Markets Growth

Fund, Inc. (2007-2010);

Chairperson of Performance

Equity Management, LLC

(2006-2010); and

Chairperson, GMAM

Absolute Return Strategies

Fund, LLC (2006-2010).

17

Information Concerning Trustees and Officers (Unaudited) (continued)

Name, Address

and Birth Year of

Independent

Trustee

Position(s)

Held with

Registrant

Length of

Time

Served*

Principal Occupation(s) During

Past 5 Years and Other Relevant

Professional Experience

Number of

Funds

in Fund

Complex

Overseen by

Independent

Trustee

Other Directorships Held by

Independent Trustee**

Jakki L. Haussler

c/o Perkins Coie

LLP

Counsel to the

Independent

Trustees

1155 Avenue of the

Americas

22nd Floor

New York, NY

10036

Birth Year: 1957

Trustee

Since

January

2015

Chairman, Opus Capital Group

(since 1996); formerly, CEO, Opus

Capital Group (1996-2019);

Director, Capvest Venture Fund, LP

(May 2000-December 2011);

Partner, Adena Ventures, LP (July

1999-December 2010); Director,

The Victory Funds (February 2005-

July 2008).

88 Vertiv Holdings Co. (VRT)

(August 2022); Director of

Cincinnati Bell Inc. and

Member, Audit Committee and

Chairman, Governance and

Nominating Committee (2008-

2021); Director of Service

Corporation International and

Member, Audit Committee and

Investment Committee;

Director, Barnes Group Inc.

(Since July 2021); Member of

Chase College of Law Centre

for Law and Entrepreneurship;

Board of Advisors; Director of

Best Transport (2005-2019);

Director of Chase College of

Law Board of Visitors;

formerly, Member, University

of Cincinnati Foundation

Investment Committee.

Dr. Manuel H.

Johnson

c/o Johnson Smick

International, Inc.

220 I Street, NE

Suite 200

Washington, D.C.

20002

Birth Year: 1949

Trustee Since July

1991

Senior Partner, Johnson Smick

International, Inc. (consulting firm);

Chairperson of the Fixed Income,

Liquidity and Alternatives

Investment Committee (since

January 2021), Chairperson of the

Investment Committee (2006-2020)

and Director or Trustee of various

Morgan Stanley Funds (since July

1991); Co- Chairman and a founder

of the Group of Seven Council

(G7C) (international economic

commission); formerly,

Chairperson of the Audit

Committee (July 1991- September

2006); Vice Chairman of the Board

of Governors of the Federal

Reserve System and Assistant

Secretary of the U.S. Treasury.

87 Director of NVR, Inc. (home

construction).

Joseph J. Kearns

c/o Perkins Coie

LLP

Counsel to the

Independent

Trustees

1155 Avenue of the

Americas

22nd Floor

New York, NY

10036

Birth Year: 1942

Trustee Since

August

1994

(Retired

December

31, 2023)

Senior Adviser, Kearns &

Associates LLC (investment

consulting); Chairperson of the

Audit Committee (2006-2022) and

Director or Trustee of various

Morgan Stanley Funds (since

August 1994); formerly, Deputy

Chairperson of the Audit

Committee (July 2003-September

2006); CFO of the J. Paul Getty

Trust (1982-1999).

88 Director, Rubicon Investments

(since February 2019); Prior to

August 2016, Director of

Electro Rent Corporation

(equipment leasing). Prior to

December 31, 2013, Director

of The Ford Family

Foundation.

18

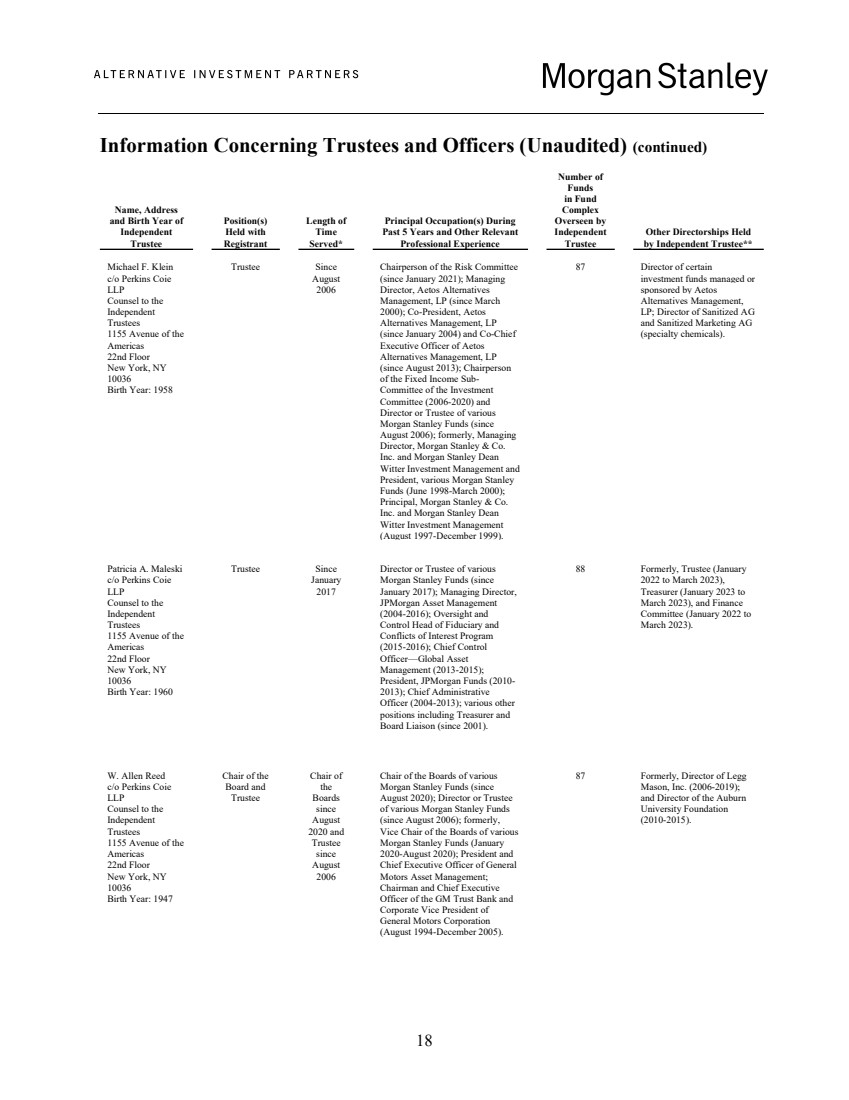

Information Concerning Trustees and Officers (Unaudited) (continued)

Name, Address

and Birth Year of

Independent

Trustee

Position(s)

Held with

Registrant

Length of

Time

Served*

Principal Occupation(s) During

Past 5 Years and Other Relevant

Professional Experience

Number of

Funds

in Fund

Complex

Overseen by

Independent

Trustee

Other Directorships Held

by Independent Trustee**

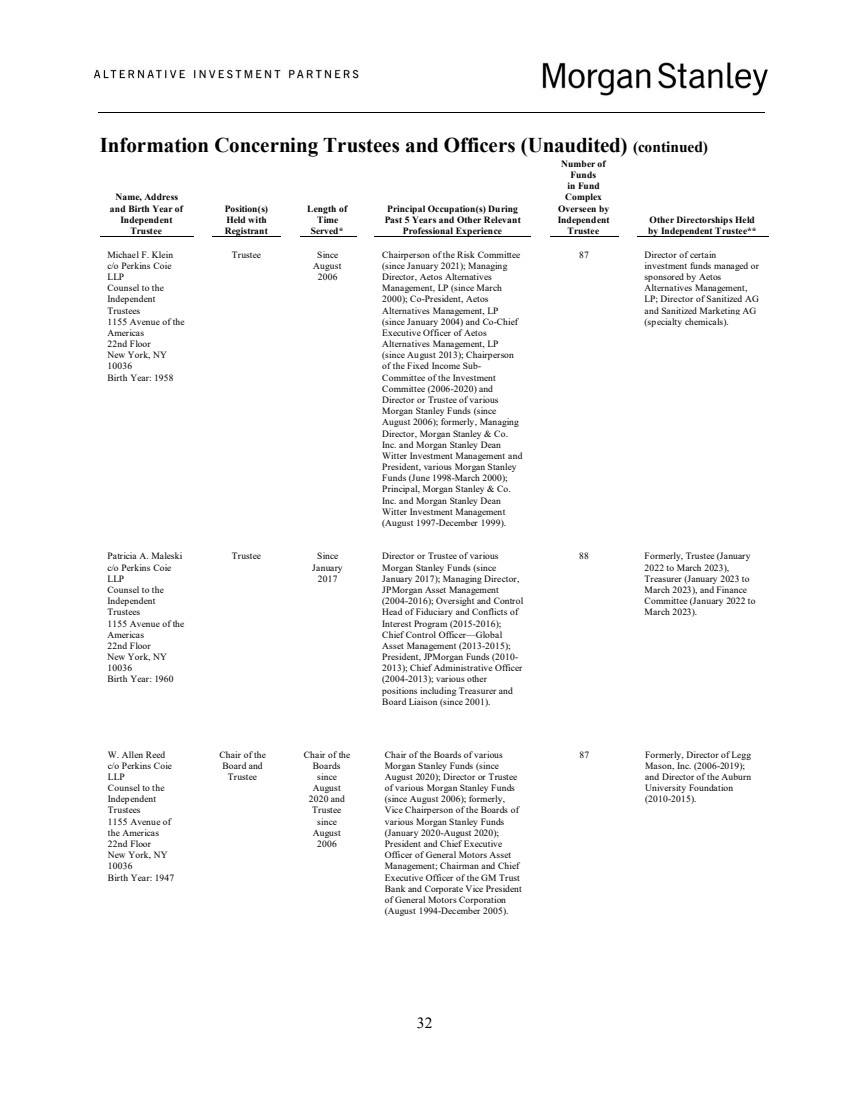

Michael F. Klein

c/o Perkins Coie

LLP

Counsel to the

Independent

Trustees

1155 Avenue of the

Americas

22nd Floor

New York, NY

10036

Birth Year: 1958

Trustee

Since

August

2006

Chairperson of the Risk Committee

(since January 2021); Managing

Director, Aetos Alternatives

Management, LP (since March

2000); Co-President, Aetos

Alternatives Management, LP

(since January 2004) and Co-Chief

Executive Officer of Aetos

Alternatives Management, LP

(since August 2013); Chairperson

of the Fixed Income Sub-Committee of the Investment

Committee (2006-2020) and

Director or Trustee of various

Morgan Stanley Funds (since

August 2006); formerly, Managing

Director, Morgan Stanley & Co.

Inc. and Morgan Stanley Dean

Witter Investment Management and

President, various Morgan Stanley

Funds (June 1998-March 2000);

Principal, Morgan Stanley & Co.

Inc. and Morgan Stanley Dean

Witter Investment Management

(August 1997-December 1999).

87 Director of certain

investment funds managed or

sponsored by Aetos

Alternatives Management,

LP; Director of Sanitized AG

and Sanitized Marketing AG

(specialty chemicals).

Patricia A. Maleski

c/o Perkins Coie

LLP

Counsel to the

Independent

Trustees

1155 Avenue of the

Americas

22nd Floor

New York, NY

10036

Birth Year: 1960

Trustee

Since

January

2017

Director or Trustee of various

Morgan Stanley Funds (since

January 2017); Managing Director,

JPMorgan Asset Management

(2004-2016); Oversight and

Control Head of Fiduciary and

Conflicts of Interest Program

(2015-2016); Chief Control

Officer—Global Asset

Management (2013-2015);

President, JPMorgan Funds (2010-

2013); Chief Administrative

Officer (2004-2013); various other

positions including Treasurer and

Board Liaison (since 2001).

88

Formerly, Trustee (January

2022 to March 2023),

Treasurer (January 2023 to

March 2023), and Finance

Committee (January 2022 to

March 2023).

W. Allen Reed

c/o Perkins Coie

LLP

Counsel to the

Independent

Trustees

1155 Avenue of the

Americas

22nd Floor

New York, NY

10036

Birth Year: 1947

Chair of the

Board and

Trustee

Chair of

the

Boards

since

August

2020 and

Trustee

since

August

2006

Chair of the Boards of various

Morgan Stanley Funds (since

August 2020); Director or Trustee

of various Morgan Stanley Funds

(since August 2006); formerly,

Vice Chair of the Boards of various

Morgan Stanley Funds (January

2020-August 2020); President and

Chief Executive Officer of General

Motors Asset Management;

Chairman and Chief Executive

Officer of the GM Trust Bank and

Corporate Vice President of

General Motors Corporation

(August 1994-December 2005).

87

Formerly, Director of Legg

Mason, Inc. (2006-2019);

and Director of the Auburn

University Foundation

(2010-2015).

19

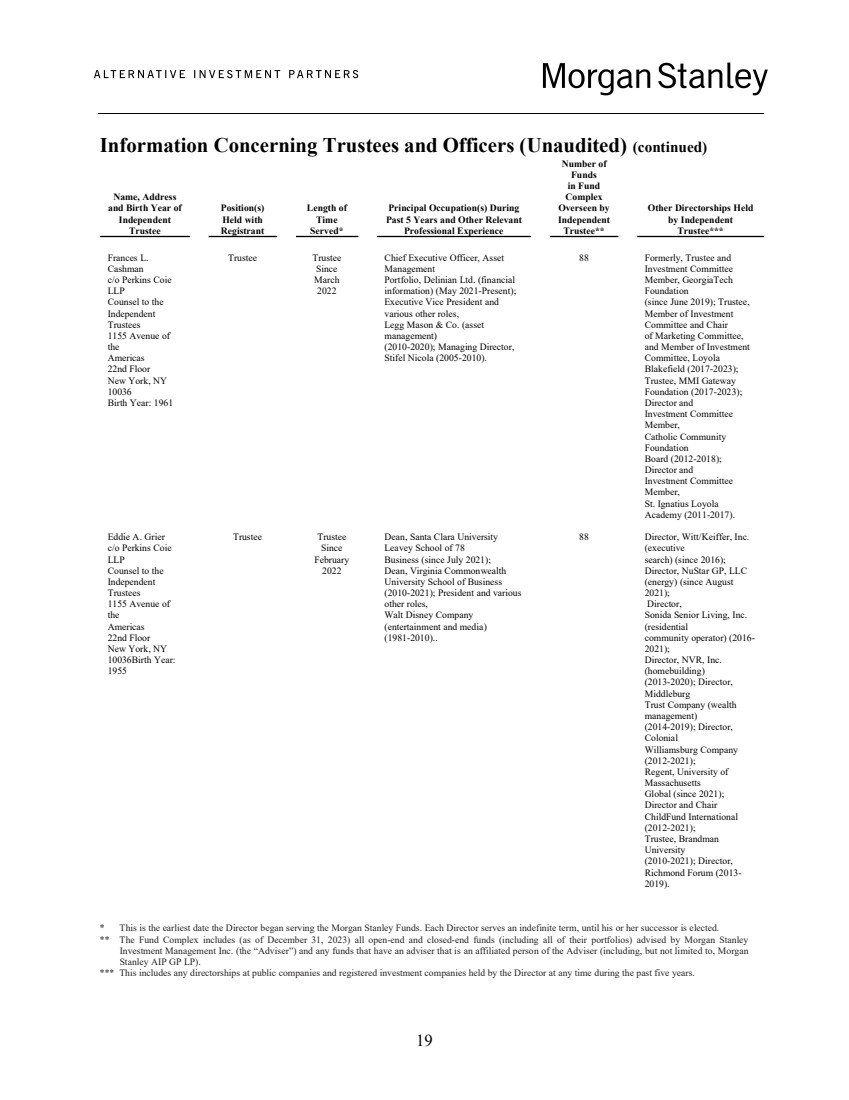

Information Concerning Trustees and Officers (Unaudited) (continued)

Name, Address

and Birth Year of

Independent

Trustee

Position(s)

Held with

Registrant

Length of

Time

Served*

Principal Occupation(s) During

Past 5 Years and Other Relevant

Professional Experience

Number of

Funds

in Fund

Complex

Overseen by

Independent

Trustee**

Other Directorships Held

by Independent

Trustee***

Frances L.

Cashman

c/o Perkins Coie

LLP

Counsel to the

Independent

Trustees

1155 Avenue of

the

Americas

22nd Floor

New York, NY

10036

Birth Year: 1961

Trustee Trustee

Since

March

2022

Chief Executive Officer, Asset

Management

Portfolio, Delinian Ltd. (financial

information) (May 2021-Present);

Executive Vice President and

various other roles,

Legg Mason & Co. (asset

management)

(2010-2020); Managing Director,

Stifel Nicola (2005-2010).

88 Formerly, Trustee and

Investment Committee

Member, GeorgiaTech

Foundation

(since June 2019); Trustee,

Member of Investment

Committee and Chair

of Marketing Committee,

and Member of Investment

Committee, Loyola

Blakefield (2017-2023);

Trustee, MMI Gateway

Foundation (2017-2023);

Director and

Investment Committee

Member,

Catholic Community

Foundation

Board (2012-2018);

Director and

Investment Committee

Member,

St. Ignatius Loyola

Academy (2011-2017).

Eddie A. Grier

c/o Perkins Coie

LLP

Counsel to the

Independent

Trustees

1155 Avenue of

the

Americas

22nd Floor

New York, NY

10036Birth Year:

1955

Trustee Trustee

Since

February

2022

Dean, Santa Clara University

Leavey School of 78

Business (since July 2021);

Dean, Virginia Commonwealth

University School of Business

(2010-2021); President and various

other roles,

Walt Disney Company

(entertainment and media)

(1981-2010)..

88 Director, Witt/Keiffer, Inc.

(executive

search) (since 2016);

Director, NuStar GP, LLC

(energy) (since August

2021);

Director,

Sonida Senior Living, Inc.

(residential

community operator) (2016-

2021);

Director, NVR, Inc.

(homebuilding)

(2013-2020); Director,

Middleburg

Trust Company (wealth

management)

(2014-2019); Director,

Colonial

Williamsburg Company

(2012-2021);

Regent, University of

Massachusetts

Global (since 2021);

Director and Chair

ChildFund International

(2012-2021);

Trustee, Brandman

University

(2010-2021); Director,

Richmond Forum (2013-

2019).

* This is the earliest date the Director began serving the Morgan Stanley Funds. Each Director serves an indefinite term, until his or her successor is elected.

** The Fund Complex includes (as of December 31, 2023) all open-end and closed-end funds (including all of their portfolios) advised by Morgan Stanley

Investment Management Inc. (the “Adviser”) and any funds that have an adviser that is an affiliated person of the Adviser (including, but not limited to, Morgan

Stanley AIP GP LP).

*** This includes any directorships at public companies and registered investment companies held by the Director at any time during the past five years.

20

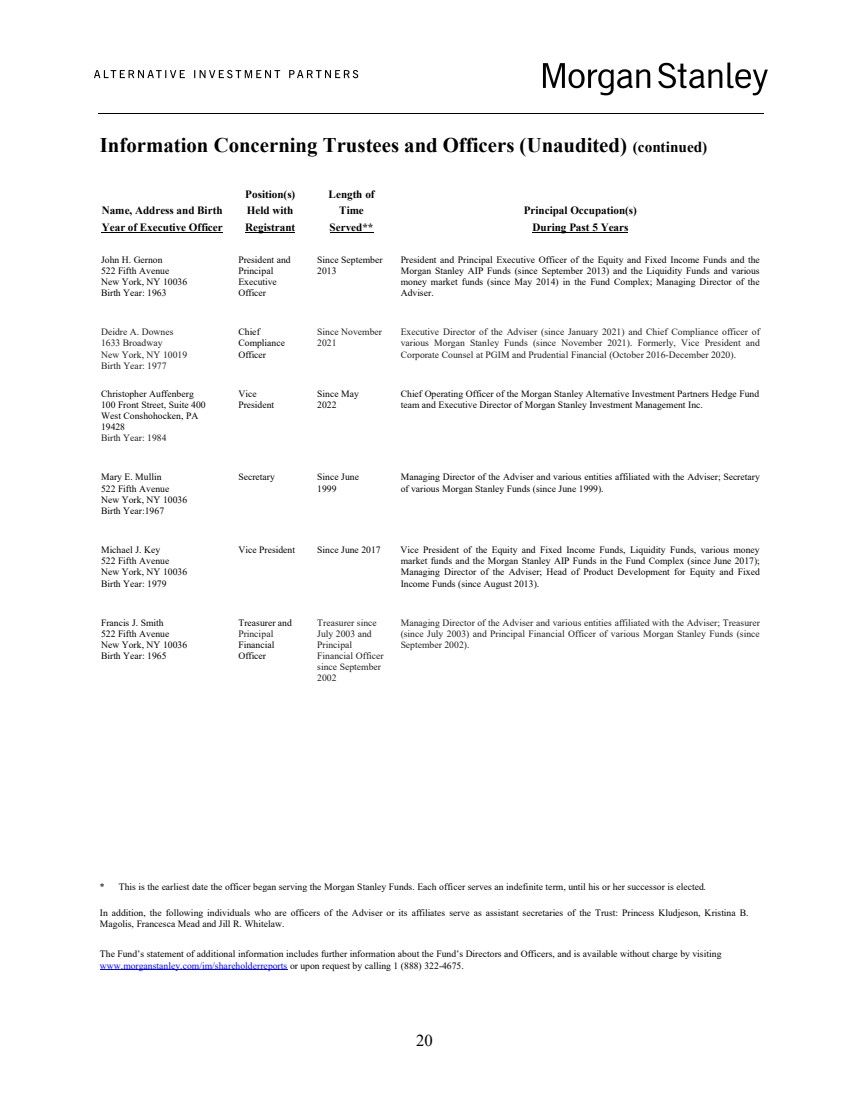

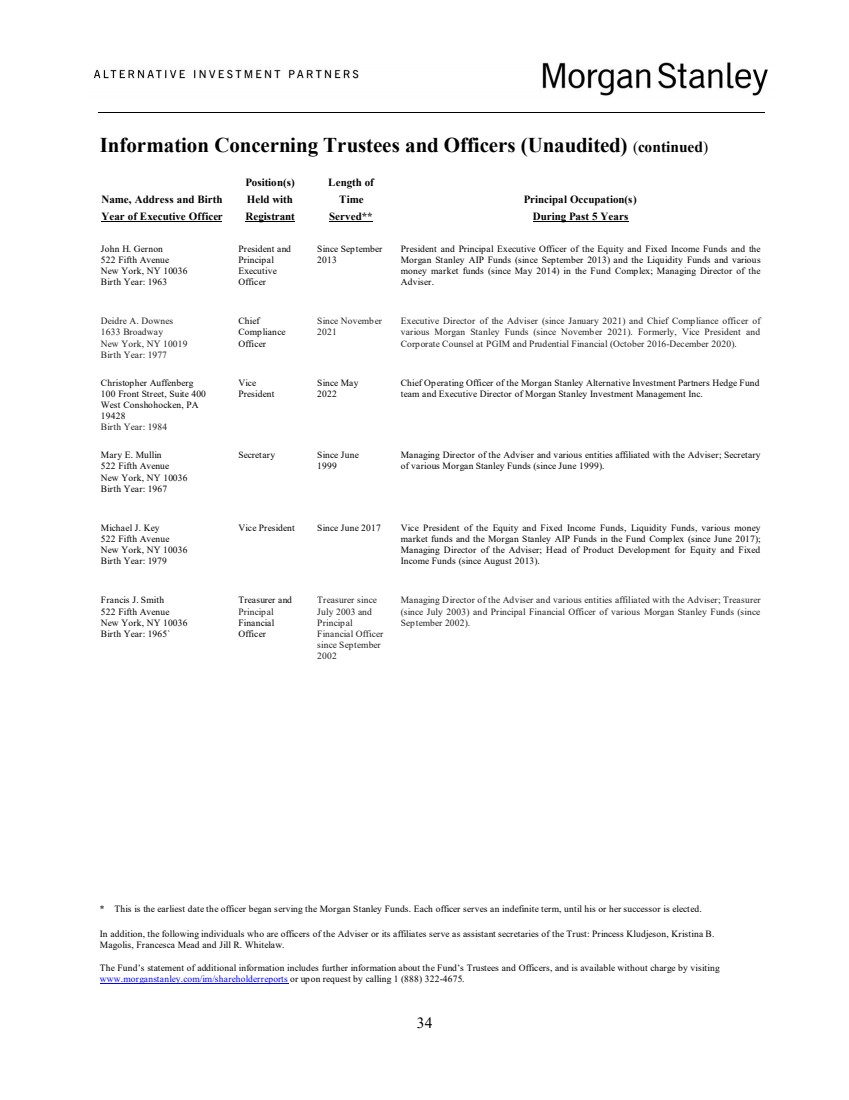

Information Concerning Trustees and Officers (Unaudited) (continued)

Position(s) Length of

Name, Address and Birth Held with Time Principal Occupation(s)

Year of Executive Officer Registrant Served** During Past 5 Years

John H. Gernon

522 Fifth Avenue

New York, NY 10036

Birth Year: 1963

President and

Principal

Executive

Officer

Since September

2013

President and Principal Executive Officer of the Equity and Fixed Income Funds and the

Morgan Stanley AIP Funds (since September 2013) and the Liquidity Funds and various

money market funds (since May 2014) in the Fund Complex; Managing Director of the

Adviser.

Deidre A. Downes

1633 Broadway

New York, NY 10019

Birth Year: 1977

Chief

Compliance

Officer

Since November

2021

Executive Director of the Adviser (since January 2021) and Chief Compliance officer of

various Morgan Stanley Funds (since November 2021). Formerly, Vice President and

Corporate Counsel at PGIM and Prudential Financial (October 2016-December 2020).

Christopher Auffenberg

100 Front Street, Suite 400

West Conshohocken, PA

19428

Birth Year: 1984

Vice

President

Since May

2022

Chief Operating Officer of the Morgan Stanley Alternative Investment Partners Hedge Fund

team and Executive Director of Morgan Stanley Investment Management Inc.

Mary E. Mullin

522 Fifth Avenue

New York, NY 10036

Birth Year:1967

Secretary Since June

1999

Managing Director of the Adviser and various entities affiliated with the Adviser; Secretary

of various Morgan Stanley Funds (since June 1999).

Michael J. Key

522 Fifth Avenue

New York, NY 10036

Birth Year: 1979

Vice President Since June 2017 Vice President of the Equity and Fixed Income Funds, Liquidity Funds, various money

market funds and the Morgan Stanley AIP Funds in the Fund Complex (since June 2017);

Managing Director of the Adviser; Head of Product Development for Equity and Fixed

Income Funds (since August 2013).

Francis J. Smith

522 Fifth Avenue

New York, NY 10036

Birth Year: 1965

Treasurer and

Principal

Financial

Officer

Treasurer since

July 2003 and

Principal

Financial Officer

since September

2002

Managing Director of the Adviser and various entities affiliated with the Adviser; Treasurer

(since July 2003) and Principal Financial Officer of various Morgan Stanley Funds (since

September 2002).

* This is the earliest date the officer began serving the Morgan Stanley Funds. Each officer serves an indefinite term, until his or her successor is elected.

In addition, the following individuals who are officers of the Adviser or its affiliates serve as assistant secretaries of the Trust: Princess Kludjeson, Kristina B.

Magolis, Francesca Mead and Jill R. Whitelaw.

The Fund’s statement of additional information includes further information about the Fund’s Directors and Officers, and is available without charge by visiting

www.morganstanley.com/im/shareholderreports or upon request by calling 1 (888) 322-4675.

21

Alternative Investment Partners Absolute Return Fund STS

100 Front Street, Suite 400

West Conshohocken, PA 19428

Trustees

W. Allen Reed, Chair of the Board and Trustee

Frank L. Bowman

Frances L. Cashman

Kathleen A. Dennis

Nancy C. Everett

Eddie A. Grier

Jakki L. Haussler

Dr. Manuel H. Johnson

Joseph J. Kearns

Michael F. Klein

Patricia Maleski

Officers

John H. Gernon, President and Principal Executive Officer

Christopher Auffenberg, Vice President

Michael J. Key, Vice President

Deidre A. Downes, Chief Compliance Officer

Francis J.Smith, Treasurer and Principal Financial Officer

Mary E. Mullin, Secretary

Investment Adviser

Morgan Stanley AIP GP LP

100 Front Street, Suite 400

West Conshohocken, PA 19428

Administrator, Custodian, Fund Accounting Agent and Escrow Agent

State Street Bank and Trust Company

One Lincoln Street

Boston, MA 02111

Transfer Agent

UMB Fund Services, Inc.

803 W. Michigan Street

Milwaukee, WI 53233

Independent Registered Public Accounting Firm

Ernst & Young LLP

200 Clarendon Street

Boston, MA 02116

Legal Counsel

Dechert LLP

1095 Avenue of the Americas

New York, NY 10036

Counsel to the Independent

Trustees

Perkins Coie LLP

1155 Avenue of the Americas

New York, New York 10036

ALTERNATIVE INVESTMENT PARTNERS

ABSOLUTE RETURN FUND

Financial Statements with Report of Independent

Registered Public Accounting Firm

For the Year Ended December 31, 2023

Oath and Affirmation

To the best of my knowledge and belief, the information contained in this document is accurate and

complete.

Lee Spector, Executive Director of Morgan Stanley Alternative Investment LLC, the General Partner of

Morgan Stanley AIP GP LP, the Commodity Pool Operator of Alternative Investments Partners Absolute

Return Fund

(This oath is required by Section 4.12(c)(3) of the Commodity Futures Trading Commission Regulations under the

Commodity Exchange Act, as amended.)

Alternative Investment Partners Absolute Return Fund

Financial Statements with Report of

Independent Registered Public Accounting Firm

For the Year Ended December 31, 2023

Contents

Management’s Discussion of Fund Performance (Unaudited)………………………………………1

Report of Independent Registered Public Accounting Firm 4

Audited Financial Statements

Statement of Assets and Liabilities 5

Statement of Operations 6

Statements of Changes in Net Assets 7

Statement of Cash Flows 8

Schedule of Investments 9

Notes to Financial Statements 14

Proxy Voting Policies and Procedures and Proxy Voting Record (Unaudited) 27

Quarterly Portfolio Schedule (Unaudited) 27

U.S. Privacy Policy (Unaudited) 28

Information Concerning Trustees and Officers (Unaudited) 30

1

Alternative Investment Partners Absolute Return Fund

Management’s Discussion of Fund Performance

Investment Objective and Strategy Summary

The Fund’s investment objective is to seek capital appreciation principally through investing in

investment funds (“Investment Funds”) managed by third party investment managers who employ a

variety of “absolute return” investment strategies in pursuit of attractive risk-adjusted returns consistent

with the preservation of capital.

The Fund invests substantially all its assets in private investment funds (commonly referred to as hedge

funds) that are managed by a select group of alternative investment managers that employ different

“absolute return” investment strategies in pursuit of attractive risk-adjusted returns consistent with the

preservation of capital. “Absolute return” refers to a broad class of investment strategies that are managed

without reference to the performance of equity, debt and other markets. “Absolute return” investment

strategies allow unaffiliated third-party investment managers the flexibility to use leveraged or short-sale

positions to take advantage of perceived inefficiencies across the global capital markets. These strategies

are in contrast to the investment programs of “traditional” registered investment companies, such as

mutual funds. Absolute return strategies can be contrasted with “relative return strategies” which

generally seek to outperform a corresponding benchmark equity or fixed income index. The Fund seeks

attractive “risk-adjusted” returns, which are returns adjusted to take into account the volatility of those

returns. The Fund intends to invest in private investment funds that employ the following principal

strategies: relative value strategies, security selection strategies, specialist credit strategies and directional

strategies.

Performance Discussion

Total Returns

One Year Five Years Ten Years

Alternative Investment Partners Absolute Return Fund 6.53% 6.91% 4.96%

Average Annual

2

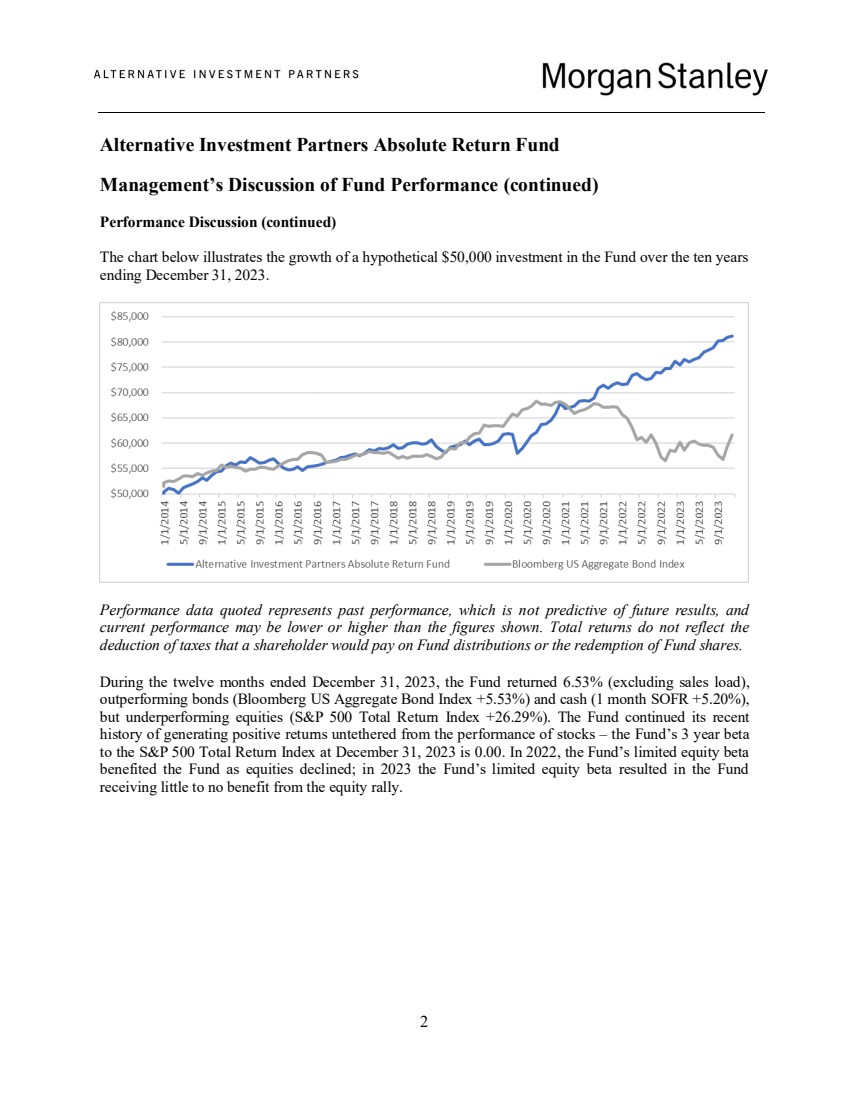

Alternative Investment Partners Absolute Return Fund

Management’s Discussion of Fund Performance (continued)

Performance Discussion (continued)

The chart below illustrates the growth of a hypothetical $50,000 investment in the Fund over the ten years

ending December 31, 2023.

Performance data quoted represents past performance, which is not predictive of future results, and

current performance may be lower or higher than the figures shown. Total returns do not reflect the

deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares.

During the twelve months ended December 31, 2023, the Fund returned 6.53% (excluding sales load),

outperforming bonds (Bloomberg US Aggregate Bond Index +5.53%) and cash (1 month SOFR +5.20%),

but underperforming equities (S&P 500 Total Return Index +26.29%). The Fund continued its recent

history of generating positive returns untethered from the performance of stocks – the Fund’s 3 year beta

to the S&P 500 Total Return Index at December 31, 2023 is 0.00. In 2022, the Fund’s limited equity beta

benefited the Fund as equities declined; in 2023 the Fund’s limited equity beta resulted in the Fund

receiving little to no benefit from the equity rally.

3

Alternative Investment Partners Absolute Return Fund

Management’s Discussion of Fund Performance (continued)

Performance Discussion (continued)

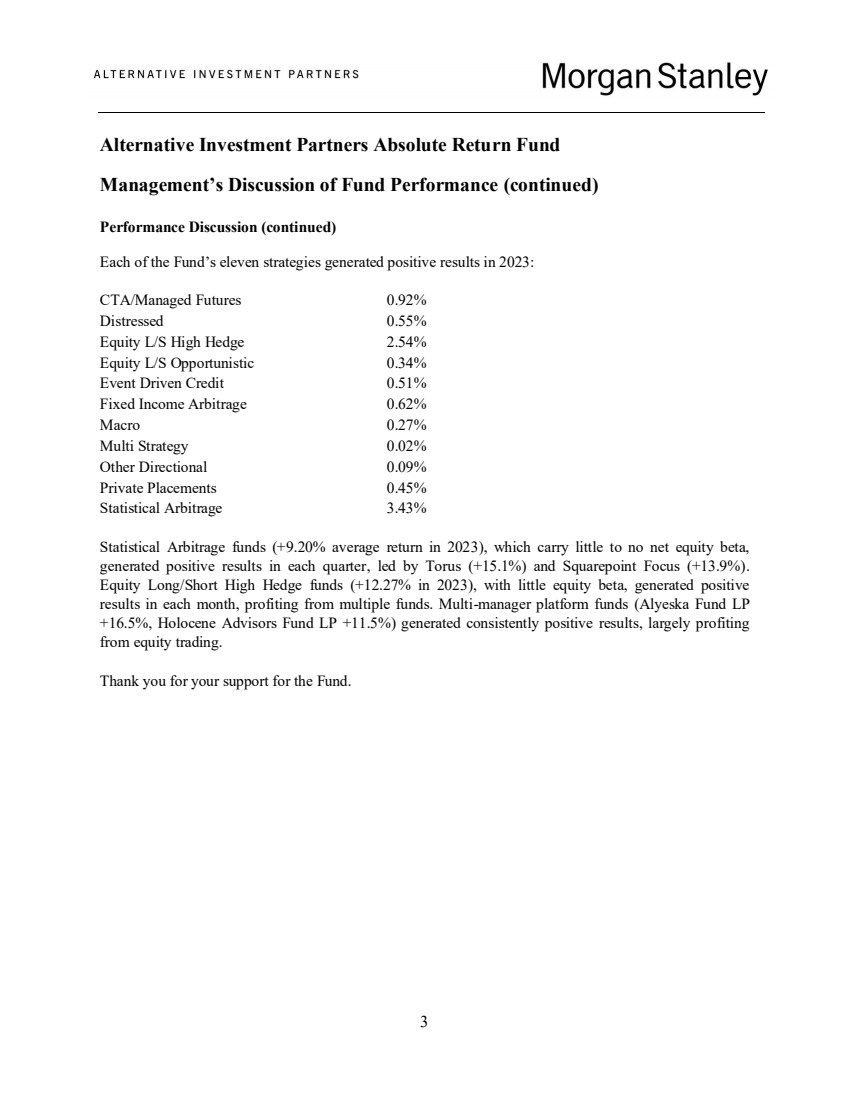

Each of the Fund’s eleven strategies generated positive results in 2023:

CTA/Managed Futures 0.92%

Distressed 0.55%

Equity L/S High Hedge 2.54%

Equity L/S Opportunistic 0.34%

Event Driven Credit 0.51%

Fixed Income Arbitrage 0.62%

Macro 0.27%

Multi Strategy 0.02%

Other Directional 0.09%

Private Placements 0.45%

Statistical Arbitrage 3.43%

Statistical Arbitrage funds (+9.20% average return in 2023), which carry little to no net equity beta,

generated positive results in each quarter, led by Torus (+15.1%) and Squarepoint Focus (+13.9%).

Equity Long/Short High Hedge funds (+12.27% in 2023), with little equity beta, generated positive

results in each month, profiting from multiple funds. Multi-manager platform funds (Alyeska Fund LP

+16.5%, Holocene Advisors Fund LP +11.5%) generated consistently positive results, largely profiting

from equity trading.

Thank you for your support for the Fund.

4

Report of Independent Registered Public Accounting Firm

To the Shareholders and Board of Trustees of Alternative Investment Partners Absolute Return Fund

Opinion on the Financial Statements

We have audited the accompanying statement of assets and liabilities of Alternative Investment Partners

Absolute Return Fund (the “Fund”), including the schedule of investments, as of December 31, 2023, and the

related statements of operations and cash flows for the year then ended, the statements of changes in net assets

for each of the two years in the period then ended and the related notes (collectively referred to as the “financial

statements”). In our opinion, the financial statements present fairly, in all material respects, the financial position

of the Fund at December 31, 2023, the results of its operations and its cash flows for the year then ended and the

changes in its net assets for each of the two years in the period then ended, in conformity with U.S. generally

accepted accounting principles.

Basis for Opinion

These financial statements are the responsibility of the Fund’s management. Our responsibility is to express an

opinion on the Fund’s financial statements based on our audits. We are a public accounting firm registered with

the Public Company Accounting Oversight Board (United States) (“PCAOB”) and are required to be

independent with respect to the Fund in accordance with the U.S. federal securities laws and the applicable rules

and regulations of the Securities and Exchange Commission and the PCAOB.

We conducted our audits in accordance with the standards of the PCAOB. Those standards require that we plan

and perform the audit to obtain reasonable assurance about whether the financial statements are free of material

misstatement, whether due to error or fraud. The Fund is not required to have, nor were we engaged to perform,

an audit of the Fund’s internal control over financial reporting. As part of our audits, we are required to obtain

an understanding of internal control over financial reporting but not for the purpose of expressing an opinion on

the effectiveness of the Fund’s internal control over financial reporting. Accordingly, we express no such

opinion.

Our audits included performing procedures to assess the risks of material misstatement of the financial

statements, whether due to error or fraud, and performing procedures that respond to those risks. Such procedures

included examining, on a test basis, evidence regarding the amounts and disclosures in the financial statements.

Our procedures included confirmation of investments owned as of December 31, 2023, by correspondence with

the custodian, management of the investment funds and others. Our audits also included evaluating the

accounting principles used and significant estimates made by management, as well as evaluating the overall

presentation of the financial statements. We believe that our audits provide a reasonable basis for our opinion.

We have served as the auditor of one or more Morgan Stanley investment companies since 2000.

Boston, Massachusetts

February 29, 2024

The accompanying notes are an integral part of these financial statements and should be used in conjunction herewith.

5

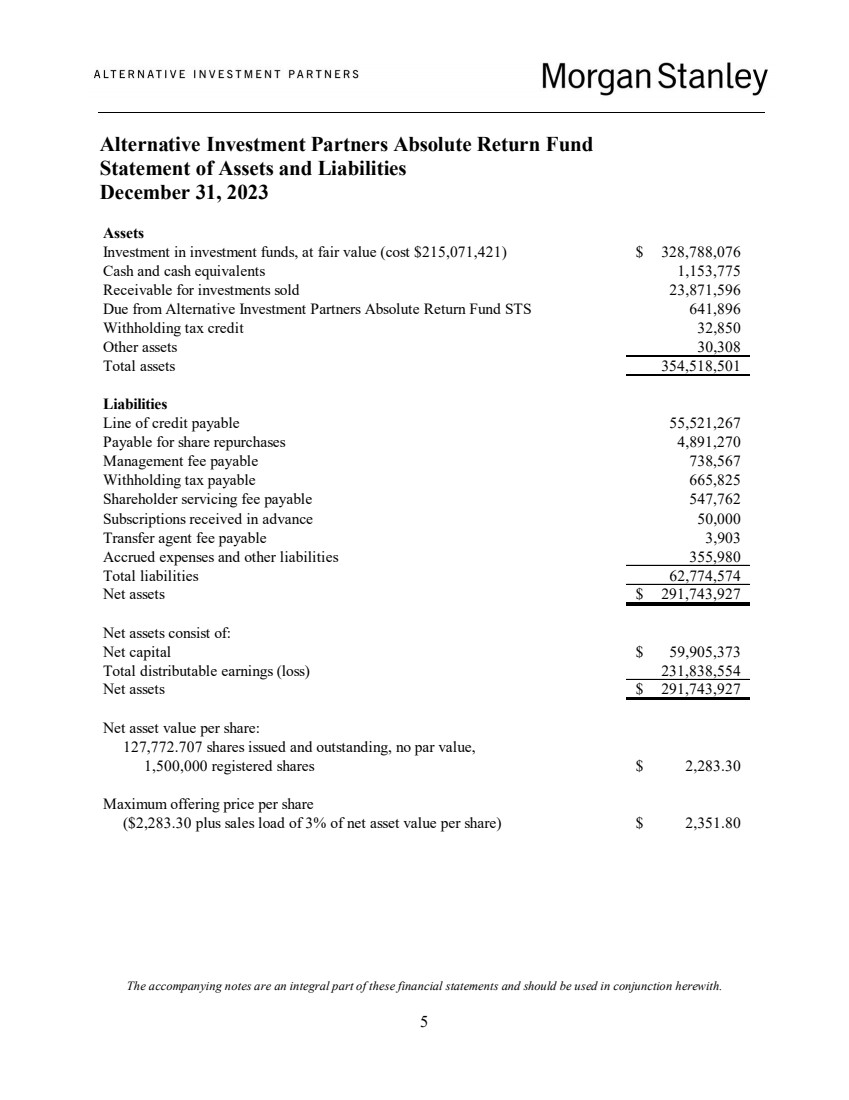

Alternative Investment Partners Absolute Return Fund

Statement of Assets and Liabilities

December 31, 2023

Assets

Investment in investment funds, at fair value (cost $215,071,421) $ 328,788,076

Cash and cash equivalents 1,153,775

23,871,596

641,896

32,850

Other assets 30,308

Total assets 354,518,501

Liabilities

Line of credit payable 55,521,267

Payable for share repurchases 4,891,270

Management fee payable 738,567

Withholding tax payable 665,825

Shareholder servicing fee payable 547,762

Subscriptions received in advance 50,000

Transfer agent fee payable 3,903

Accrued expenses and other liabilities 355,980

Total liabilities 62,774,574

Net assets $ 291,743,927

Net assets consist of:

Net capital $ 59,905,373

Total distributable earnings (loss) 231,838,554

Net assets $ 291,743,927

Net asset value per share:

127,772.707 shares issued and outstanding, no par value,

1,500,000 registered shares $ 2,283.30

Maximum offering price per share

($2,283.30 plus sales load of 3% of net asset value per share) $ 2,351.80

Due from Alternative Investment Partners Absolute Return Fund STS

Withholding tax credit

Receivable for investments sold

The accompanying notes are an integral part of these financial statements and should be used in conjunction herewith.

6

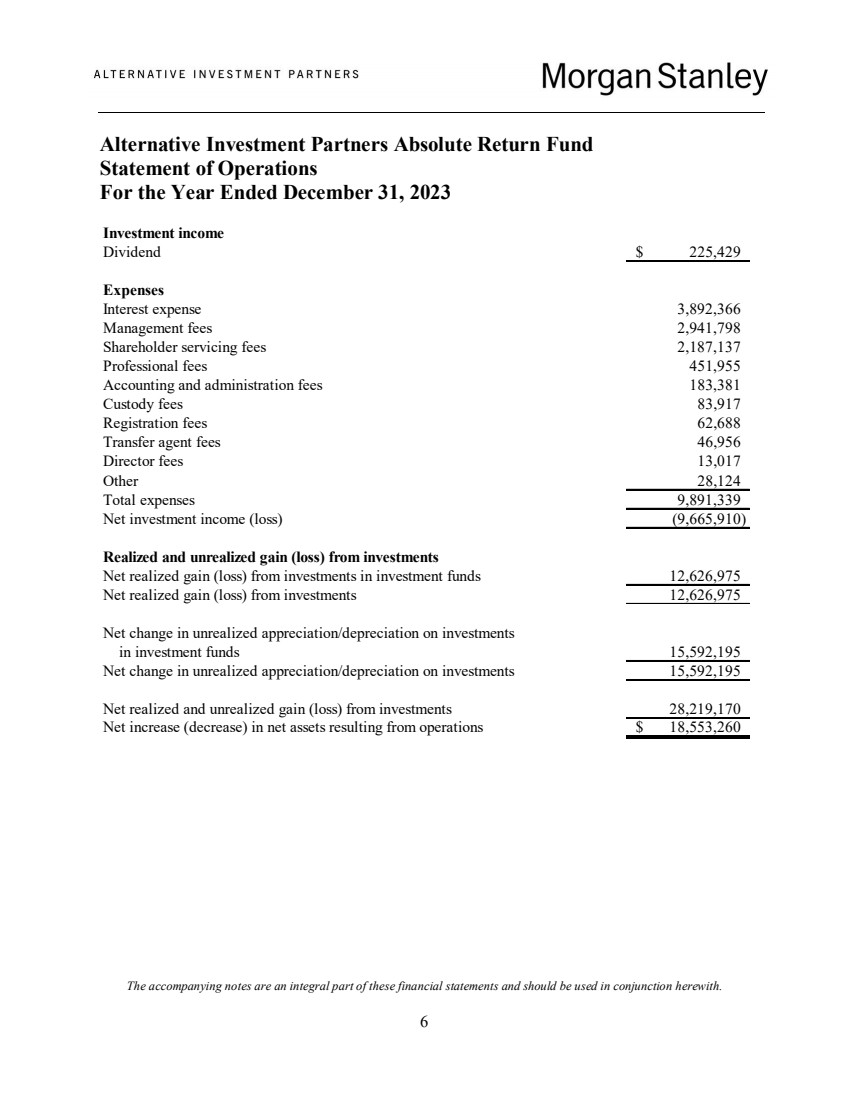

Alternative Investment Partners Absolute Return Fund

Statement of Operations

For the Year Ended December 31, 2023

Investment income

Dividend $ 225,429

Expenses

Interest expense 3,892,366

Management fees 2,941,798

Shareholder servicing fees 2,187,137

Professional fees 451,955

Accounting and administration fees 183,381

Custody fees 83,917

Registration fees 62,688

Transfer agent fees 46,956

Director fees 13,017

Other 28,124

Total expenses 9,891,339

Net investment income (loss) (9,665,910)

Realized and unrealized gain (loss) from investments

Net realized gain (loss) from investments in investment funds 12,626,975

Net realized gain (loss) from investments 12,626,975

Net change in unrealized appreciation/depreciation on investments

in investment funds 15,592,195

Net change in unrealized appreciation/depreciation on investments 15,592,195

Net realized and unrealized gain (loss) from investments 28,219,170

Net increase (decrease) in net assets resulting from operations $ 18,553,260

The accompanying notes are an integral part of these financial statements and should be used in conjunction herewith.

7

Alternative Investment Partners Absolute Return Fund

Statements of Changes in Net Assets

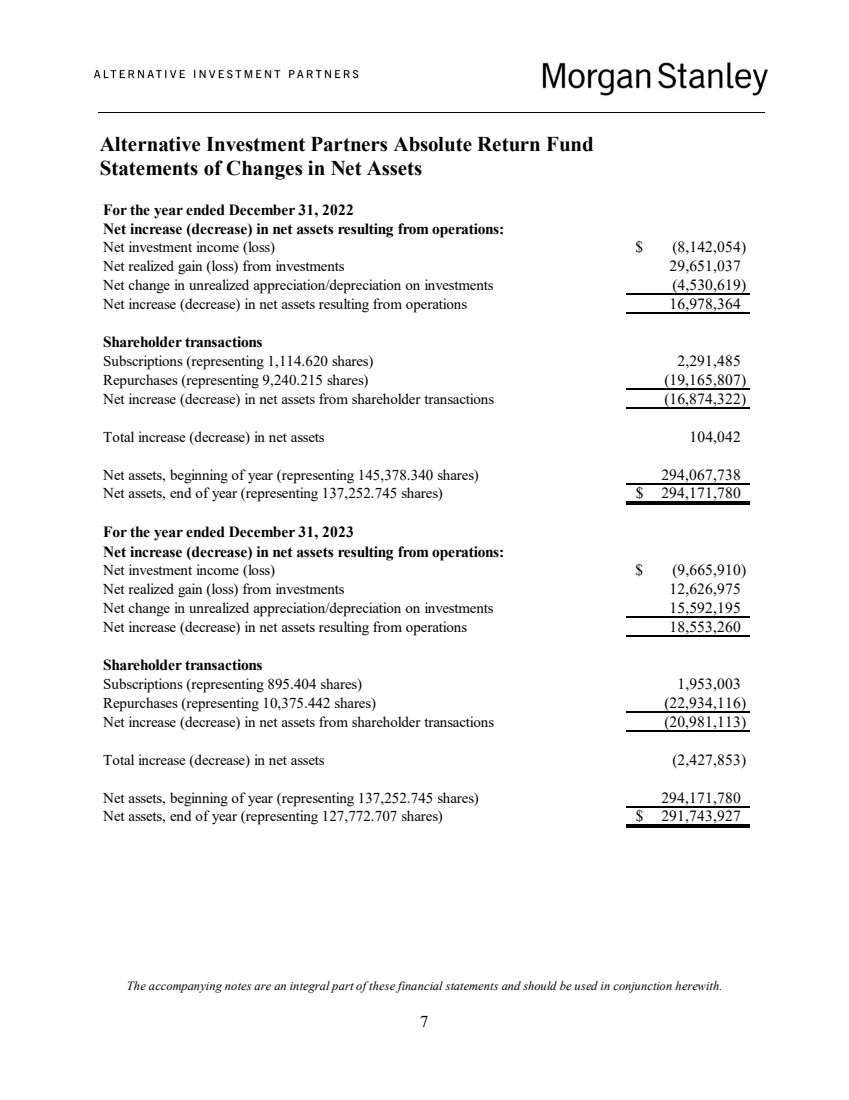

For the year ended December 31, 2022

Net increase (decrease) in net assets resulting from operations:

Net investment income (loss) $ (8,142,054)

Net realized gain (loss) from investments 29,651,037

Net change in unrealized appreciation/depreciation on investments (4,530,619)

Net increase (decrease) in net assets resulting from operations 16,978,364

Shareholder transactions

Subscriptions (representing 1,114.620 shares) 2,291,485

Repurchases (representing 9,240.215 shares) (19,165,807)

Net increase (decrease) in net assets from shareholder transactions (16,874,322)

Total increase (decrease) in net assets 104,042

Net assets, beginning of year (representing 145,378.340 shares) 294,067,738

Net assets, end of year (representing 137,252.745 shares) $ 294,171,780

Net increase (decrease) in net assets resulting from operations:

Net investment income (loss) $ (9,665,910)

Net realized gain (loss) from investments 12,626,975

Net change in unrealized appreciation/depreciation on investments 15,592,195

Net increase (decrease) in net assets resulting from operations 18,553,260

Shareholder transactions

Subscriptions (representing 895.404 shares) 1,953,003

Repurchases (representing 10,375.442 shares) (22,934,116)

Net increase (decrease) in net assets from shareholder transactions (20,981,113)

Total increase (decrease) in net assets (2,427,853)

Net assets, beginning of year (representing 137,252.745 shares) 294,171,780

Net assets, end of year (representing 127,772.707 shares) $ 291,743,927

For the year ended December 31, 2023

The accompanying notes are an integral part of these financial statements and should be used in conjunction herewith.

8

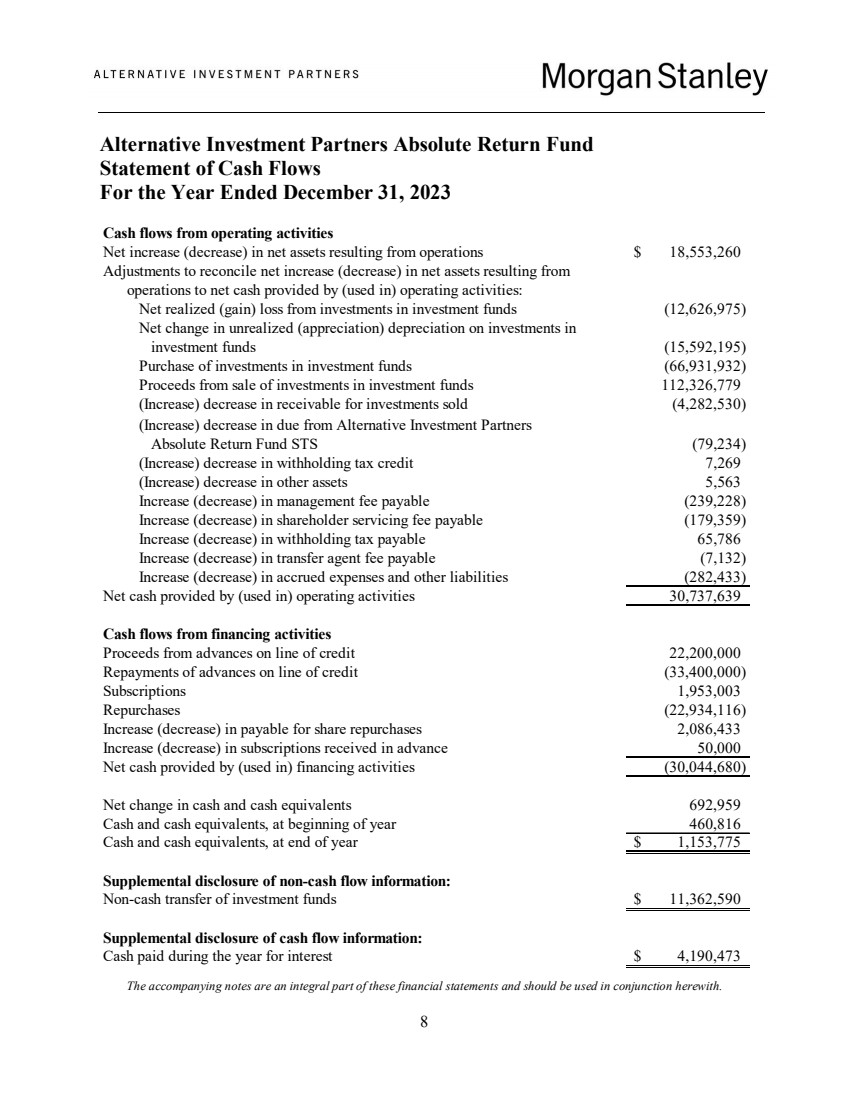

Alternative Investment Partners Absolute Return Fund

Statement of Cash Flows

For the Year Ended December 31, 2023

Cash flows from operating activities

Net increase (decrease) in net assets resulting from operations $ 18,553,260

Adjustments to reconcile net increase (decrease) in net assets resulting from

operations to net cash provided by (used in) operating activities:

Net realized (gain) loss from investments in investment funds (12,626,975)

Net change in unrealized (appreciation) depreciation on investments in

investment funds (15,592,195)

Purchase of investments in investment funds (66,931,932)

Proceeds from sale of investments in investment funds 112,326,779

(Increase) decrease in receivable for investments sold (4,282,530)

(Increase) decrease in due from Alternative Investment Partners

Absolute Return Fund STS (79,234)

(Increase) decrease in withholding tax credit 7,269

(Increase) decrease in other assets 5,563

Increase (decrease) in management fee payable (239,228)

Increase (decrease) in shareholder servicing fee payable (179,359)

Increase (decrease) in withholding tax payable 65,786

Increase (decrease) in transfer agent fee payable (7,132)

Increase (decrease) in accrued expenses and other liabilities (282,433)

Net cash provided by (used in) operating activities 30,737,639

Cash flows from financing activities

Proceeds from advances on line of credit 22,200,000

Repayments of advances on line of credit (33,400,000)

Subscriptions 1,953,003

Repurchases (22,934,116)

Increase (decrease) in payable for share repurchases 2,086,433

Increase (decrease) in subscriptions received in advance 50,000

Net cash provided by (used in) financing activities (30,044,680)

Net change in cash and cash equivalents 692,959

Cash and cash equivalents, at beginning of year 460,816

Cash and cash equivalents, at end of year $ 1,153,775

Supplemental disclosure of non-cash flow information:

Non-cash transfer of investment funds $ 11,362,590

Supplemental disclosure of cash flow information:

Cash paid during the year for interest $ 4,190,473

The accompanying notes are an integral part of these financial statements and should be used in conjunction herewith.

9

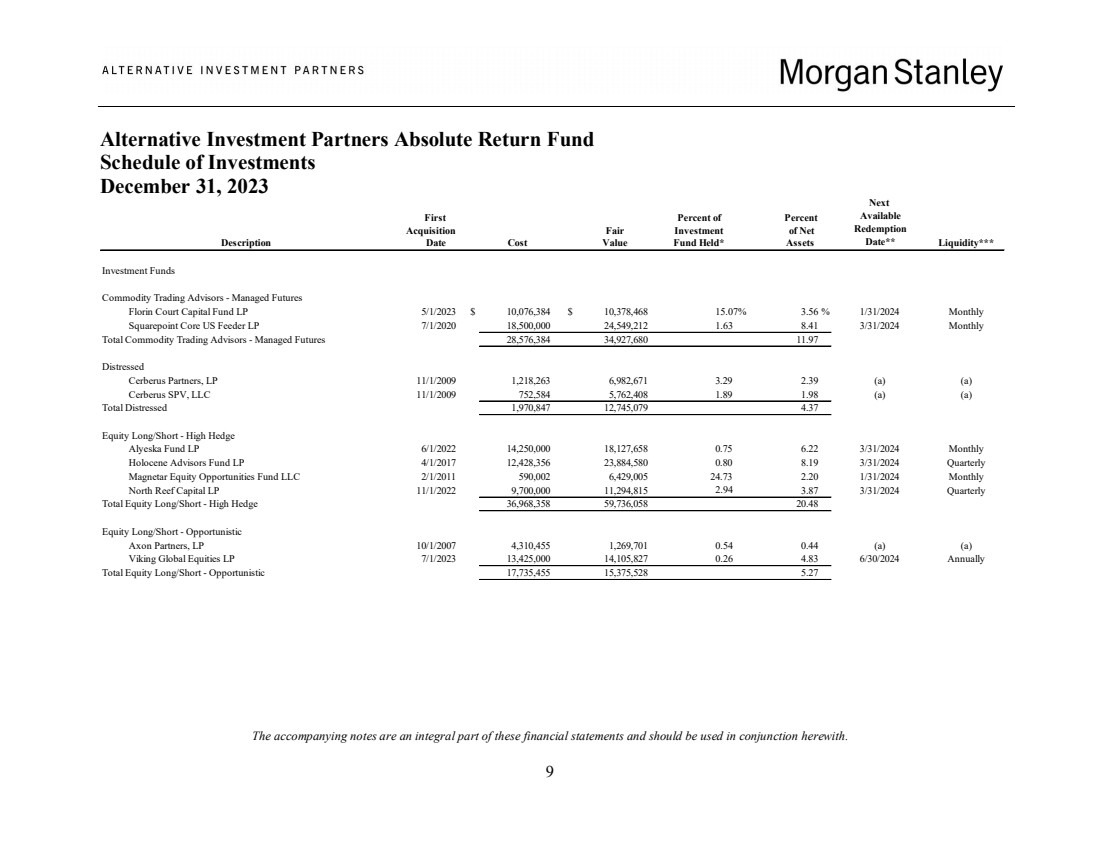

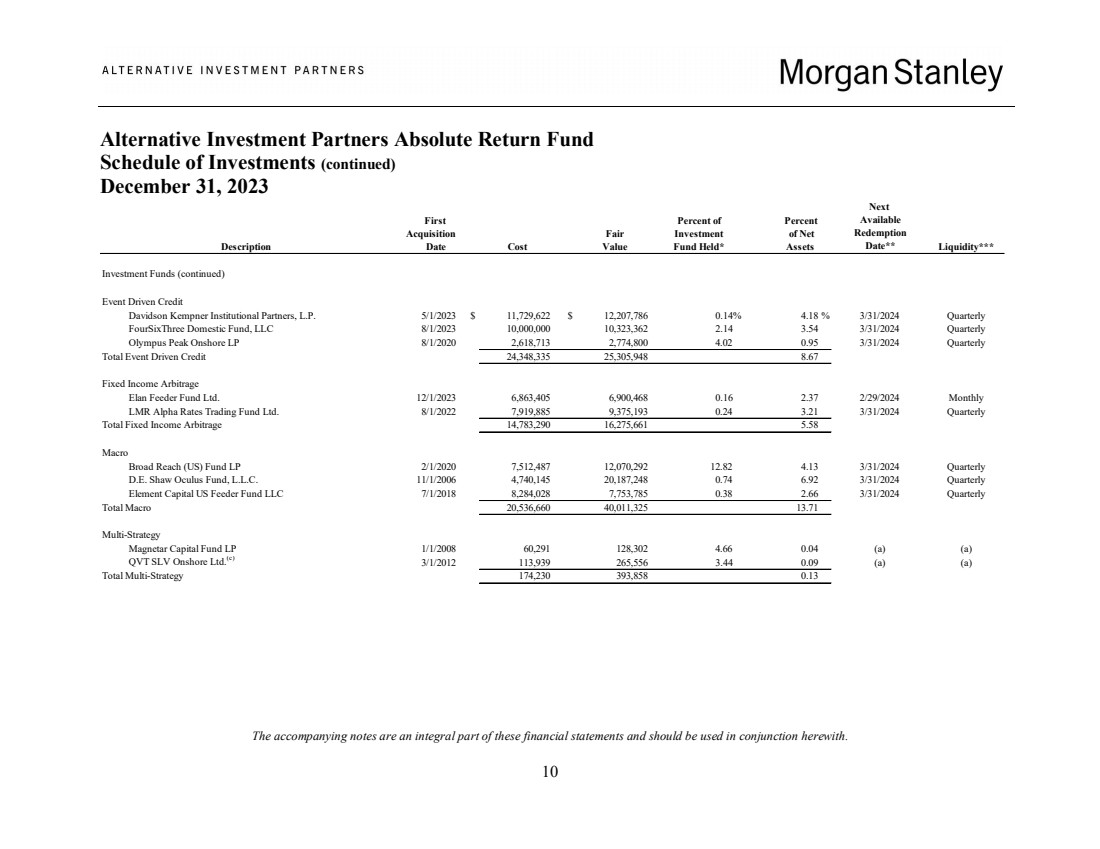

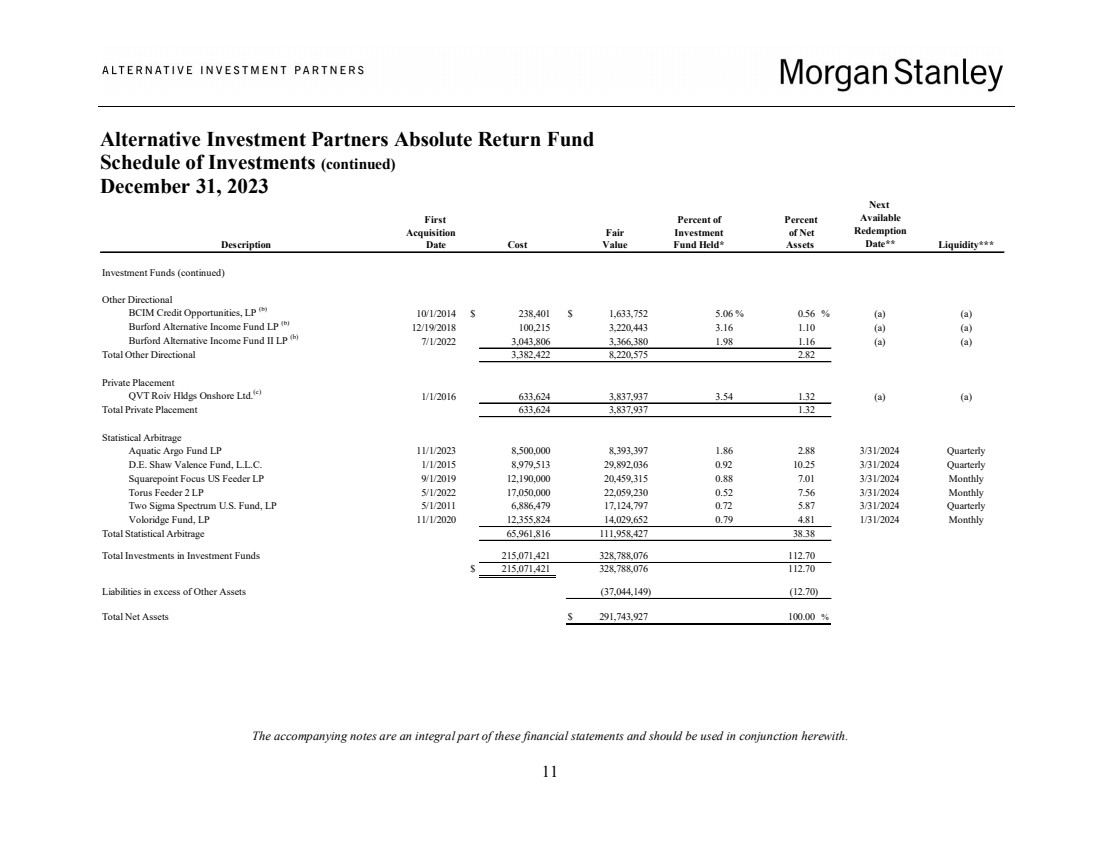

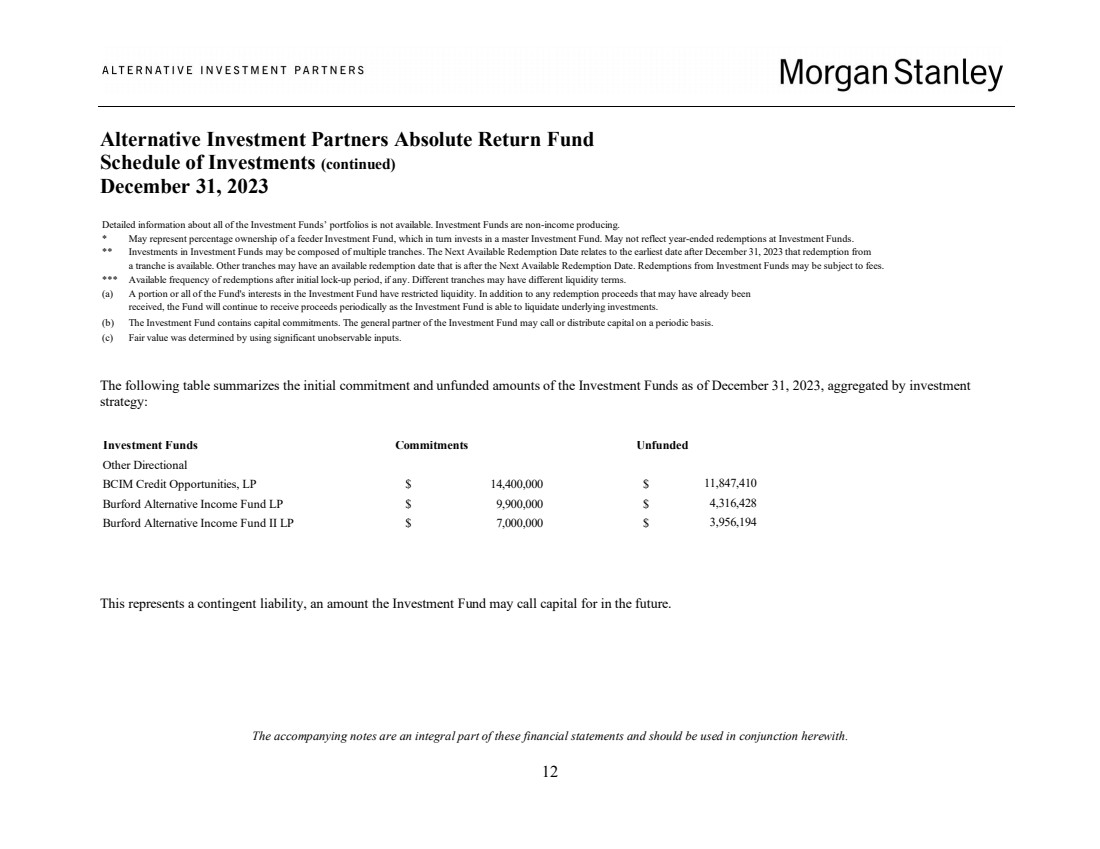

Alternative Investment Partners Absolute Return Fund

Schedule of Investments

December 31, 2023

Next

First Percent of Percent Available

Acquisition Fair Investment of Net Redemption