portishead1

The Evidence for Alternative Investments

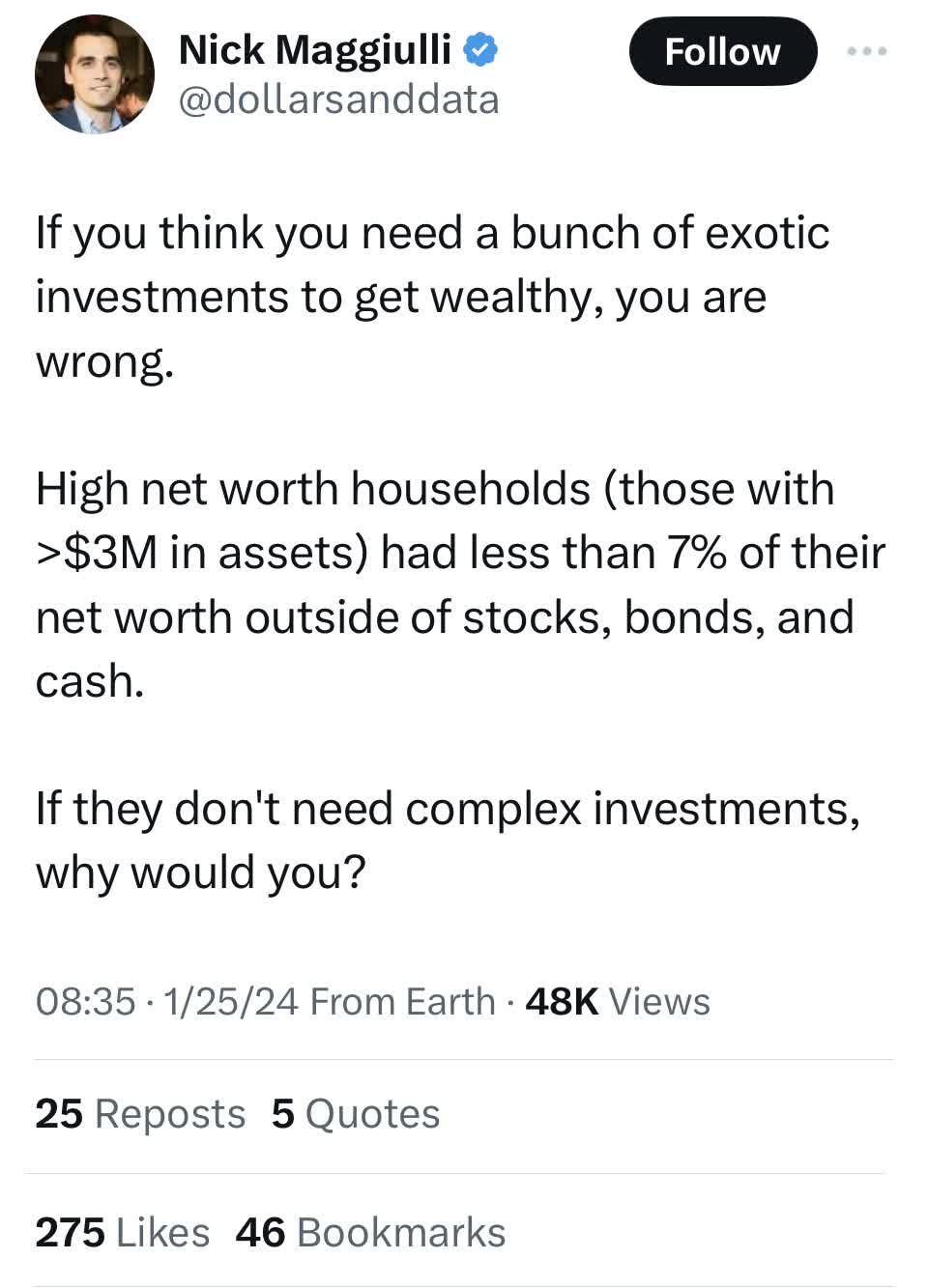

The common refrain from many financial advisors is that alternative investments are unnecessary. For example, I recently read an article by Nick Maggiulli from Ritholtz Wealth Management, about how millionaires invest. In the article, he puts forth data from Vanguard showing that investors in this category of wealth generally have the majority of their money in stocks, bonds, and cash. Mr. Maggiulli states in his post on X advertising the blog post:

X/Twitter

Many investors would concur with this conclusion; however, the evidence shows this is not only misleading, but also highly fueled by recency bias, and contrary to the evidence. Further down in the piece he even demonstrates that high net worth investors invest a large portion of their wealth in alternative assets, contrary to the Vanguard study cited earlier.

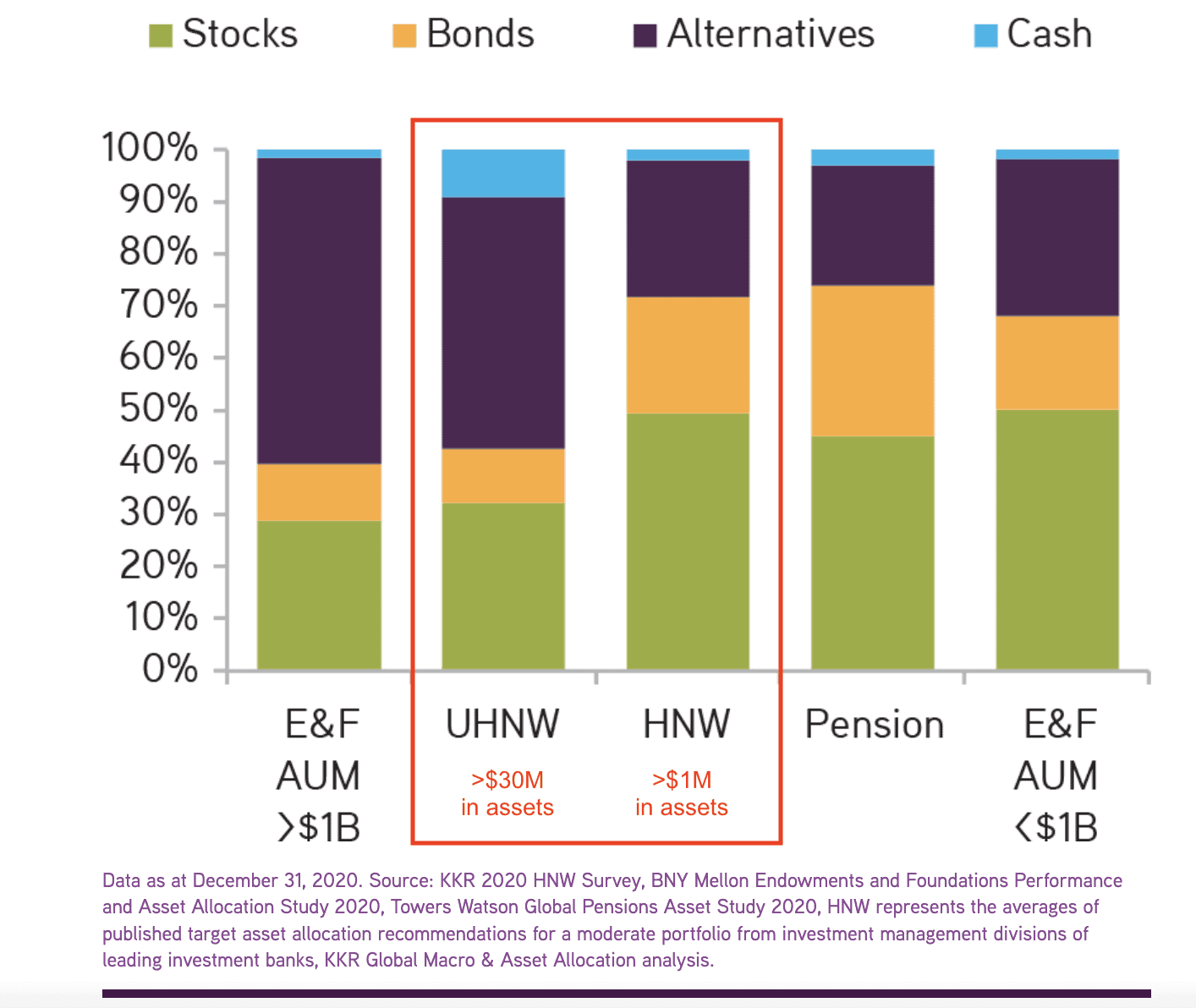

KKR 2020 HNW Survey

But for the sake of argument, let’s take the assumption at face value and see if we can explain this phenomenon. The reasons individuals with $3M+ net-worth surveyed by Vanguard would have so much of their investments in stocks, bonds, and cash, rather than alternative investments could be for many reasons.

First, the largest wealth building tool for these individuals has likely been their 401(K) and other retirement accounts. These accounts tend to be limited in the choices offered to individuals.

Second, is a lack of understanding of investment theory, and portfolio construction. In my experience of working with high and ultra-high net worth individuals and families they have developed a core competency in their chosen field and lack the time or in some cases interest to learn about these topics. This is to their credit however, because it is the highly focused effort in their chosen field that explains why they have been so successful. In many cases default investment strategies such as the S&P 500 have been chosen in some cases without thought.

Finally, these individuals tend to have a high savings rate which more than anything is why they have achieved such success in accumulating assets.

One additional caveat is that many of these individuals may own their own businesses where they keep a large portion of their wealth. (In fairness the original blog post mentioned does go through this factor.)

The most important point is that Mr. Maggiulli makes the case that because the wealthy don’t do this that means no one else needs to either. Just because the wealthy households surveyed do not hold meaningful allocations to alternative investments in the past does not have any bearing on whether they should, or you should. Ultimately the decision to invest in alternative assets should be based on each individual’s goals. The question is, are investments in alternatives supported by the evidence, which is where we now turn?

The Case Against Alternatives: An Example of Recency Bias

Ultimately investors choose whether to invest in something or not based on its recent performance. This recency bias explains why investors choose US stock bias over international stocks, why investors choose a stock bias over bonds (I have proven here this isn’t always wise,) and why everyone seems to hate alternative investments.

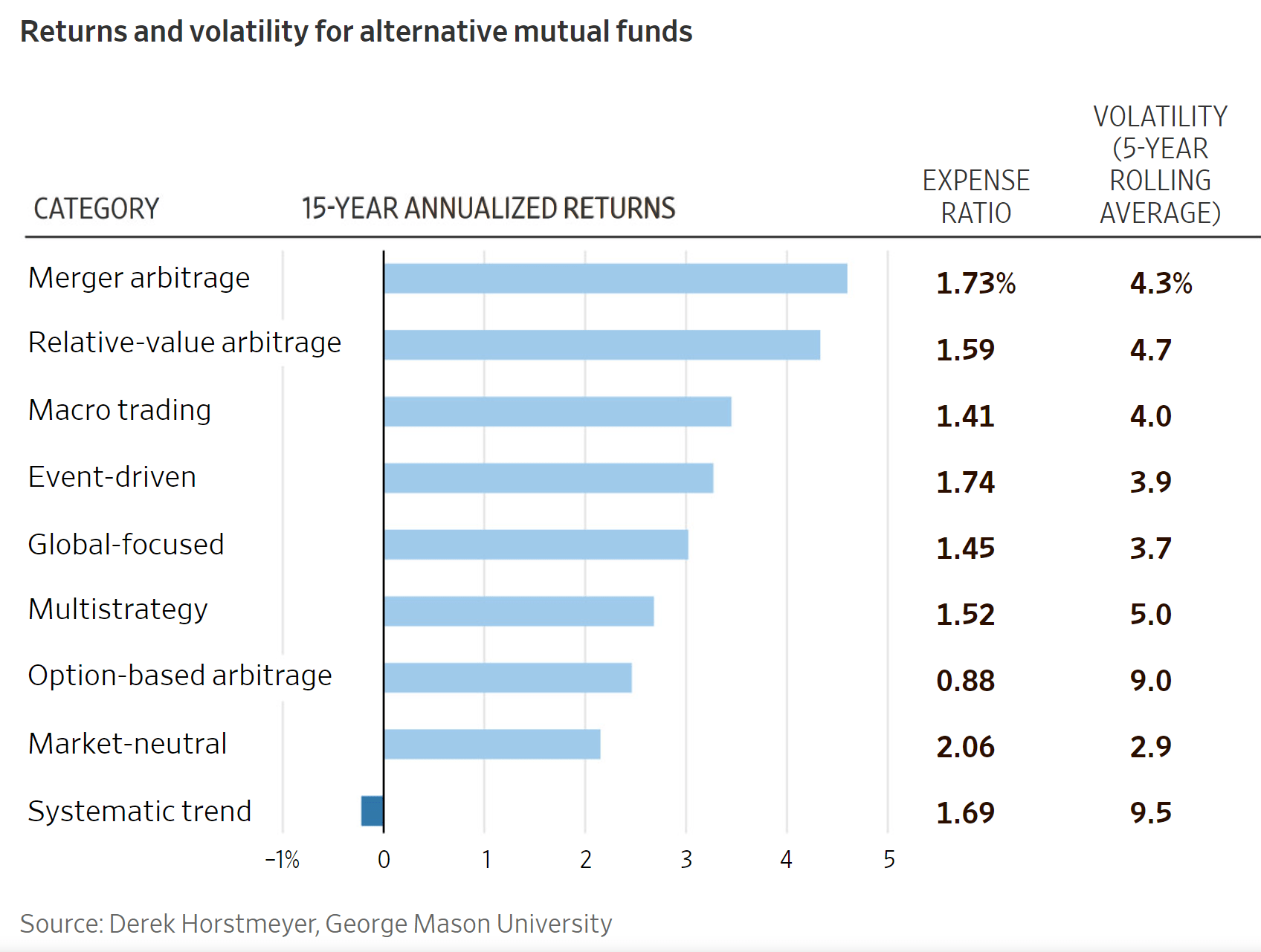

In the past alternative investments have had a reputation for being high-fee products that have performance that most accurately mimics cash at best. In an article in the Wall Street Journal, author Professor Derek Horstmeyer of George Mason University makes the case against these investments.

So which type of strategy has fared best over the past 15 years on a risk-adjusted basis? To tackle this issue, my research assistants (Kurshat Gheni and Heyuan Li) and I pulled all U.S.-dollar denominated alternative mutual funds listed in the U.S. We then separated them according to their Morningstar category of focus. To be included in the final sample, there needed to be 20-plus mutual funds in a particular category.

The final list of alternative mutual-fund categories we examined: market-neutral, event-driven, macro trading, multistrategy, option-based arbitrage, relative-value arbitrage, systematic trend, global-focused and merger arbitrage.

With these categories in hand, we then explored the average annualized returns, the volatility and the average fees within each group. The first interesting finding: Across the board, the alternative funds much more resembled short to midterm bond mutual funds in their risk and return characteristics.

WSJ

This analysis aggregates the data, uses a small sample period, and a myriad of other issues. But I will take the results at face value, alternative funds have done a poor job over the last 15 years, producing returns that were more like bonds. However, in making this conclusion the author does not consider the fact that they are supposed to. Alternative investments are supposed to be an uncorrelated source of returns. You do not expect an uncorrelated source of returns to do well during a rip-roaring bull market for equities as we have had for the last 15 years.

But more importantly, the real reason to invest in something or not should be based not on its recent performance but on the evidence. I have provided a great deal of evidence on managed futures here, and I would encourage investors to read that piece for a deeper analysis, as I will skip managed futures here and instead focus on another alternative strategy.

Most critics of alternative investments compare their performance to the S&P 500 index, as the WSJ piece does. This alone is a form of home country and recency bias in itself. But these products should not be compared to a large cap stock index with a momentum bias.

Investors should think of alternative investments as uncorrelated sources of return, insurance against the periods when stocks and bonds go down together. Most of them are far better thought of as bond alternatives than stock alternatives, but ideally, they are uncorrelated with both of these traditional assets that dominate portfolios.

While I could write a far lengthier analysis exploring each of the single alternative strategies and their efficacy within a portfolio model, for the purposes of this piece I want to focus on a specific strategy, style premia.

Multi-strategy funds like style premia allow investors to hold multiple uncorrelated strategies in a single fund structure. Additionally, lower costs from mutual funds and ETFs for retail investors make these more palatable for asset allocators. But do they improve portfolio statistics?

Style Premia: A Case Study

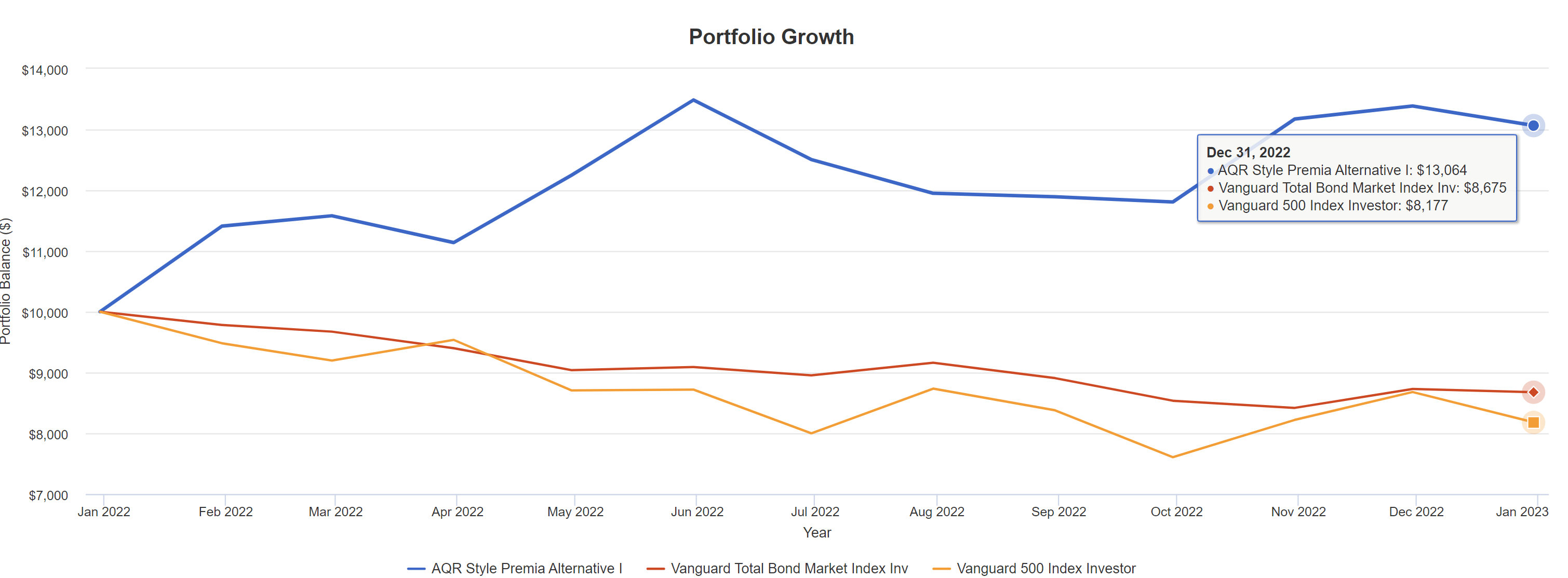

Let’s look at time periods that include a rapid increase in the stock market and rapid decrease in the stock market, followed by a return to the previous highs. We will define this as a full cycle for the purposes of this analysis. This will allow us to see how the alternative section of the portfolio performs in positive and negative environments for equity and fixed income. We are lucky enough to have this very structure of market returns in the period 2021-2023. This provides us with a perfect backdrop to analyze the performance of portfolios with and without these strategies.

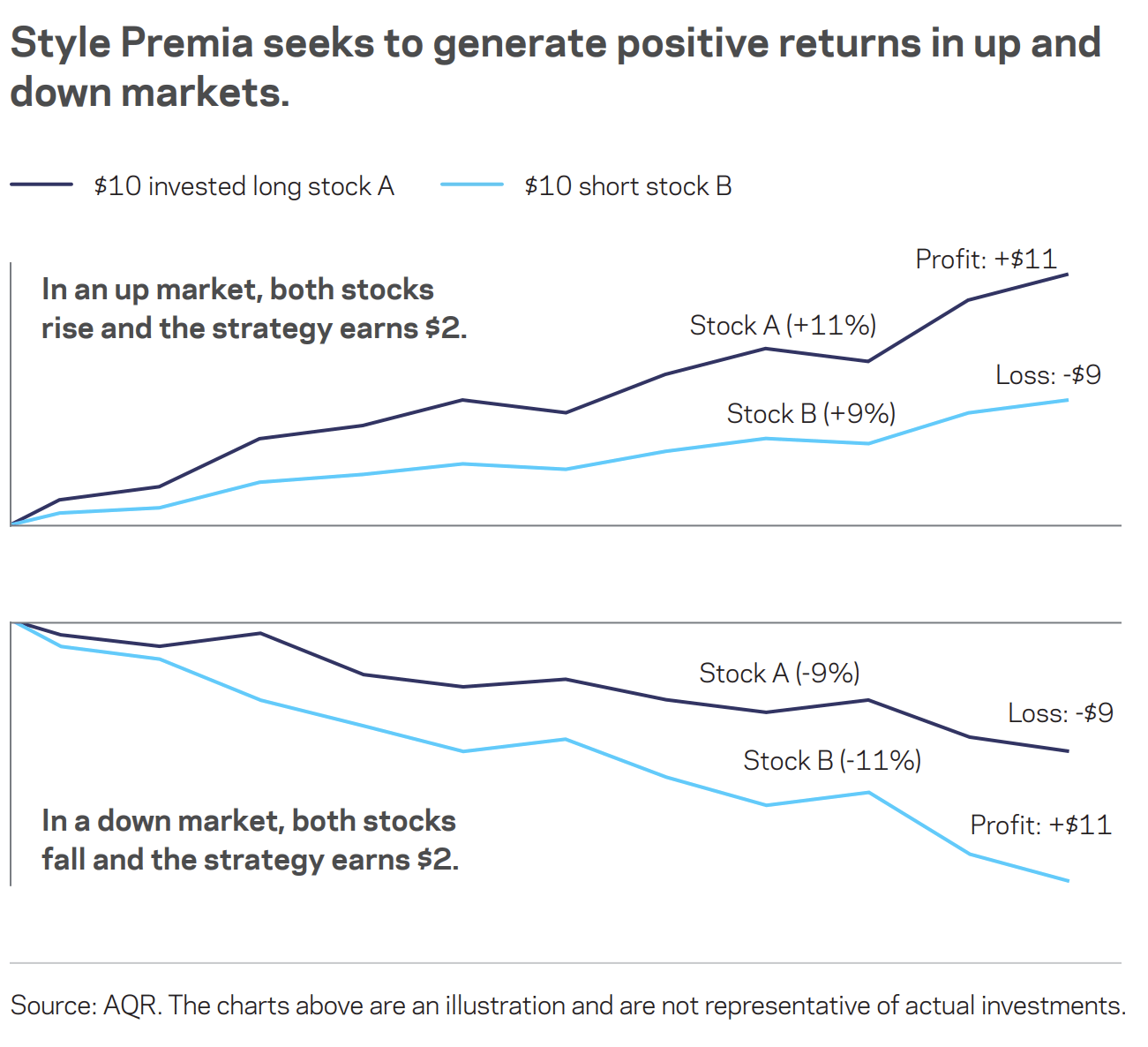

In this backtest we are going to use two multi-strategy funds, one is an index-based product iMGP DBi Hedge Strategy ETF (DBEH) which acts as an index of sorts aggregating the returns of 40 hedge funds before fees and seeks to beat the index through lower fees. Secondly, we are including the AQR Style Premia Fund (QSPIX). Style premia is a strategy in which investors seek to capture the alpha from taking long and short positions across a range of factors and asset classes.

I will also use a dual benchmark both the S&P 500 Index and a 50%/50% portfolio that does not include alternative assets. For this portfolio, we will allocate the portion going to alternative assets into short-term TIPS to mimic the inflation protection commonly associated with alternative strategies.

The purpose of this analysis is to see whether alternative investments make a difference in the risk and return characteristics of the portfolio.

Portfolio Visualizer

As you can see from the data, the portfolio with style premia included not only beat all of the other portfolios including the S&P 500 index for this period, but it did so while also reducing standard deviation, increasing the Sharpe and Sortino ratios, and lowering the overall correlation of the portfolio to the market. What is most impactful is the return in 2022, pictured below, when both stocks and bonds were down, Style Premia had a negative correlation with traditional asset classes and was up 30.64%. Also, note the negative correlation with traditional assets.

Portfolio Visualizer Portfolio Visualizer

The Evidence For Style Premia

Ronen Israel and Thomas Moloney wrote a piece in The Journal of Investing, entitled “Understanding Style Premia.” In the piece they go through the fundamental truth that most portfolios, including the standard 60%/40% portfolio, are dominated by equity risk. They then proceed to define the concept of styles as:

A style is a disciplined, systematic method of investing that can produce long-term positive returns across markets and asset groups, backed by robust data and economic theory.

The authors then proceed to review the literature on style investing beginning with the research of Eugene Fama and Kenneth French who discussed investment returns and style premia in two styles, value and size. Subsequent research progressed this idea to international stocks and other asset classes.

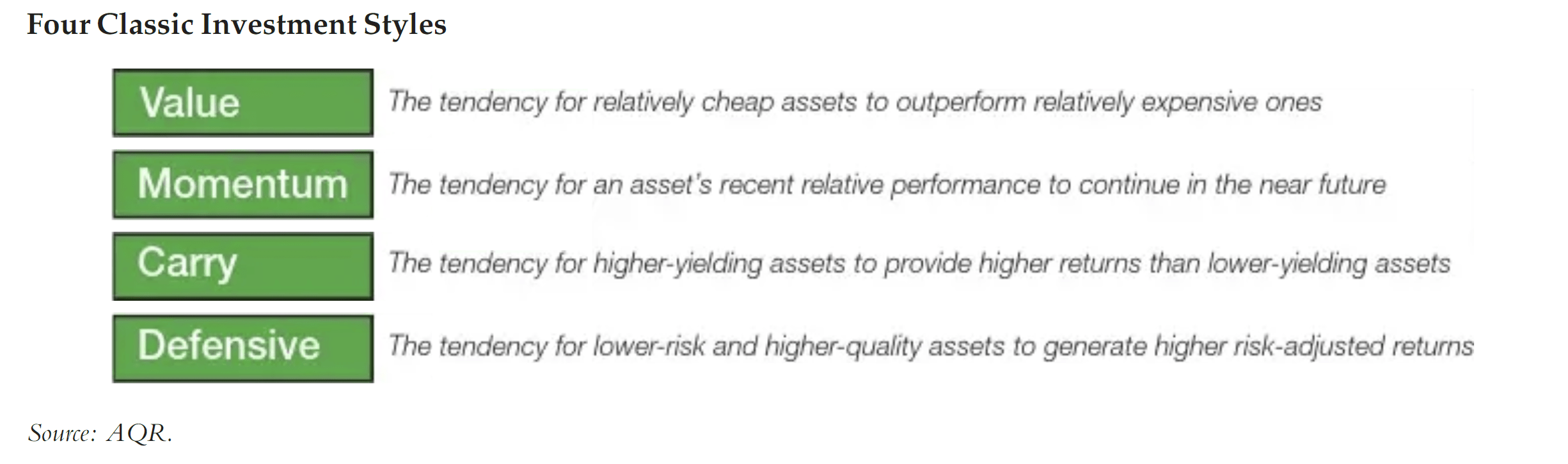

They list “four classic styles that have delivered persistent long-term performance across multiple, unrelated asset groups, in different markets, and in out-of-sample tests.” As you can see from the chart below, these four styles are value, momentum, carry, and defensive.

AQR Journal of Investing

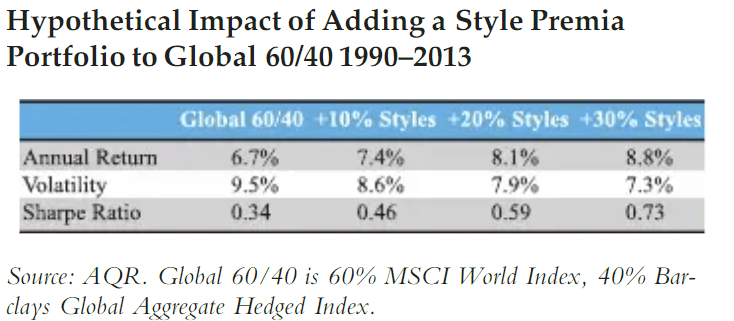

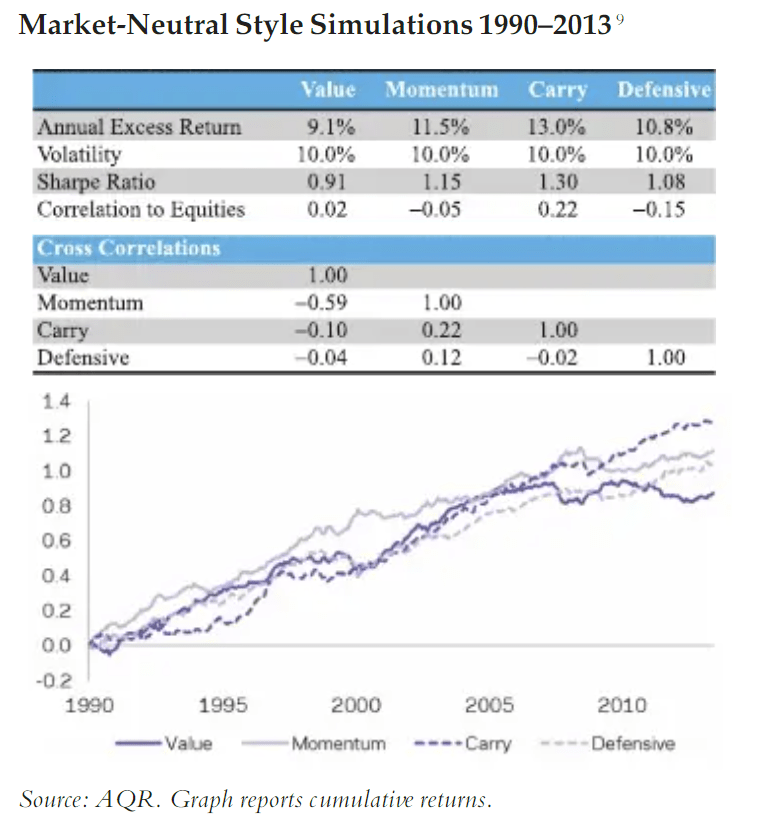

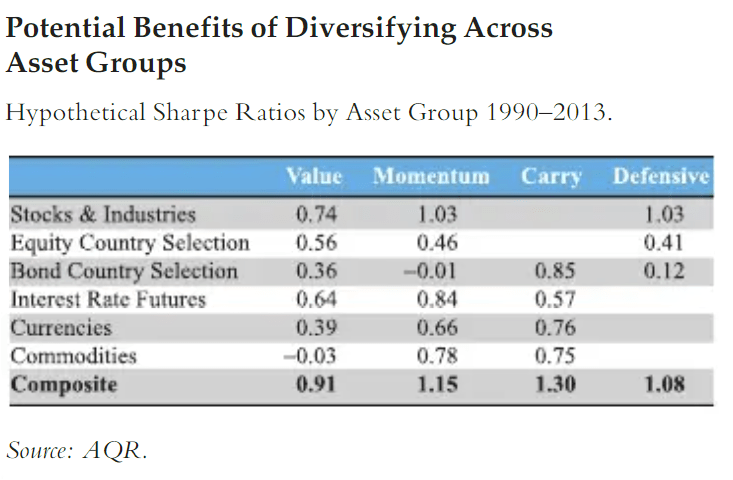

The authors then perform an analysis for the time period 1990-2013 in an effort to show the value of style premia strategies being added as a third pillar to traditional stock and bond portfolios. Their results give further evidence that incorporating this alternative strategy led to higher returns, lower risk characteristics, and better Sharpe ratios.

Journal of Investing Journal of Investing Journal of Investing

Diversification is one of the key elements in style premia portfolio design: the styles naturally diversify each other, which can help provide stronger and more consistent performance. While some style-asset pairs appear stronger than others over our sample period, we believe that the long-term efficacy of the composite styles is sufficiently similar that our aim is to build a well-balanced, diversified portfolio and not to strategically over- or under-weight certain styles.”

When we look around the world and into different asset classes, we see there are return premia to be had. Investors can choose to harvest these returns or continue to build traditional portfolios that over-rely on the risk-free rate of cash and cash equivalents, and market risk from equities commonly known as the equity risk premium (Rm-Rf.) The evidence clearly shows that investors who choose to employ a multi-factor, multi-style approach to investing have captured return premia, as well as reduced risk in multiple periods.

Conclusion

It is clear from the evidence the original assertion made that investors do not need, and implicitly are not benefited by alternative strategies is simply not supported by the evidence. Style premia has a clear benefit on traditional asset portfolios as demonstrated both by the team at AQR in their 1990-2013 analysis and in my own simulation provided here. The strategy can benefit investors in both rising and falling markets giving an uncorrelated source of returns commonly, when investors need it most.

AQR

One cannot minimize the impact of recency bias against alternative strategies. Like all assets, they go in and out of favor. This is why it is important for investors to build a multi-asset uncorrelated portfolio of stocks, bonds, and alternatives from around the world and hold said portfolio through thick and thin.

Over the long run, the premia from holding a diversified asset portfolio will far outweigh allocating assets according to the recency bias of the moment. Even if it seems the current bull market will go on forever, we all know, it won’t. International stocks will outperform at some point, bonds will outperform at some point, and yes, alternative strategies will outperform at some point. Holding a portfolio of all of these assets in weights that are best for your situation is likely to be the best long-term investment strategy for an uncertain future.

stock price analysis and earnings preview")

{kind=link}