cogal/E+ via Getty Images

The first test of “the inflation bump thesis”

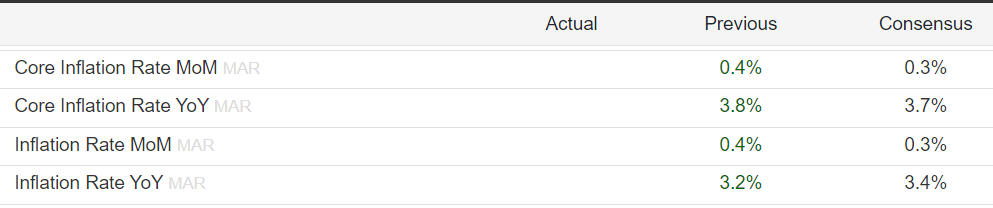

The US Bureau of Labor Statistics is set to release the CPI inflation numbers for March on April 10th. This will be a pivotal data report with significant implications for the financial markets.

Specifically, the core CPI inflation data was “hot” in January and February, rising at 0.4% MoM, which was above expectations, and also well above the Fed’s 2% inflation target – monthly inflation has to come at 0.2% to be consistent with 2.4% annual inflation, which is the upper limit of the Fed’s tolerance for core CPI.

The Fed has so far treated the January/February spike in core CPI inflation as a “bump” on the way to a sustainable path towards the 2% target. Thus, the Fed has not “overreacted” with hawkish rhetoric.

In fact, the Fed continues to signal 3 interest rate cuts in 2024, based on the FOMC March SEP dot-plot. Furthermore, the market continues to price 3 interest rate cuts in 2024, consistent with the Fed’s signal.

The March CPI report will be the first test of the “inflation bump” thesis. If the core CPI continues to surprise to the upside, which is anything above the required 0.2% MoM core CPI, it would start becoming more likely that we are possibly witnessing a resurgence of inflation – or possibly the second wave of inflation.

The consensus expectations

The market consensus expectations are: 1) the core CPI at 0.3% MoM, which would be less than 0.4% in January and February, and 2) the headline CPI also at 0.3% MoM, also less than 0.4% in the previous two months.

Trading Economics

The expectations are also that the annual core CPI to fall to 3.7% in March from 3.8% in February, which means that technically the disinflationary process continues.

However, the expectations are that the headline CPI will rise to 3.4% in March from 3.2% in February – thus the headline inflation is expected to rise on an annual basis.

The Cleveland Fed’s Inflation Nowcast is predicting 0.31% MoM inflation in March, and also in April. Note, the January and February CPI inflation data increased above the Nowcast predictions.

The Fed’s window to cut is almost closed

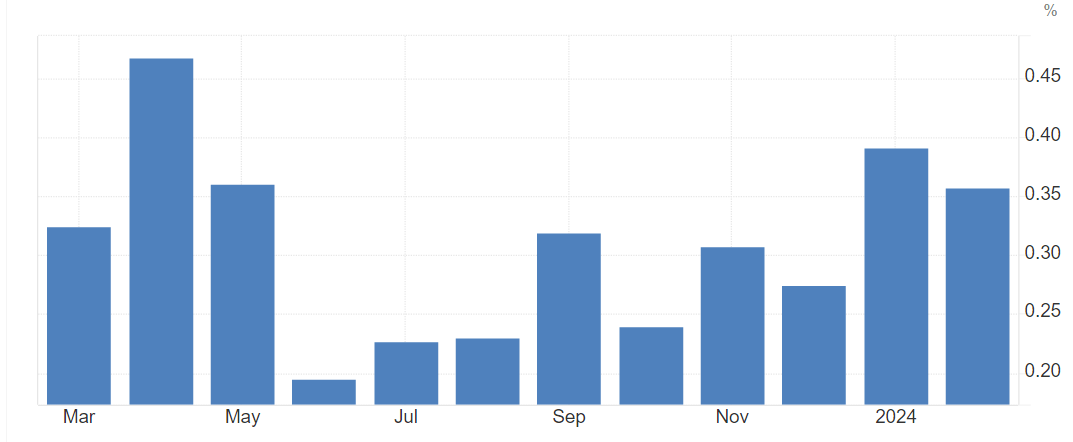

The graph below illustrates the monthly core CPI over the last 12 months. Each month the “last” monthly data is replaced with the “now” monthly data to compute the annual rate of core CPI inflation – which is important for the so-called “base effects”.

The graph below shows that there was a “bump” in monthly core inflation in March, April, and May of 2023, followed by a significant disinflation in June, July and August. These represent the relevant base effects.

The graph also illustrates the current “bump”, in January and February 2024, after a period of gradually rising monthly inflation.

Trading Economics

What this means is that if the March monthly core CPI comes above 0.325%, the annual inflation will stay unchanged at 3.8. Obviously, if it’s above 0.35% (rounded to 0.4%), the annual core CPI will rise. That’s due to the base effects.

But more importantly, once we are past the inflation bump from April/May 2023, the annual core CPI will start sharply rising in June – if the monthly core CPI continues to come at 0.3%. That’s also due to the base effects.

This is important, since the Fed is expected to start lowering interest rates in June, just as the core CPI starts rising. Obviously, the Fed will not be able to cut interest rates in this situation.

In fact, the Fed has a short window to have the first interest rate cut before the core CPI starts rising in June – and the window is all but closed. Thus, it’s unlikely that the Fed will cut in 2024 – unless the recession hits.

The elusive 0.2% MoM core CPI

The Fed desperately needs that 0.2% MoM on core CPI to be able to cut.

Specifically, the yield curve continues to be inverted – and this will cause a recession, as the long and variable lags eventually hit the economy.

More importantly, the approaching maturity wall of junk bond and leveraged loan repricing is likely to deepen the recession as many smaller and weaker firm’s default.

The Fed needs to lower interest rates to prevent the recession with the credit event, especially leading to the elections in November. But, it can’t as long as monthly core CPI readings come at 0.3% or higher.

The key inflation drivers to focus on

Shelter:

Shelter inflation has been the main contributor to the core and headline inflation, particularly via the Owner’s Equivalent Rent, rising by 0.6% in January and 0.4% in February. Given the significant weight of shelter in the total inflation, it will be difficult to have a 0.2% monthly inflation as long as shelter is rising at 0.4% or above.

The Fed’s main “hope” is that shelters will start falling, and that’s based on the apparently falling market rents, not yet reflected in the lagging official shelter inflation data.

Eventually, falling market rents will be reflected in the official data, but will it be in March? Nobody can tell, but this would be a welcome surprise that could validate the “inflation bump thesis” and allow the Fed to cut.

However, the shelter is correlated with the housing prices, and the housing market is still frozen with prices holding near the highs. Thus, it does not appear that shelter will provide relief in the March data.

Energy – commodity driven inflation

The most important variable now is actually energy and commodities. Since the Fed’s dovish turn in December, oil (USO) has been rising. If the Fed cuts prematurely, commodity prices will rise, which could start the commodity driven inflation wave.

The price breakout in gold (GLD) is potentially the leading indicator of the fears that the Fed is letting inflation get out of hand. But it’s not only the dovish Fed that is causing commodity-driven inflation, at least not yet as the US Dollar (UUP) remains strong.

We are in the process of deglobalization, and currently this process is producing two actual wars – in Ukraine and in Gaza, and both of these wars have significant implications on commodity prices, gold and oil.

The point is, there is a high risk of the oil price spike, and this situation is not transitory – it will likely get worse as the de-globalization process advances.

Energy inflation was up 2.3% MoM in February. This trend is likely to continue.

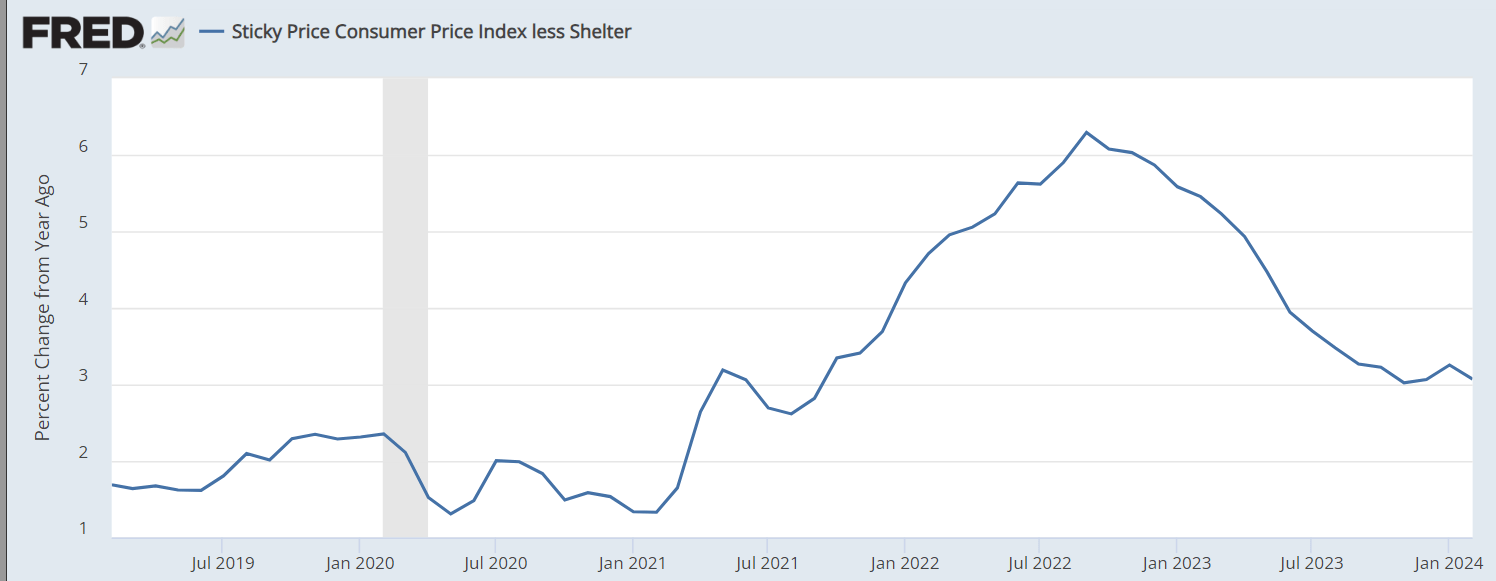

Sticky price CPI less shelter

But let’s ignore energy and shelter, and see what evaluate the core sticky inflation – and this is dependent on wage growth and the overall labor market.

The sticky price CPI less shelter disinflation bottomed in November at 3% YoY, and this is not good news for the Fed.

FRED

Implications

It seems like we are facing several inflationary shocks – defying the “inflaiton bump thesis”:

- First, energy prices are rising, and we could be in the early stages in the commodity-driven inflationary spike.

- Second, shelter inflation remains elevated, reflecting the housing price bubble that has not busted yet.

- Third, the labor-market dependent sticky prices less shelter are bottoming at a 3% annual inflation.

The Fed’s only hope is that shelter inflation will fall. Maybe it happens, let’s see, but it’s unlikely to happen in March, and if the March core CPI comes at 0.3% or above, the window to cut is essentially closed.

The S&P500 (SP500) (SPY) (SPX) has been rising relentlessly since the Fed’s dovish turn in December, counting on the 3 cuts in 2024 – as these cuts could prevent a deep recession.

However, it looks like inflation will prevent the Fed from preventively cutting interest rates. Thus, a deep recessionary bear market is approaching.

The March CPI data could trigger a decisive breakdown in the current uptrend in S&P500 and Nasdaq 100 (QQQ). Whether the stock market could recover and reach the new highs before the recession depends on the big tech earnings, particularly the earnings from Nvidia (NVDA).

On the other hand, the surprise drop in core CPI (falling shelter) could reignite the rally. Given the inflation dynamics and broader macro issues, I would sell all the rallies. Thus, I am downgrading the S&P500 to a Sell from Neutral.

The main reason is the unfolding commodity-driven inflation situation, which is unlikely to allow the Fed to cut, even if the March core CPI comes at 0.2%, especially if the US Dollar starts falling.

{kind=link}